I didn’t mean that the current PE was cheap. I am looking at the forward PE and find it reasonably valued.

Posts tagged Value Pickr

Manappuram Finance (27-06-2024)

Don’t know if it’s a coincidence, but both Muthoot & Manappuram are hiving off their microfinance subsidiaries at a time when there are signs of the cycle turning.

Irrespective of that, I think worth monitoring as MFI has done very well for them in the recent past.

DLINK: Small Company with a Big Brand (27-06-2024)

PnL Statement: (last 9 years)

· Low sales growth except for 2019/22/23

· Low OPM except for 2023/24

· Other income high from 2020

· Low NPM except for 2023/24

· High capex 2020/23

· Low growth of Net Fixed Assets

· Fluctuating receivable days

· Fluctuating Inventory Turnover

· Low RoE except for 2023/24

· Low RoCE except for 2023/24

· High Dividend payout

Highly Competitive Indian Market. Jio, Airtel & others providing their own router.

The revenue & profitability improvement in the year2023 is because of the below factor. Although when we see the year2024 revenue/profitability, there is not much further improvement or progress.

Looks like a highly commoditized market with low profitability margins.

Positive-

D-Link (India) Limited is strongly focusing on local products as part of its ‘Make in India’ initiative. “Make in India,” and localization of products are two important initiatives of the Indian government that are closely linked. D-Link (India) has been granted exclusive rights/ license by the parent company to use the D-Link trademark for such

locally manufactured products. The Company had made strategic decisions on manufacturing certain products locally through third-party or contract manufacturing with its own brand names, under its own proprietary designs, quality control and supervision.

The Company has made noteworthy progress in this direction and has entered into arrangements with local manufacturers.

