You seem to hold 81 stocks in your portfolio. Even the Nifty 50 has only 50 stocks.

Posts tagged Value Pickr

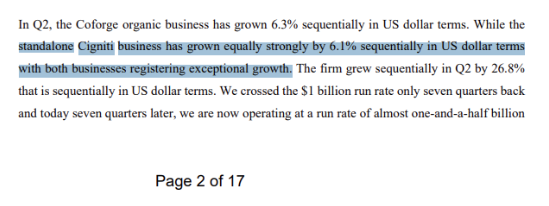

Cigniti Technologies – Global Leader in Software Testing (08-11-2024)

Commentary from Q2FY25 Earnings Call of Coforge, the Promoters of Cigniti.

Link: https://www.coforge.com/hubfs/Transcript-of-Earnings-Conference-Call-Q2-FY25pdf.pdf

- Growth

- Cigniti grew 6.1% QoQ

- This is very strong across growth across all IT companies

- Last 5-year revenue CAGR of Cigniti is 17% (Source:screener)

- We can assume that Cigniti can grow at 10% going forward, conservatively

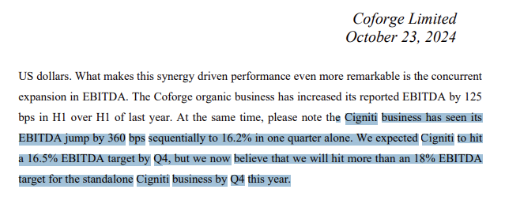

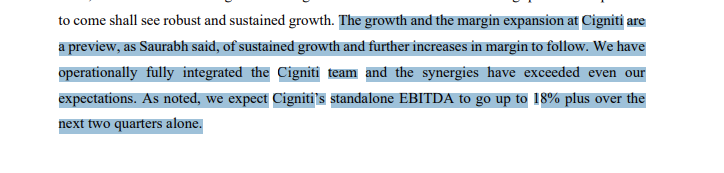

- Big turnaround in Profitability : Cigniti EBITDA margins are expected to go to 18% by Q4FY25

- Cigniti had 12% margins in FY24.

- It is a fair assumption that Cigniti will have 18% EBITDA margins in FY26,

- This margin expansion from 12% to 18% can lead to 50% increase in EBITDA

- Valuation

- Good RoE of 27% over last three years

- If we very conservatively assume 10% revenue growth in FY25 and FY26, FY26 revenue can be 2,200 crores. Management is very positive on revenue growth outlook of Cigniti.

- With 18% EBITDA margin on 2,200 crore, it can mean ~400 crores of EBITDA in FY26

- Cigniti is net cash company with cash of ~400 crores

- Market Cap is 3,800 crores

- EV = 3800 – 400 = 3,200 crores

- EV/EBITDA for FY26 = 3200/400 = ~8x

Nitiraj’s Portfolio (08-11-2024)

I would first like to ask…you provided weights as per market cap…where is the other allocation since the total of the same is not 100%

I am a CFA Level 1 Candidate and it has been 2 years since I took charge of my parents portfolio. (Have been personally investing since 4 years).

The primary problem with our combined portfolio was the same. We had around 48 stocks.

Over the last year I have brought it down to 32 Stocks.

There are certain biases in our minds when it comes to selling stocks. These include but are not limited to Loss Aversion, Endowment etc.

I suggest you to first look into your portfolio composition. I would suggest to not hold too many stocks in the same sector since they have a high correlation. Examples in your portfolio are like Wipro, Happiest Minds, TCS and Infosys which are all software companies.

Next are investments on which you have made significant losses. Book them.

Let me know if you are interested in more advice I can look into it.

GUJARAT GAS Improving outlook on volumes (08-11-2024)

Gujarat Gas Limited Q2 FY25 Summary

Key Pointers from the Call

- GGL is the largest city gas distribution company in India, operating in 27 geographical areas across six states and one union territory.

- The company has filed a scheme of arrangement with stock exchanges to eliminate the layered structure of the GSPC group, promote business synergies, and unlock value for stakeholders.

- GGL has been able to grow CNG volumes by 12% year-over-year.

- They have added nine new CNG stations during the quarter, bringing the total to 820 stations.

- The company is planning to increase the blending level of its hydrogen blending pilot project after receiving necessary regulatory approvals.

- GGL is evaluating options to increase CNG prices in the near future to offset the increased cost of gas procurement due to a reduction in APM gas allocations.

- They are seeing positive growth in the domestic segment, with a customer base of over 2.19 million domestic customers.

