- Positive Start to Fiscal Year:

- Performance met expectations in Q1.

- Sales and Production:

- Sales lower due to selling built-up inventory in previous quarters.

- Production capacity remained optimal.

- Strong demand for products.

- Capex Updates:

- New R&D facility: Half operational, new molecule development underway.

- More R&D sections to be commissioned in the next few months.

- API block: Plant and lab work ready, equipment qualification ongoing.

- Pilot plant batches to begin in a couple of months.

- Additional fermentation capacity: Civil construction halfway completed.

- Capex execution progressing as planned.

Posts tagged Value Pickr

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (27-07-2024)

Investing Basics – Feel free to ask the most basic questions (27-07-2024)

Thank you @Prashant_Karandikar @aditya14920251 @keeyes for sharing your views on the matter. I too find the reasoning a little unconvincing.

Ranvir’s Portfolio (27-07-2024)

FEDERAL BANK –

Q1 results and concall highlights –

Deposits @ 2.66 lakh cr, up 20 pc

Advances @ 2.20 lakh cr, up 20 pc

NII up 19 pc @ 2592 cr

Fee income grew 22 pc @ 652 cr

Other income grew 25 pc @ 915 cr

NIMs @ 3.16 vs 3.20 pc

Gross NPAs @ 2.11 vs 2.38 pc

Net NPAs @ 0.60 vs 0.69 pc

High yielding segments grew at faster rates ( However, these segments grew on a lower base ) –

CV/CE loans up 51 pc @ 3.7k cr

MFI loans up 107 pc @ 3.7k cr

MSME book up 22 pc @ 40.1 k cr

Credit cards book up 73 pc @ 3.2k cr

Gold loans book up 31 pc @ 27.4k cr

Total high yielding book @ 35 pc of total loan book. Growth in high yielding segments is critical for the bank as their NIMs are on the lower side

CASA deposits grew by 10 pc @ 77k cr vs 70k cr YoY. CASA ratio @ 29 vs 33 pc YoY

CASA + Deposits < 3 cr form 80 pc of the Deposit book vs 84 pc YoY

Retail : Wholesale loan book @ 56:44

Yield on advances @ 9.43 vs 9.21 pc

Fresh slippages @ 417 cr – very well controlled – this to me is the key highlight of the results

Expecting the credit quality to remain within control for rest of FY 25 ( at similar levels as in Q1 )

Cost / Income @ 53 pc. Added 210 branches in last 18 months. Despite that, cost / income is trending downwards ( vs Q4 ). Aim to bring to down to 50 pc within 1.5-2 yrs time

Aim to add > 100 branches in FY 25. This should also help in deposit mobilisation

Federal bank’s loans are generally priced lower than other banks in most of the segments they operate. As a result, they are able to get best customers, lower slippages ( its reflected in the numbers as well ). But it comes at the cost of lower NIMs. But this is a deliberate ( and very conservative ) policy

Expect the NIMs to be around Q1 levels for Q2,Q3

Expect to exit FY 25 with RoA @ 1.35 pc vs 1.27 pc in Q1. That should mean – continued momentum in Deposits, Advances and control over slippages

Disc: holding from lower levels, things looks well within control, doesn’t look expensive at CMP, not SEBI registered, biased, not a buy / sell recommendation

Federal Bank – A Turnaround banking Story? (27-07-2024)

FEDERAL BANK –

Q1 results and concall highlights –

Deposits @ 2.66 lakh cr, up 20 pc

Advances @ 2.20 lakh cr, up 20 pc

NII up 19 pc @ 2592 cr

Fee income grew 22 pc @ 652 cr

Other income grew 25 pc @ 915 cr

NIMs @ 3.16 vs 3.20 pc

Gross NPAs @ 2.11 vs 2.38 pc

Net NPAs @ 0.60 vs 0.69 pc

High yielding segments grew at faster rates ( However, these segments grew on a lower base ) –

CV/CE loans up 51 pc @ 3.7k cr

MFI loans up 107 pc @ 3.7k cr

MSME book up 22 pc @ 40.1 k cr

Credit cards book up 73 pc @ 3.2k cr

Gold loans book up 31 pc @ 27.4k cr

Total high yielding book @ 35 pc of total loan book. Growth in high yielding segments is critical for the bank as their NIMs are on the lower side

CASA deposits grew by 10 pc @ 77k cr vs 70k cr YoY. CASA ratio @ 29 vs 33 pc YoY

CASA + Deposits < 3 cr form 80 pc of the Deposit book vs 84 pc YoY

Retail : Wholesale loan book @ 56:44

Yield on advances @ 9.43 vs 9.21 pc

Fresh slippages @ 417 cr – very well controlled – this to me is the key highlight of the results

Expecting the credit quality to remain within control for rest of FY 25 ( at similar levels as in Q1 )

Cost / Income @ 53 pc. Added 210 branches in last 18 months. Despite that, cost / income is trending downwards ( vs Q4 ). Aim to bring to down to 50 pc within 1.5-2 yrs time

Aim to add > 100 branches in FY 25. This should also help in deposit mobilisation

Federal bank’s loans are generally priced lower than other banks in most of the segments they operate. As a result, they are able to get best customers, lower slippages ( its reflected in the numbers as well ). But it comes at the cost of lower NIMs. But this is a deliberate ( and very conservative ) policy

Expect the NIMs to be around Q1 levels for Q2,Q3

Expect to exit FY 25 with RoA @ 1.35 pc vs 1.27 pc in Q1. That should mean – continued momentum in Deposits, Advances and control over slippages

Disc: holding from lower levels, things looks well within control, doesn’t look expensive at CMP, not SEBI registered, biased, not a buy / sell recommendation

Aurion Pro : Yet another IP product company? (27-07-2024)

I’m also invested in the comp. since 49 CMP. ![]()

I am slightly concerned about 4 separate businesses the company is trying to push forward. In the recent investor meet, the question was raised on this regarding how they plan to run 4 different business verticals with the same funds and then plan to become global top 3. I wasn’t totally convinced by his answer that some years some business will be pushed based on the conditions.