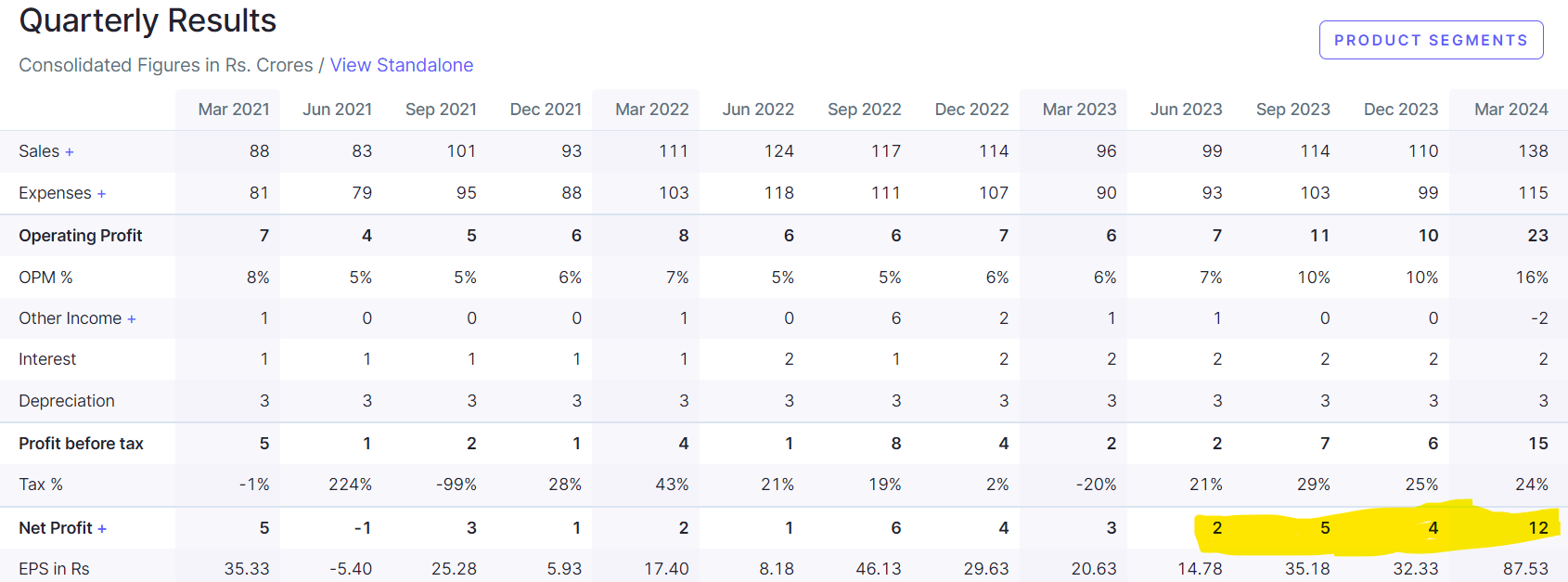

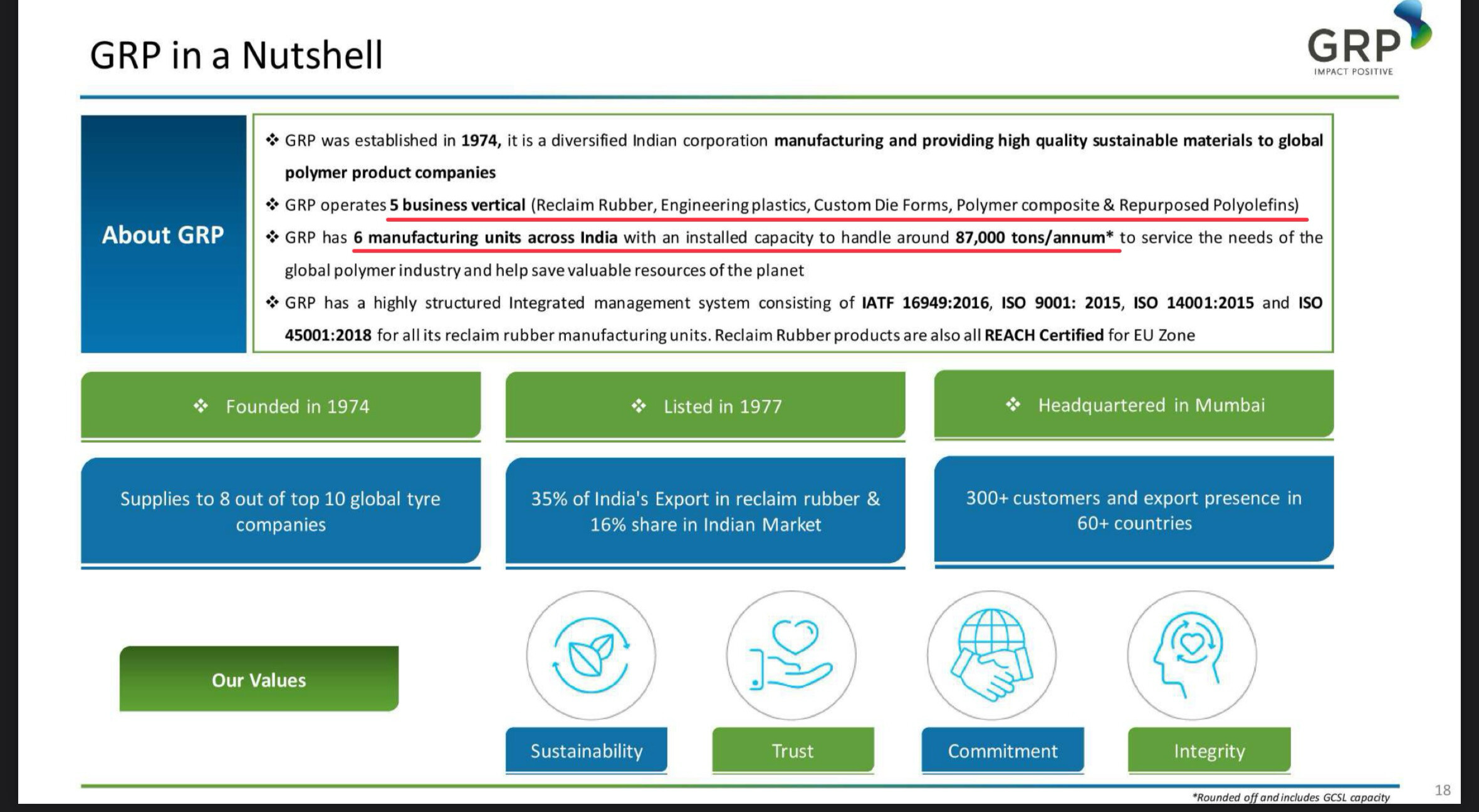