- GGL is targeting new markets in Ahmedabad rural, Silvassa, and the Daman, Diu and Silvassa markets.

- The company is looking to enter the LNG trucking business and is in the process of surveying routes connected to major ports in Gujarat and expressways coming up in and around Gujarat.

- GGL’s EBITDA margins are expected to be in the range of 5 to 6 rupees going forward.

- The company maintains a focus on expanding geographical coverage, and expanding its gas network to lead to increased volumes and profitability.

Key Financials

| Metric | Q2 FY25 |

|---|---|

| Revenue from Operations (Crores) | 3,949 |

| Profit After Tax (Crores) | 415 |

| EBITDA (Crores) | 553 |

| EBITDA/SCMD (Rupees) | 6.86 |

| Capex (Crores) | 130 for the Qtr |

| Morbi Volume (MMCMD) | 2.86 |

| Non-Morbi Volume (MMCMD) | 2.05 |

| Total Volume (MMCMD) | 8.75 |

Gas Sourcing Details:

- APM Gas: 31%

- Long-term Contracts: 35%

- Spot LNG: 34%

Average price of spot LNG: ₹37.4 per SCM

Future Outlook

- GGL expects the number of customers in the domestic and commercial segments to increase over time as new areas mature.

- The company is hopeful that volumes will recover in Q3 FY25.

- Management believes that expanding geographical coverage and expansion of the gas network will lead to increased volumes and profitability.

- GGL is in discussions for a new LNG contract to replace the volumes from the BG contract that will expire in mid-2025.

- The company is evaluating options for deploying operating cash flow, including diversifying into renewables and hydrogen.

- GGL aims to grow its presence in the industrial segment, targeting the Ahmedabad rural, Silvassa, and the Daman, Diu and Silvassa markets, and expects volumes in these areas to grow substantially in the next few years.

- The rollout of the FDO scheme is expected to ramp up in the coming quarters, with 125 franchisees already having accepted LOIs.

- When replacing expiring contracts, GGL will prioritize oil-linked contracts but will also include some Henry Hub exposure.

- Overall volume growth guidance for FY25 remains at 5-7%.

Challenges

- Reduction in APM Gas Allocation: GGL has seen a significant reduction in APM gas allocation, which is being replaced by higher-priced new well gas and spot LNG. This will impact margins in the coming quarters.

- Competition from Propane: GGL faces competition from propane in the industrial segment, especially in the Morbi region. The company is working to convert propane users to natural gas, but price fluctuations in propane can make this challenging.

- Maintaining Volume Growth: While GGL has a positive outlook for volume growth, achieving its target of 5-7% growth will depend on factors such as the pace of infrastructure development, competition from alternative fuels, and economic conditions.

- Passing on Increased Gas Costs: The recent reduction in APM gas allocation and the increase in spot LNG prices will require GGL to pass on these costs to customers. The company will need to carefully balance price increases with maintaining its competitiveness against alternative fuels.

- Exposure to GSPC: The proposed merger with GSPC creates indirect exposure to GSPC’s performance until the merger is finalized. While GSPC is not a listed entity, its performance will be closely watched by investors and analysts.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (08-11-2024)

Attended Q1 concall last time and I too felt they are not confident about their prospects. I exited partially last month but I will exit soon as I don’t see any hope unless some drastic changes in the management.

Wonderla Holidays (08-11-2024)

Yes. Wonderla has again disappointed us with Q2 Results. I listened to the Concall and I am willing to continue hold my investments however I just stuck with one question, if the business is so well, they could have gone for Debt instead of QIP. When they have good margins, they could have afforded this. Is there some uncertainty which forces them to stay away from Debt? QIP may lead to dilution of equity and possible decline in EPS etc…

Great articles to read on the web (08-11-2024)

Awesome… An open mind with liberty to think constructively can only analyze such things in a simple way … and also explain in layman terms.

Thanks @diffsoft for sharing your thoughts as a global investor.

Look forward to learn much more from you.

Max Healthcare: A Growing Force in India’s Healthcare Sector (08-11-2024)

Can you please mention the valuation metrics and if possible, a comparison with peers…

Ranvir’s Portfolio (08-11-2024)

Posting my current portfolio breakdown ( I know … the number of stocks are way too many ![]()

![]() ) – however, I believe that I am currently in a stage / age where I need to maximise my learning by reading up ( and tracking ) about as many companies as I can even if I have to sacrifice a few percentage points on returns.

