I would welcome the notes from the fellow investors. The company usually shares the AGM transcript on its website: avantel.in > Investors > Financial Information > AGM – EGM Proceedings

Posts tagged Value Pickr

Digispice – play on the rural economy (06-06-2024)

@utsav08 ji, thanks for the reply. One more doubt, what do they mean by CASA service, they are not a bank, so where are they storing Adhikari’s funds?

Anshul’s investing journey (06-06-2024)

A bit late but here it is

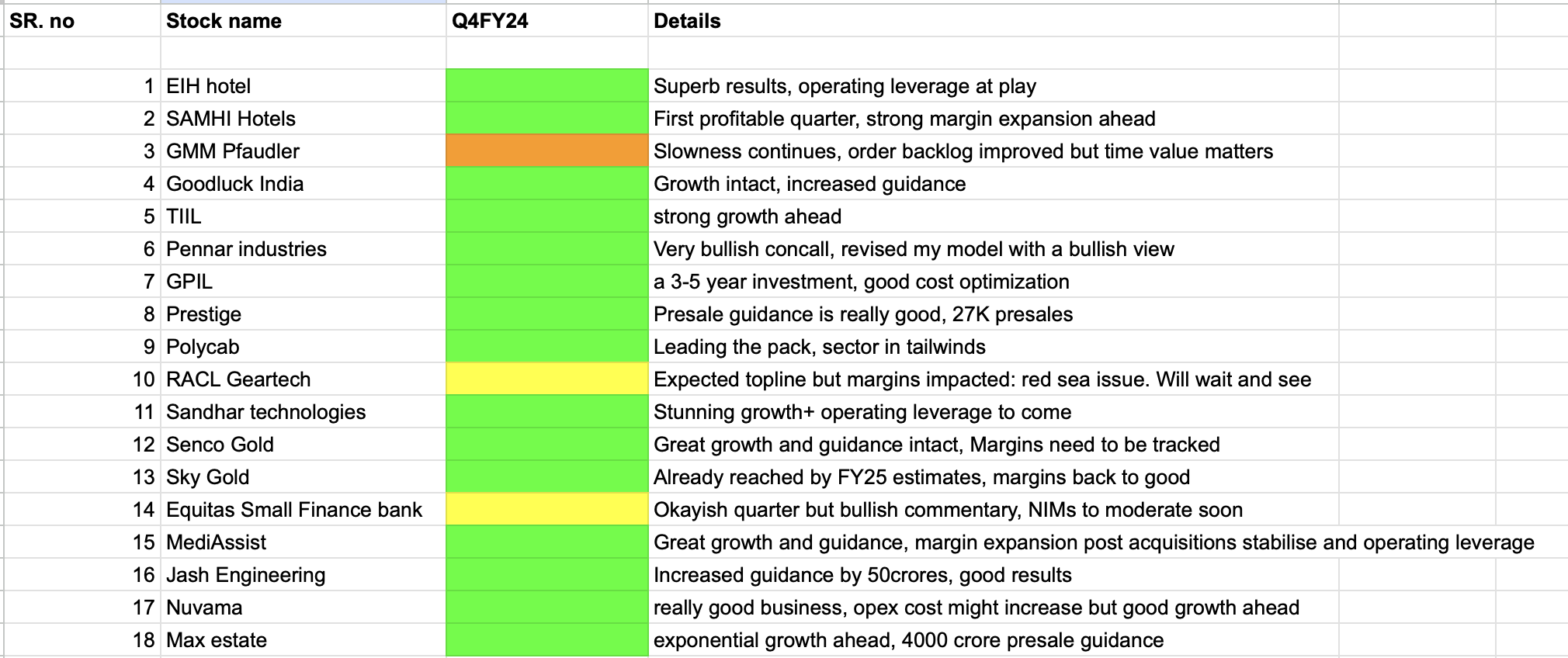

My quarterly update

There have been a few changes which I will explain and maybe and a few possible mistakes that I want to delve deeper into.

I have exited South India bank, GMM,NH, Sanghvi movers and added Nuvama and Max estate.

Why did I sell each of them?

Slow to no growth: GMM and NH. Sold GMM ±5% of cost and NH at +5% I think. not much to gain or lose.

South India bank: I found it better to allocate capital in other businesses and add Nuvama.