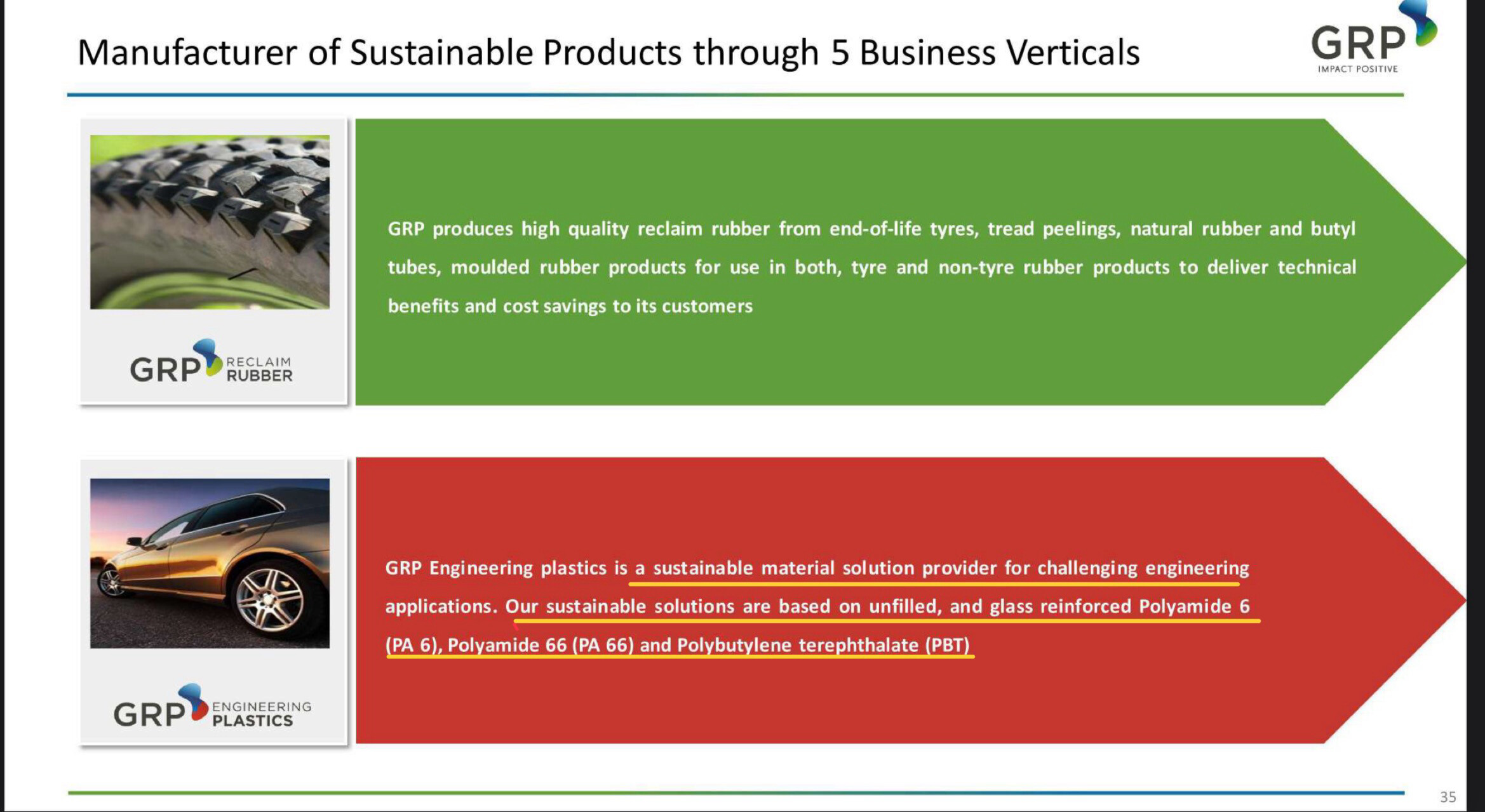

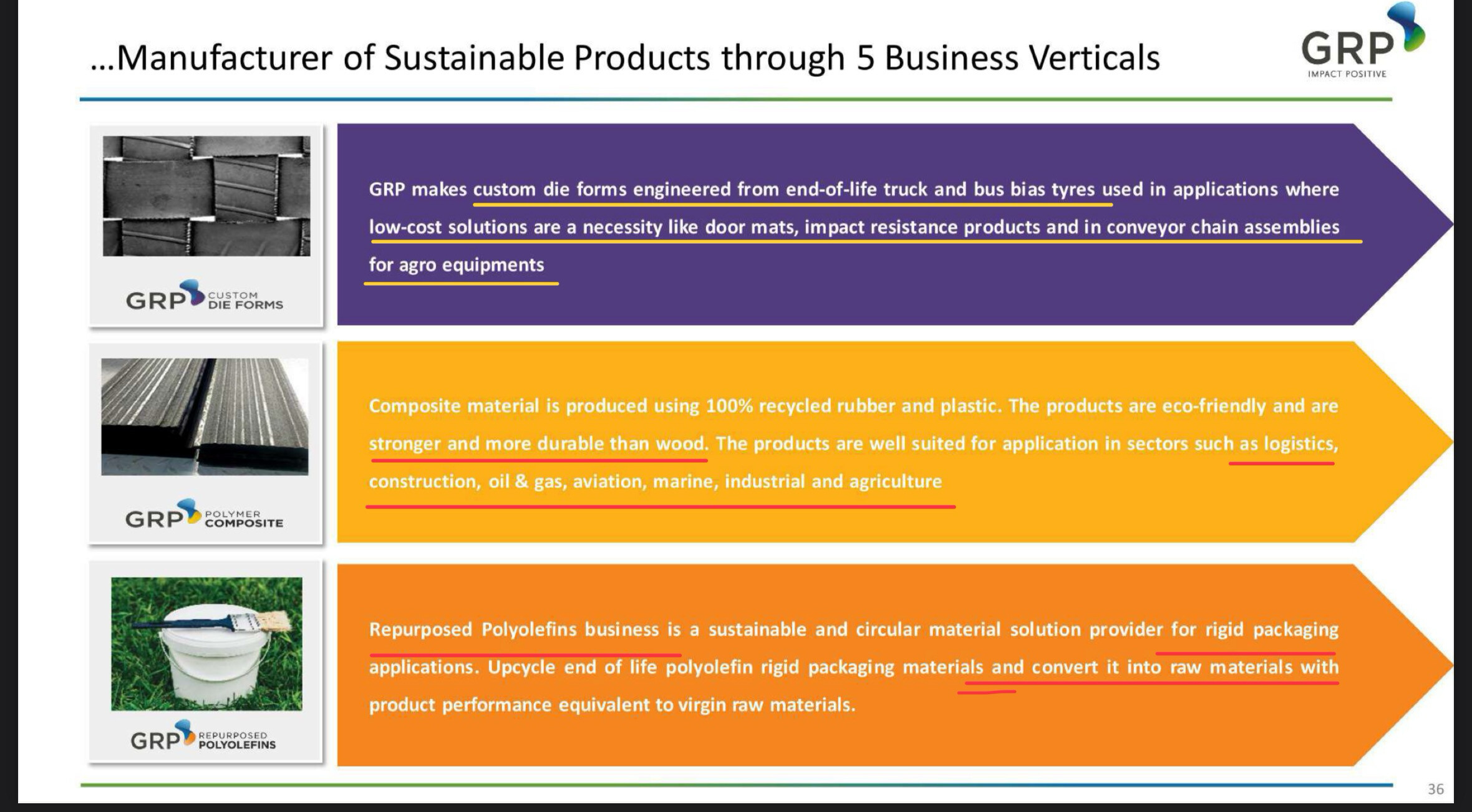

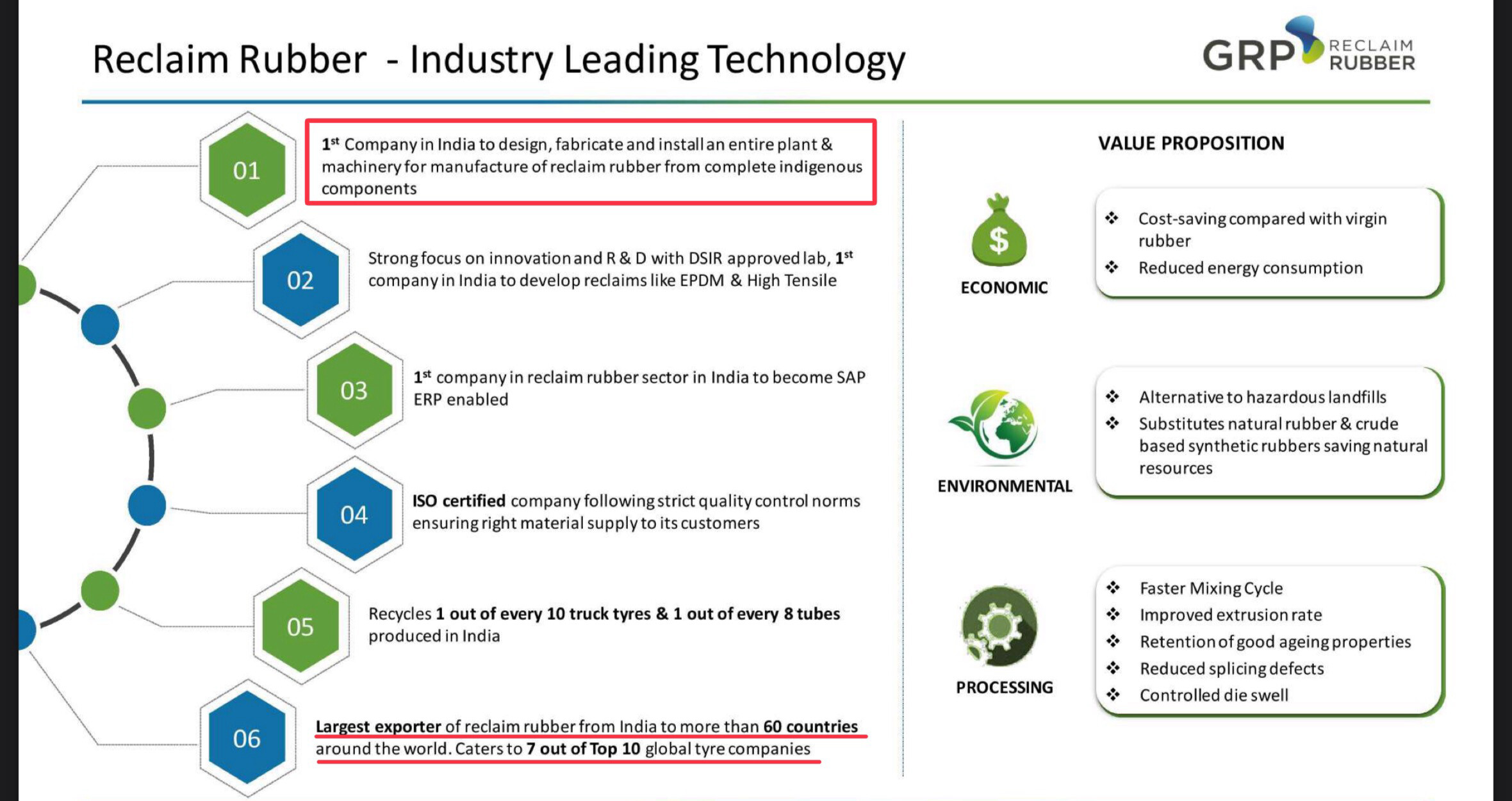

