There’s a proverb Fake it untill you make it.

Since I don’t see much progress or activities in this company so company might have released something that makes people think of their work contribution or involvement in the industrial activities. As someone suggested they may come up with QIP or atleast increase their shareholder to a minimum so that it can appear in many screens as promoters increased their share ![]() . Poor investors if they can’t understand the math behind it

. Poor investors if they can’t understand the math behind it

Posts tagged Value Pickr

Eco Recycling Limited (Ecoreco (05-11-2024)

Srestha Finvest Ltd: A Strategic Shift Towards Green Finance and Sustainable financing (05-11-2024)

I don’t understand 2things CMP is less then QIP price then why new investor will buy at rs 1.05per share,then old investor nexus,mocktail, etc continues selling if company doing well any suggestions from any body ,

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (05-11-2024)

Has anyone used or seen a Gensol’s leased EV?

Separately, has anyone in the group visited their EV car manufacturing plant? will be good to get any thoughts.

My sincere apologies if this was addressed in the thread and I missed it.

Avenue Supermart: a compounding machine? (05-11-2024)

Any view on the unit economics of QC, specifically BlinkIt?

Zomato – Should you order? (05-11-2024)

BlinkIt or Zepto (QC: quick commerce) service will sustain and grow since the service provides extreme convenience, specifically in metro cities and for items that are required immediately, unique and fresh.

Per AR of FY24, BlinkIt is yet to breakeven at the EBITDA level. Also, management is focused to densify and expand stores at EBITDA level breakeven. Customers already pay MRP or best price compared to ‘slow reaching value offers’ along with platform fee and tip to the rider for convenience.

What levers QC has on the revenue side and cost side to improve gross and operating margins? AR disclosures are not sufficient for my mind to make any progress on this aspect.

Anyone has any opinion on this aspect?

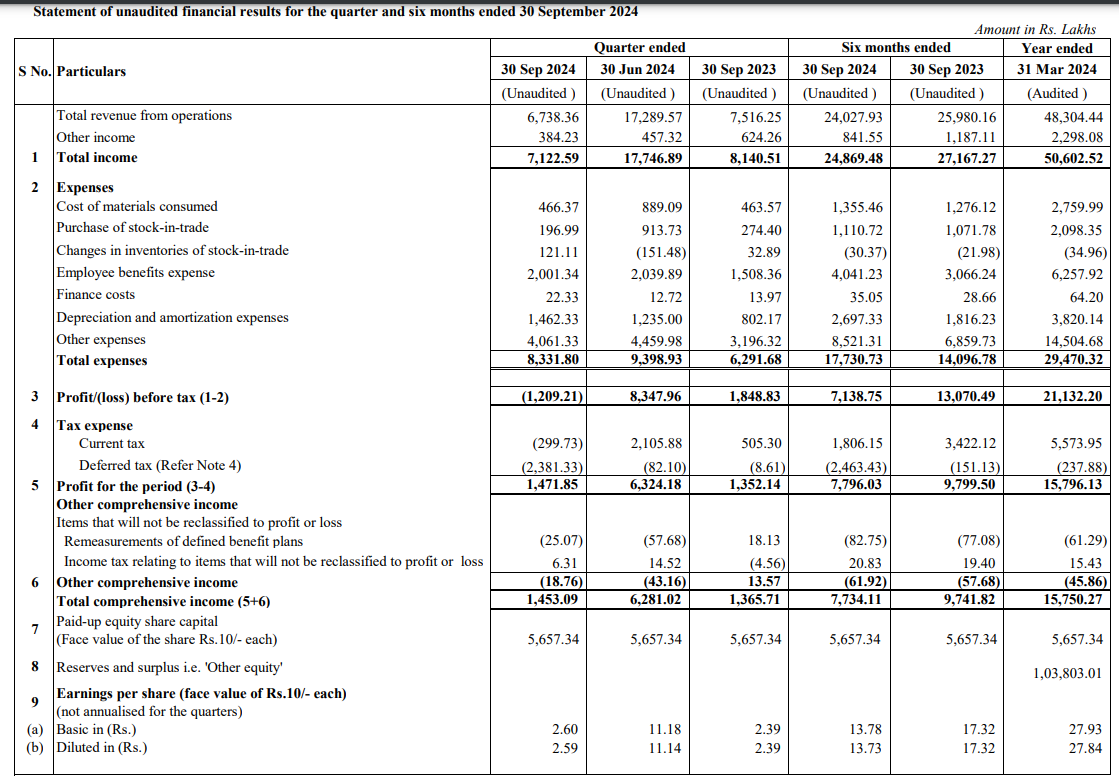

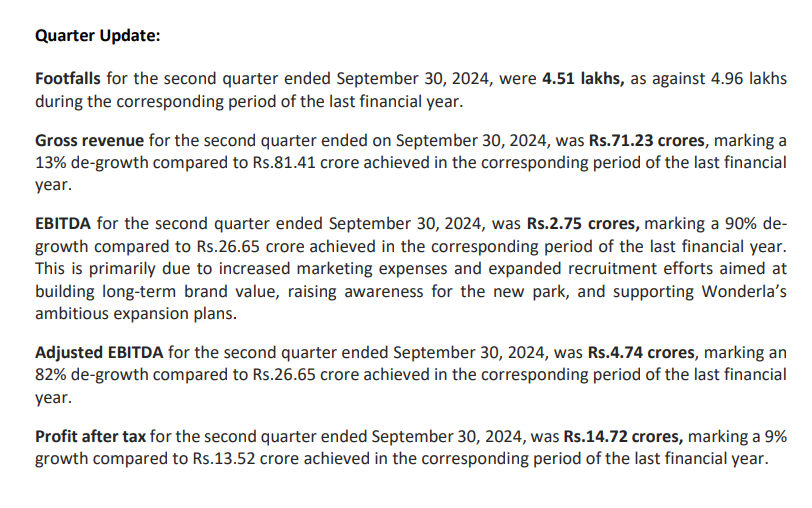

Wonderla Holidays (05-11-2024)

Not invested:

They have a pre-tax loss, but due to the deferred tax, they ended up with profit. They also had a footfall drop.