) – however, I believe that I am currently in a stage / age where I need to maximise my learning by reading up ( and tracking ) about as many companies as I can even if I have to sacrifice a few percentage points on returns.

Healthcare and Pharma –

Advanced Enzymes – 0.5 pc

Alkem Labs – 1.16 pc

Ajanta Pharma – 0.76 pc

Alembic Pharma – 0.33 pc

Aarti Pharmalabs – 1.05 pc

Ami Organics – 0.8 pc

Cipla – 1.68 pc

Zydus Lifesciences – 1.40 pc

Dr Reddy Labs – 1.24 pc

Eris Lifesciences – 2.69 pc

FDC – 0.47 pc

Glenmark Life – 1.30

Glenmark Pharma – 1.01 pc

Innova Captab – 1.31 pc

Indraprastha Medical – 0.54 pc

JB Chemicals – 1.32 pc

Kopran – 0.84 pc

Abbott India – 0.43 pc

Laurus Labs – 0.75 pc

MANKIND PHARMA – 0.83 pc

Neuland Labs – 6.98 pc

Piramal Pharma – 1.48 pc

Rpg Lifesciences – 1.21 pc

Shalby Ltd – 0.64 pc

Supriya Lifesciences – 2.44 pc

Sun Pharma – 1.09 pc

Star Health – 0.24 pc

Wockhardt – 1.22 pc

Windlas Bio – 0.81 pc

Yatharth Hospitals – 0.67 pc

Financials –

ABSL AMC – 0.58 pc

HDFC AMC – 1.37 pc

NIPPON Life AMC – 2.11 pc

Bajaj Finserv – 1.67 pc

Chola Investment and Fin – 1.95 pc

IIFL Finance – 0.88 pc

Karur Vysya Bank – 1.64 pc

Federal Bank – 1.04 pc

Kotak Bank – 1.51 pc

Axis Bank – 0.95 pc

Agri Inputs –

Dhanuka Agritech – 1.97 pc

Insecticides India – 0.64 pc

Godrej Agrovet – 0.86 pc

Building Materials –

Cera Sanitaryware – 1.10 pc

Prince Pipes – 0.56 pc

Carysil – 0.32

Retailers –

Electronics Mart – 1.56 pc

Aditya Vision – 1.12 pc

Senco Gold – 0.81 pc

MISC + Manufacturing –

Garware Hi Tech – 1.65 pc

Time Technoplast – 1.27 pc

Technocraft Industries – 1.45 pc

XPRO ltd – 1.13 pc

Shaily Engineering – 0.99 pc

SG Mart – 0.51 pc

Mayur Uniquoters – 0.53 pc

Updater Services – 0.85 pc

Usha Martin – 1.48 pc

Metals and Mining –

Hindustan Zinc – 0.81 pc

Hospitality –

Benares Hotels – 1.46 pc

EIH ltd – 1.75 pc

Kamat Hotels – 1.23 pc

Royal Orchid – 1.05 pc

SAMHI Hotels – 0.80 pc

TAJ GVK – 0.73 pc

Wonderla Holidays – 0.99 pc

FMCG –

ADF Foods – 1.56 pc

Zydus Wellness – 1.45 pc

Dodla Dairy – 1.32 pc

Dabur India – 0.54 pc

Emami – 0.68 pc

There was a steep runup in some of my portfolio holdings in the last 1-2 months because of which I reduced their portfolio weights. These include –

MANKIND PHARMA

RPG Lifesciences

Piramal Pharma

Senco Gold ( additional reason in case of Senco Gold was industry wide pressure on stud ratios because of falling demand for natural daimonds )

Windlas Bio

Innova Captab

Ami Organics

Prince Pipes, Kamat Hotels and Royal Orchid Hotels continue to be laggards. I am hopeful of good recovery in both Kamat and Royal Orchid Hotels ( going by Q2 trends ). Price Pipes may be in for extended pain because of increased aggression from Mkt leader – Supreme Industries

I continue to be bullish on Indian CDMO + API companies – because of the American Biosecure Act and the China + 1 effect playing out in this sector

Dabur and Emami are recent opportunistic bets – anticipating a bottoming out of consumption cycle ( as Govt spending accelerates in Q3, Q4 )

Reliance Capital- Growth at cheap Valuations? (08-11-2024)

Good story about how Reliance Power bids for a project using a bank guarantee from a foreign bank, which needed an Indian bank’s endorsement – but the endorsement was fake, it seems, cos the email on it was http://s-bi.co.in ![]()

management: once a fraud, always a fraud