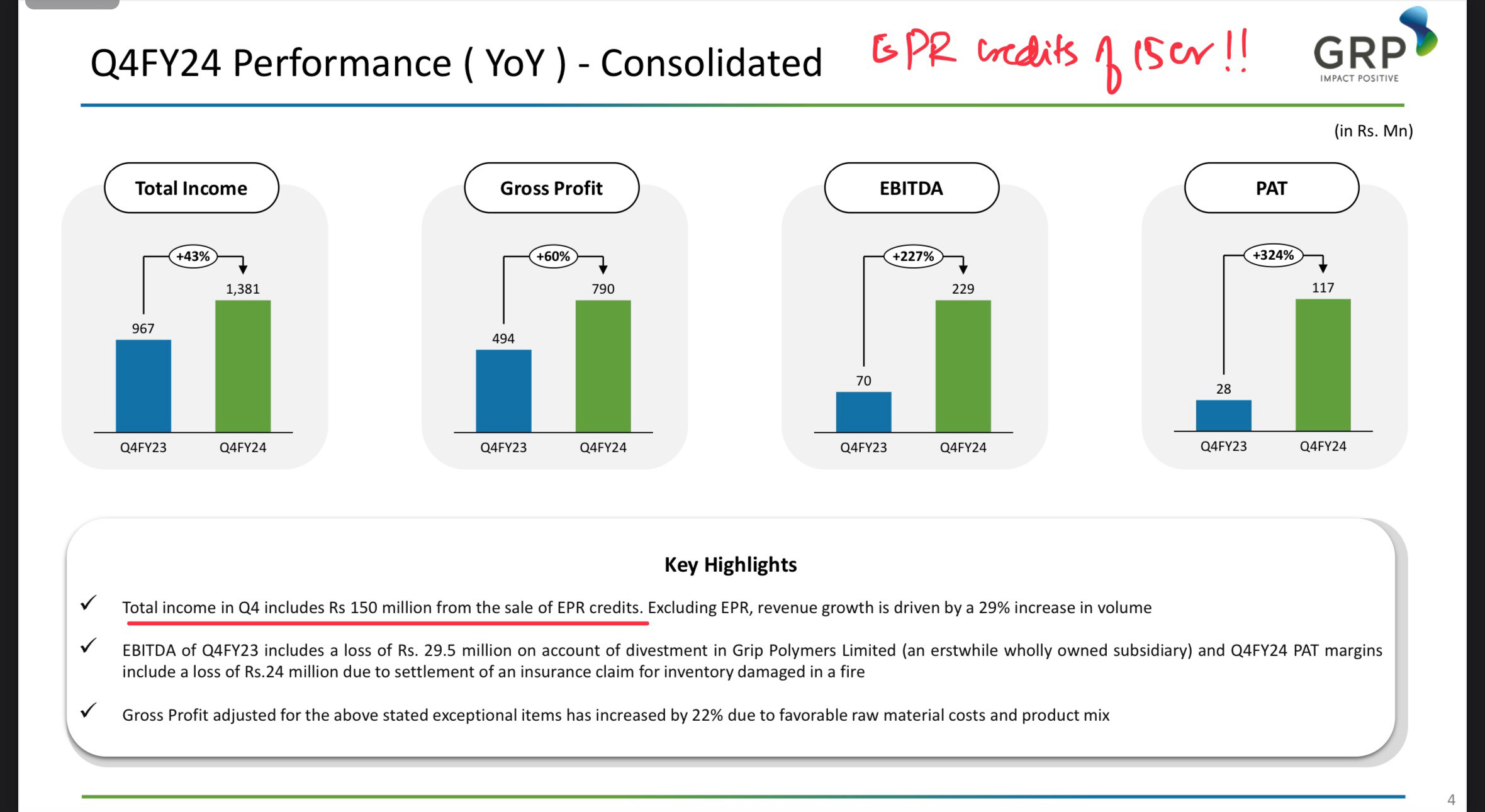

Gujarat Reclaim Rubber (now GRP Ltd) (27-06-2024)

This stock delivered 3x of their usual PAT avg in Q4 . This is what piqued my interest.

.

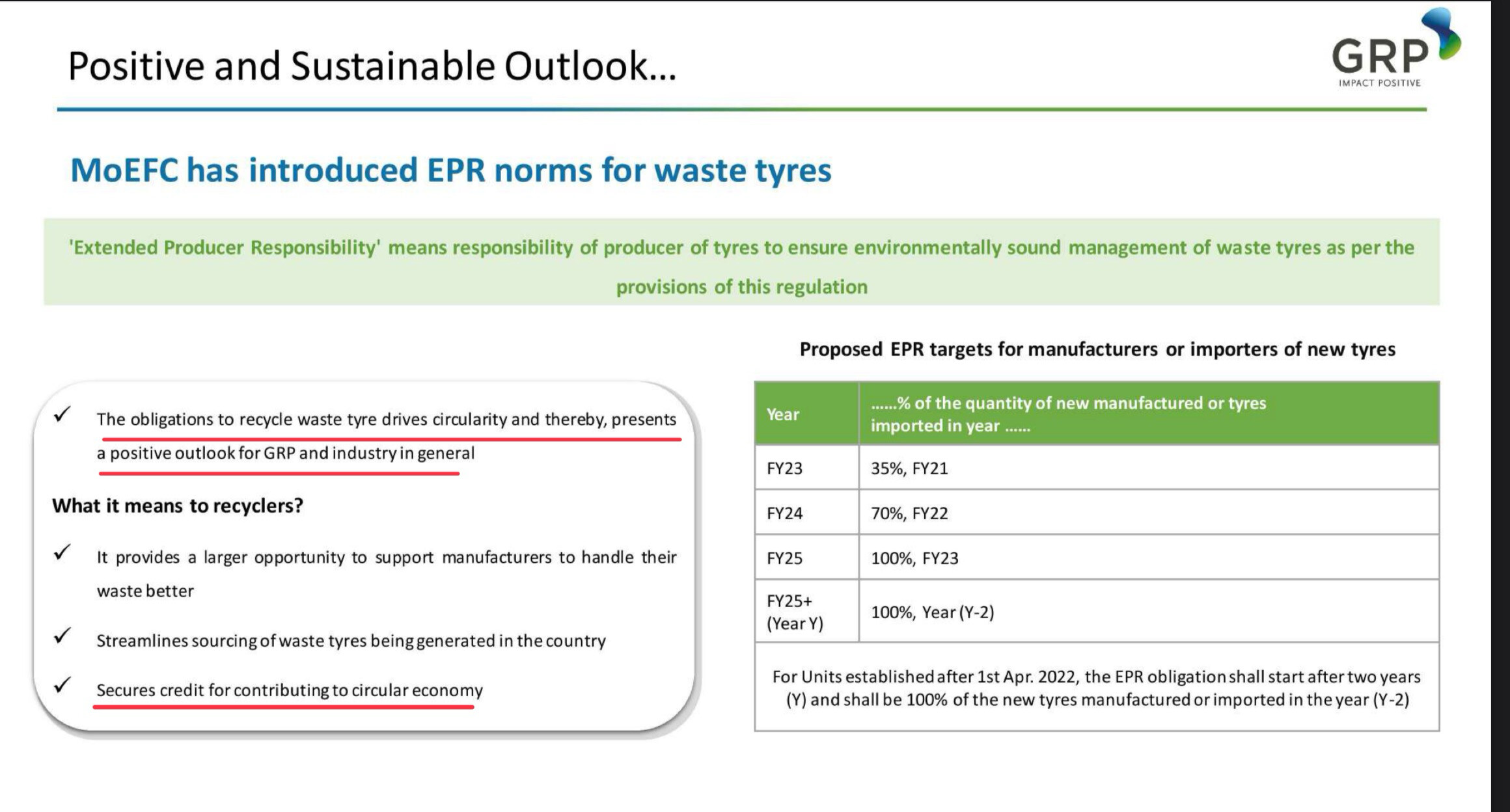

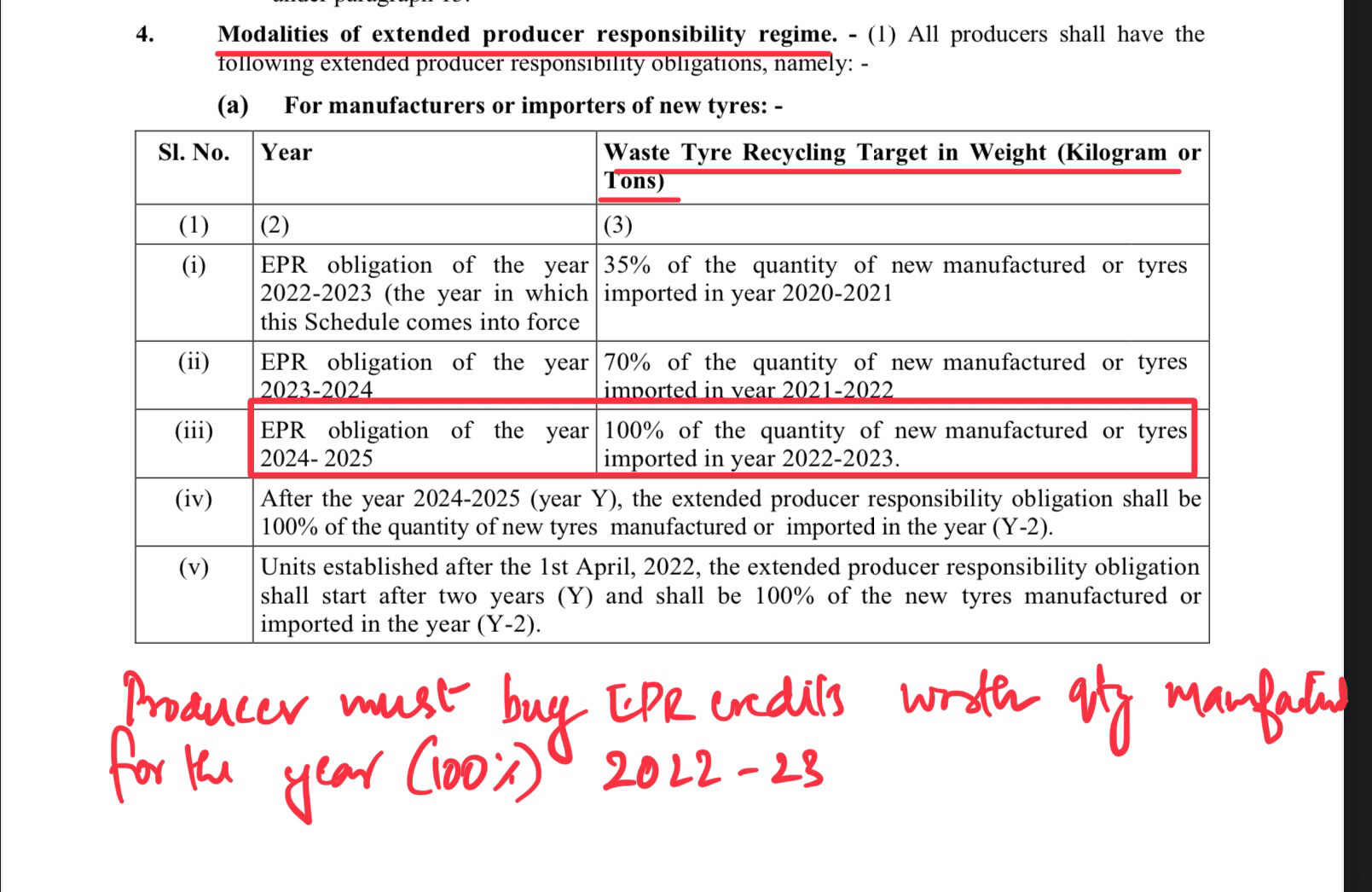

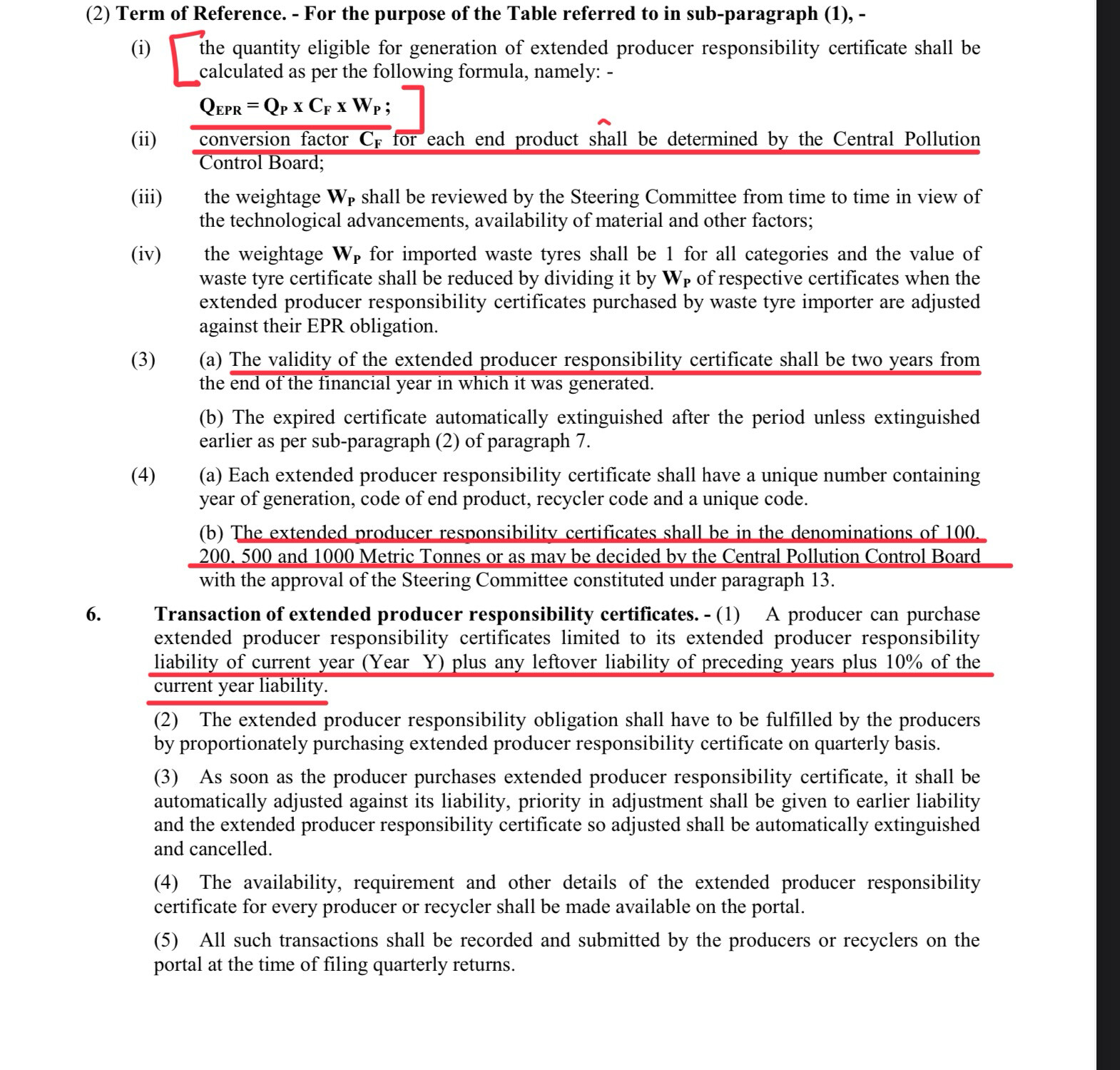

Part of the reason for this bumper performance is due to EPR (Extended Producer Responsibility). I believe this has the potential to change the fortunes of this once loved now forgotten company.