I don’t expect them to become top player in all those business and I think they are kind of hedging their bets. They are not married to a business rather the goal is to become a large player in one/more of these businesses.

I wish they’d start reporting the numbers by the business for more transparency, probably this is a question/request to be raised in the next concall.

Disclaimer: I am invested and biased.

Aurion Pro : Yet another IP product company? (27-07-2024)

(post deleted by author)

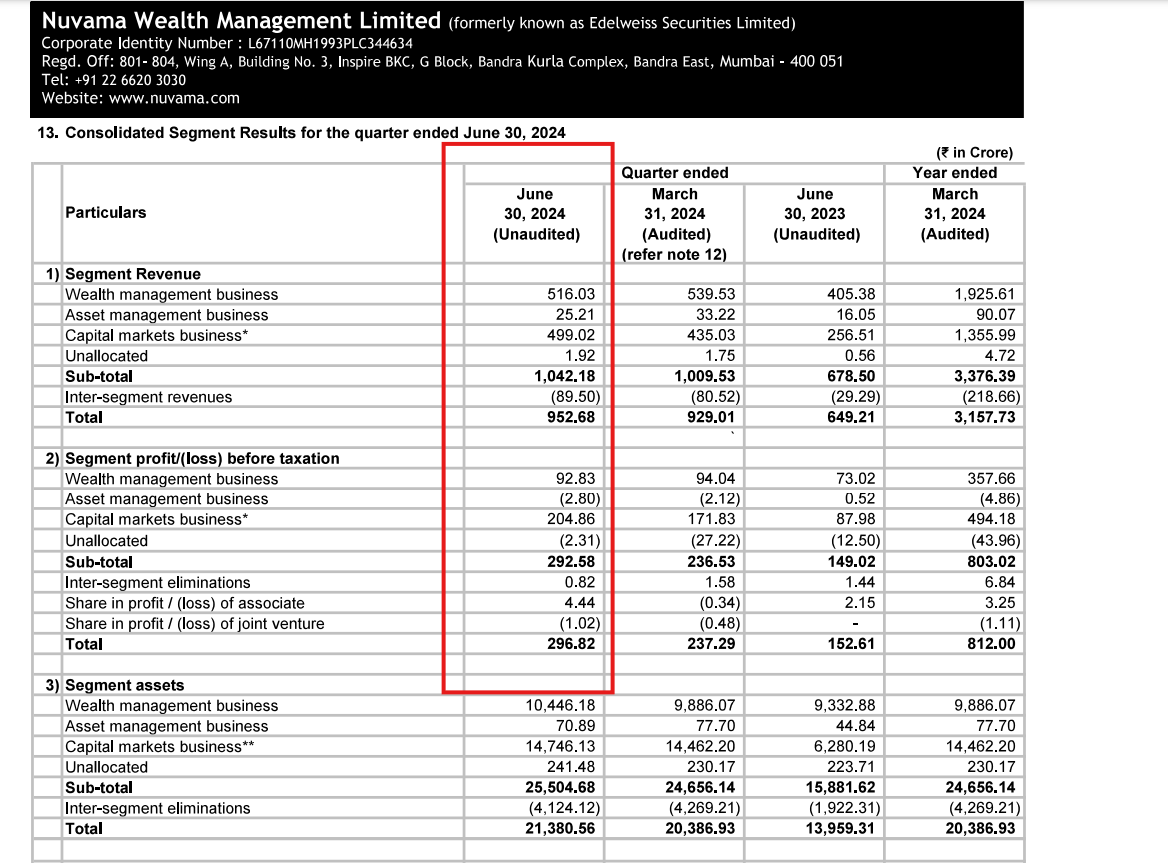

Nuvama Wealth Management: Proxy to Affluent India (27-07-2024)

I agree with the profit part, but I don’t understand how this RM addition and Dubai investment could affect the WM segmental revenue(topline) growth.

In fact, looking at the WM segment on a longer time frame

Revenue: Q2FY23 → 455 : Q1FY25 → 516

PBT: Q2FY23 → 105 : Q1FY25 → 93

I know revenue to AUM should not be looked at in a linearity. But in about 2 years where AUM grew 30-40% CAGR, where is the incremental ARR?

On a positive note, I hope the WM revenue can jump exponentially in the coming quarters, looking at how revenue recognition has been falling behind the exceptional AUM growth.

Microcap momentum portfolio (27-07-2024)

deploying same amount to each stock each week.

for eg, you have 2L to invest for this week, it’ll be 2L/20stocks = 10k in each stock irrespective of their current weight.

@visuarchie , suggests that you invest money in each stock so that their weights become equal.

Globus Spirits (27-07-2024)

(post deleted by author)

SBI Cards & Payment Services Limited (27-07-2024)

Very disappointing results. Asset quality deteriorating.