Sanghvi movers: Thesis of exponential increase in profitability wouldn’t have been possible because of focus in EPC. Hence, thesis was proven wrong( I still see good growth potential though). luckily ended up in profit anyways.

Why added these? Nuvama I have started a thread and you can check my thesis there. I think the upside is high and downside limited. elements of cyclicality are present but it should work out for the better in the next 3 years hopefully.

Max estate has really strong growth ahead and I believe that Real estate will be one of the biggest winners. Hence, went for it.

Here is my take on the relevant businesses

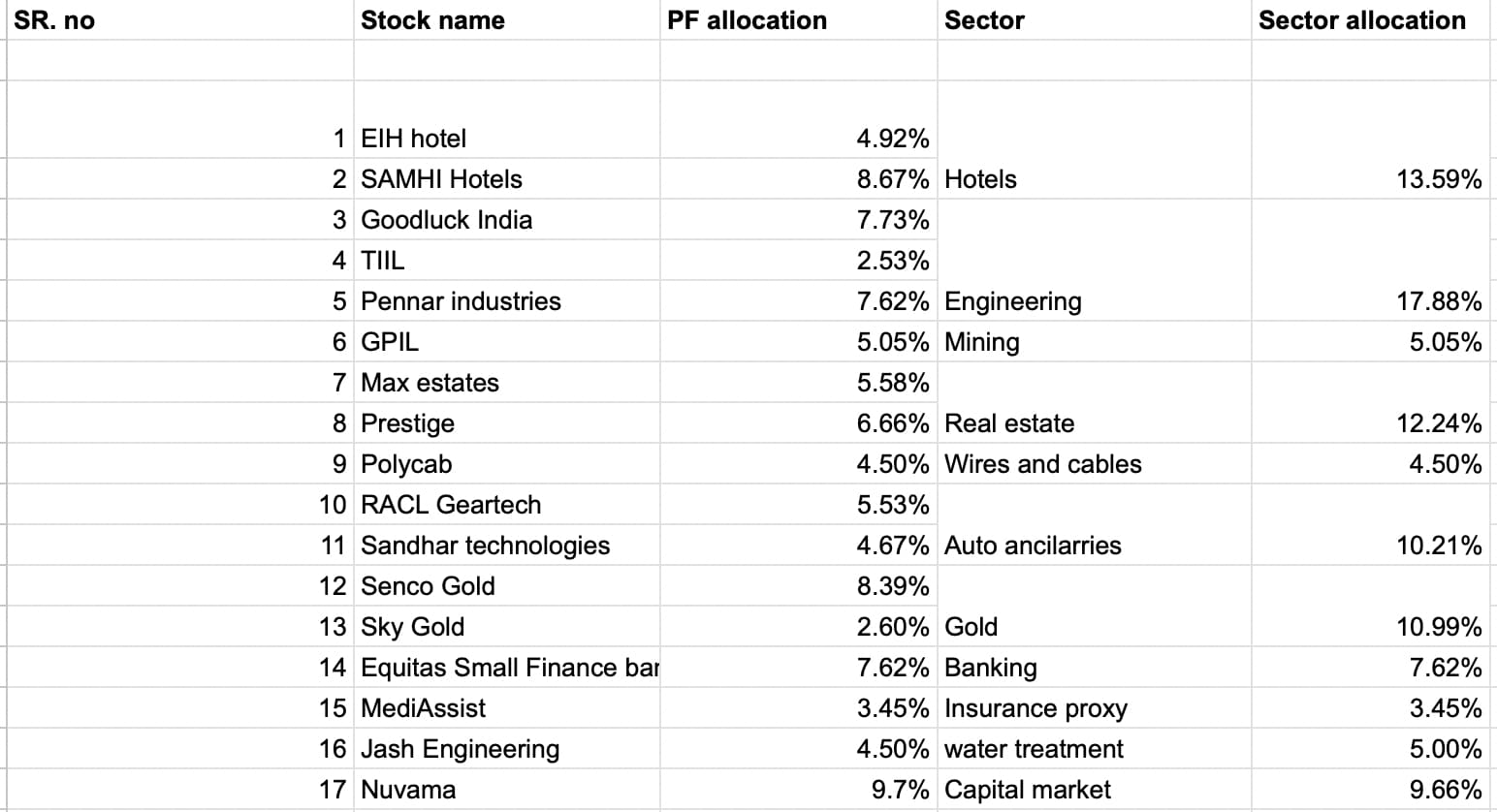

Added significantly in Hotels and Goodluck,Prestige during the election fall and Pennar after its results. Mainly because the thesis is getting priced right in hotels and the guidance Is very strong for the other with good margin of safety. Prestige is in solid momentum and the growth is intact, correction gave good valuations at around Mcap/presales of 2-2.5x

EIH deserved a higher allocation and got it right after the election correction

You might notice a small drop in the other positions its because I added fresh capital and did not take a basket approach to it.

Anyways, here are my potential worries ahead.

Samhi: it’s a turnaround bet and hence can go wrong. Which is why it concerns me that it’s a high allocation idea. Its going well so far and the prices I got while adding were very good and hence feel good about it but its a potential worry.

Auto anc dilemma: I consider Sandhar a better business than RACL yet RACL has a higher weitghage. It’s my bias because I studied RACL first. I will probably correct it and adjust accordingly

TIIL: great business but I am already playing the theme with 2 good business. Do I even need it with such low allocation? even if it does great I cant do much and I am 100% invested right now so would prefer it.

Also, Missed airman and Welspun. Had mentioned above wanted to study them and see what to do.Arman looks good but out of cash rn. Welspun is a bit expensive for me.

Bhagiradha Chemicals & Industries Ltd – Growing AgroChemical Company (06-06-2024)

- Recently, a bulk deal by Derive Trading and Resort Private Ltd which is owned by Radhakishan Damani.

Bull therapy 101-thread for technical analysis with the fundamentals (06-06-2024)

Ceinsys:

Timeline for the above is within 3 Yrs after cash is raised.

Upfront they get 25%, rest would come within 18 months incase rights are exercised.

Garware: How to track this data point? Is it specific to the business or general polyfilms?

Sula vineyards – pioneers in indian wines (06-06-2024)

IMO It doesn’t look like 8Cr. It’s a ratio which means it could be 8100 times median salary.

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (06-06-2024)

InvIT REIT are strcutured product based on Cashflow. So Depreciation -Amortisation charge, which are major P&L item, are non-cashflow item. Since in equity, corporate is assume to run indefinite, it would need capex to surivive and grow and hence Maintenance Capex and Working capital requirement are deducted from Profit to calculate free cashflow to equity owners. However, Hybrid products (InvIT/REIT) work on current assets which are already financed from debt/equity mix and are owned. For instance, IRB InvIT have right to collect for say 15 years for Toll assets which is valued say Rs 90. So every year, as per accounting policy, there would be amortication charge of Rs 6. However, the InvIT has already paid for same. Future acquisition in IRB InvIT or any REIT/InvIT would be funded be new unit issuance or fresh debt . Hence, accounting proft or loss (after charging depreciation/amortisation) would be misleading. Hence, better way to look at Cashflow (defined as Net Distributable Cash flow or NCDF). The calculation of cashflow exclude cash avaiable from assets, less operating and maintance cash expenditure, less interest and principle payable to third party (for InvIT/REIT colnsolidated) and to parent (for InvIT REIT standalone subsidiary which normally cancell out on consolidation). Since future acquisition would be funded by new debt/equity mix, the current cashflow shall be look at net available cash (net of interest/princiapal repayment of exisiting loan and not depreciation which is accounting charge). or NCDF to get better perspective.

Hope these answer your query.

Please not that I am not REIT/InvIT expert and my understanding may be wrong.

Disclosure I am not SEBI Registerd advisor. I am not suggesting any investment action in REIT/InvIT. I have invested in IRB InvIT/India Grid InvIT/ Embassy REIT and Brookfield REIT. My view may be biased due to my investment. I am increase/decrease/exti from InvIT/REIT investment without informing forum.

Maithan Alloys Ltd (06-06-2024)

The co. has 1,788 Cr in investments, mostly in equities which they bought in the last few months. Full year revenue was 1729Cr. with a OPM of 7%. The margins are closer to the lowest margins the company has witnessed in last 10 years. They have switched on the furnace at Impex, which was turned off due to unviable operations. I guess the cycle must be turning, very low margins+starting the furnace. If I remove the investments from the m.cap (3300cr)…then the business which is debt free, is available at 1500 cr, thats P/S of 0.87 and could be a good investment idea.

What I dont like is the mgmt’s unwillingness to distribute the cash to the shareholders. They have made massive equity investments which they should not have done, unwise capital allocation.

Disc: very small allocation, not an advise