Back of the Envelope Calculation on the EPR credits for GRP:

Current Capacity: 72000 MT

Capacity Utilization : 85%

Production : 60,000 MT

Q(EPR) = Q(P)x C(P) x W(P) = 60000x .78x 1.3 ~ 60000 certificates/ 600 certificates of 100 MT denomination.

In Q4 FY24 GRP has realised 15 Cr from EPR credits (As per management only partial credits realised for FY 22-23 ).

Assuming 60% of the credits are realised for FY 23 we can arrive at approx Rs 4000/MT as addnl realisation due to EPR credit .

The beauty of this is that this amount directly flows into the the EBITDA and boosting the margins as evident from Q4 .

P.S : Realisation for EPR credit is negotiated one on one with the tyre manufactures and this value is bound to vary depending on the demand and supply. However since GRP has several years long relationship with major tyre manufactures they have a natural advantage.

Brief Note on the company :

Concall Notes :

-

EPR for tyres started after 3 years of extensive work including the govt. /CPCB/ Tyre brands etc.

-

Partially realised EPR credits for FY 22-23 . Company has generated credits in CPCB portal for FY 22-23, 23-24 and 24-25 .

-

Global brand owners are also focused on the sustainability initiatives of the recyclers. GRP is the first Indian company to be certified for ISCC- ” International Sustainability and Carbon certification “

-

100% subsidiary launched for repurpose Polyolefins business . Applications in paint and Lubricant sector.

-

Successful approval of Engineering plastics business by a European major , paving the way for entry into major auto OEMs.

-

Successfully commissioned new technology for manufacturing reclaimed rubber.

-

Additional land acquired in Sholapur for crumb rubber plant and venture into down stream recycling.

-

EPR regulations in plastics is getting delayed for implementation , expected in current FY.

-

New range of products in engineering plastics business from ocean plastics. Eg : Fish net waste.

Conclusion:

GRP is positioning itself not as a tyre recycler but as the most important cog in the circular economy .Their entire business is in the ESG domain. With the current tailwinds on environment, recycling etc and with introduction of EPR looks like good times are ahead.

Disc: Invested after Q4 results.

MapMyIndia – The Map Company (27-06-2024)

The new company would be doing consulting business using the data of mapmyindia…

Consulting is a high profit business with no loss potential… I feel that is wrong as this profit should not go to the new unlisted company but rather to mapmyindia…

Sealmatic India Limited (27-06-2024)

Disc: Invested

All fine to be an optimist. However it is not ok to deny your own prior statements.

Rather, since the company is making an honest effort to keep it’s shareholders (particularly the small retail investor), address why your numbers went awry. It is a place of learning, not of denial.

If we find our management to be leading us astray, this is a very bad sign.

I have great faith in this company and it’s ip, it’s concept of the annuity style return of it’s products, the fact that the promoters have deep expertise in it, that they are willing to have regular concalls, answer questions from investors, that they discuss future plans, and have invested in capex. It is not with a little hope that we have invested with them, but denying previous statements begins to make one nervous.

I think it is an appropriate concern that has been brought up in the forum and we, as vulnerable investors, must be alert too. The very best minds were fooled by Enron et al.

@Nimit @rinkupranjan are right to observe this lapse on our behalf.

Sealmatic India Limited (27-06-2024)

Also Mr Balwa said that once the seal is sold they have assured business for the next 20/30 years. How true is that. Once the existing seal is gone will the user should necessarily buy form Sealmatic or they can buy any other seal from other business?

Piccadily Agro Industries Ltd (27-06-2024)

Piccadily Distillery Visit (India)

Found this video very much insightful!

They are creating a visitor building with a golf course trying to emulate Sula

How to find SIP returns for a stock over 3 months / 6 months / 9 months etc? (27-06-2024)

Dear Community,

I’m investing in Stocks ( SIP way ) every month I purchase same amount of stocks.

I’m trying to find out SIP ROI values over x months, but I couldn’t find any website which gives such value.

With Tata Consultancy Services Share Price NSE/BSE – TCS Stock Price Live Today – Tickertape, one can find out 5 year SIP returns but I wish to know particular period SIP returns.

Kindly help me with this requirement.

Thanks in advance.

Regards,

Vikram

Sona Comstar BLW – Direct EV Play (27-06-2024)

Yes, all the 3 segments. They are primarily a differential assembly, several types of gears and starter motor producer. They even have global market share in many of the products. Indeed, they have application in all the 3 segments you have mentioned above.

They are using their existing expertise in starter motor manufacturing to transition into EV traction motors and using the expertise in differential assembly and gears to make same products for EVs.

It’s noteworthy to mention that the differential gears and other gears used in EV shall be exclusively designed, as they need to be extremely strong (as compared to ICE) and should have very good weight to strength ratio.

- Extremely strong – Unlike ICE in EVs torque is very high as the whole power from motor is transferred to the underlying transmission system at once. So, the whole transmission assembly is under immense stress.

- Very good weight to strength ratio – More weight in EV leads to less range

Sona BLW is market leader in this technology of making extremely strong forged components that have very good strength to weight ratio. Also, these components are not generally fungible, that means have to be customized to designed exclusively for an OEM. That leads to the industry best margins for this company. IMHO, they are acting as a contract R&D partner and later contract manufacturer.