Raymond – The Complete Man (05-11-2024)

Booking value (no. of units sold) gets a bump-up with new launches. Since new launches don’t happen every quarter, this could be uneven. I guess there were a couple of new launches in Q2 of last year

Geospatial sector – Sunrise Opportunity (05-11-2024)

Devendra Fadnavis, the deputy CM of Maharashtra emphasizing how important river linking is.

Farmer Relief | Wainganga-Nalganga Project | विदर्भ होगा सुजलाम-सुफलाम | #DCMDevendraFadnavis

CM Eknath Shinde seems to be echoing his thoughts.

https://www.uniindia.com/news/west/maha-shinde-river-linking/3250001.html

Again, this could be a pre-election stunt for the upcoming Maharashtra elections, but one can never know for sure.

Investment journey of a late starter (05-11-2024)

I do not have any since it was semi trade not a proper investment based on own conviction . WPIL thread in VP , some entries in Mr. Rajeev Jawahar’s thread in VP and some details in screener along with a few call transcripts is all that I read and entered as it seemed a good opportunity for quick gains . These lines of businesses are capital heavy ,highly competitive and usually is not very highly valued . More importantly , I am not a very good at analysing these to build strong conviction . So I trade in and out …bought at 3088 and exited at 3930… again bought at 368 and sold at 525 (very sharp run up ) . Will enter again if it pulls back and settles …it has enough reasons to go up for a while if the water works theme sustains as it has better results ahead in coming 2 quarters.

Ranvir’s Portfolio (05-11-2024)

Hindustan Zinc –

Largest and the only integrated producer of Lead, Zinc and Silver in India. Has a 75 pc mkt share in India’s Zinc industry

3rd largest producer of Silver in the world

2nd largest producer of Zinc in the world

Among India’s largest producer of Wind Power with a generation capacity of 274 MW – spread across 5 states

Company’s Mineral resources – Hindustan Zinc’s ore reserves are estimated @ 281 million Tons of material graded @ 4.5 pc Zn, 2.0 pc Pb and 60 gm/ ton of Ag – amounting to 12.68 million tons of Zinc ( Zn ), 5.52 million tons of Lead ( Pb ) and 542 million Ounces of Silver ( Ag )

Company’s Ore reserves – Company’s ore reserves are estimated @ 175 million tons of material graded @ 5.6 pc Zn, 1.6 pc Pb and 55gm/ton of Ag – amounting to 9.86 million tons of Zinc ( Zn ), 2.75 million tons of Lead ( Pb ) and 312 million Ounces of Silver ( Ag )

At current production rates and existing Resources and Reserves ( R&R ) company can sustain 25 yrs of mine life

In FY 23-24, company successfully added 24.7 million tons of material at gross level amounting to 1.85 million tons of metal

Company has set up a dedicated subsidiary – Hindmetal Exploration Services Pvt Ltd – to continuously focus on exploring, discovering, developing and tapping mineral resources. The subsidiary has interest in exploration of all minerals across the globe by implementing best in class technologies and practices

Company currently operates 8 underground mines @ 5 locations in Rajasthan

Ore mined in FY24 vs FY 23 @ 16.5 vs 16.7 million tons

Zinc metal mined in FY 24 vs FY 23 @ 0.855 vs 0.839 million tons

Lead metal mined in FY 24 vs FY 23 @ 0.168 vs 0.165 million tons

Q2 FY 25 results and concall updates –

Revenues – 8242 vs 6792 cr, up 22 pc

EBITDA – 4164 vs 3122 cr, up 33 pc ( margins @ 50 vs 46 pc )

PAT – 2389 vs 1729 cr, up 38 pc

India is expected to become the third largest Zinc consumer by 2026 – a key positive for the company

Mined metal production ( Zn + Pb ) in Q2 was @ 0.256 million tons, up 2 pc YoY

Refined metal production ( Zn + Pb ) in Q2 was 0.262 million tons, up 8 pc YoY

Silver production stood at 184 Tons, up 2 pc YoY

Company has achieved a 6 pc reduction in unit cost of production, along with supportive metal prices to achieve 38 pc PAT growth on a YoY basis

Company’s 5.1 lakh tons per annum fertilizers plant is under construction @ Chanderia. It ll be producing DAP fertiliser and NPK nutrients. Likely to go live by Q2 FY 26

Company’s 1.6 lakh tons per annum roast smelter ( using roast leach electro technology ) is likely to go commercial by Q4 FY 25

Company has entered into a 25 yr long renewable power purchase agreement with Serentica ltd – this would @ a fixed flat rate of energy buying without any inflation and would help the company move towards its sated goal of reducing costs to $ 1000 / Ton

In Q2, cost of production ( COP ) for Zinc stood @ $ 1071 / Ton – lower by 6 pc YoY

Current share of renewable power being used by the company in around 14 pc. By the end of Q4, company expects to hit a share of renewable power @ 24-25 pc, This should further help reduce the COP/Ton. Company is striving to achieve $ 1050 / ton – COP by end of Q4 FY 25

The fertiliser plant that the company is expected to commission next yr has the potential to do peak EBITDA of 450 – 500 cr / yr

For H2, company has hedged 1 lakh ton of Zinc @ $ 3008 per ton and 83 tons of Silver @ $ 32.26 per ounce

H2 is generally better for the company in terms of volumes vs H1

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation