Was trying to convey same point … does producing only ethanol gives them some comparative advantage , as it will be expected having more favourable position compared to sugar ???

Posts tagged Value Pickr

Hariom Pipes Ltd: A Capex Play! (04-11-2024)

You are right thank you

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (04-11-2024)

Would you not want to give a higher PE to some big names in the industry because of Ethanol production?

Not disagreeing with you that sugar industry will still be very cyclical in nature. One bad year of sugarcane produce at the farm level would mean a significant revenue hit, at high valuations it would lead to trouble.

Hariom Pipes Ltd: A Capex Play! (04-11-2024)

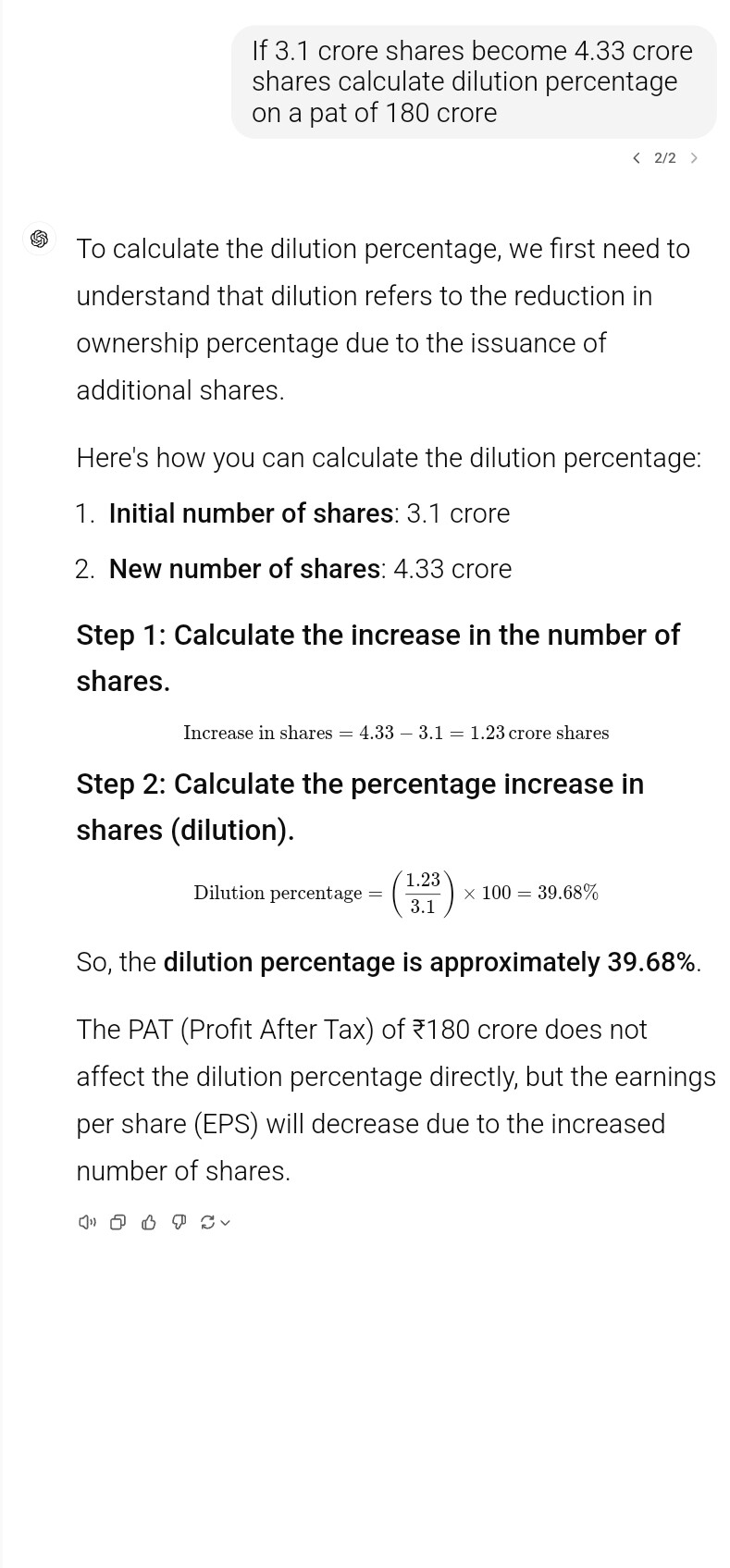

Can you please help me with this calculation.

If 3.1 cr shares become 4.33 cr shares how is it 40 percent dilution

MapMyIndia – The Map Company (04-11-2024)

Hello, for those invested here, what do you think about the current valuations of the company ?

Jindal Drilling – Beneficiary of a sustained offshore upcycle? (04-11-2024)

Thanks for the detailed thread @nirvana_laha .

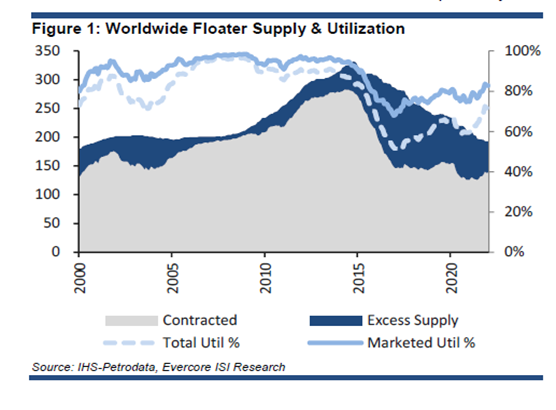

I have done some work on the largest offshore drilling operator (Transocean) which operates Ultra Deepwater floaters (UDW) and semi-subs. I agree the supply side of the market in offshore drilling has tightened with almost no new drillships being ordered in last 8 years.

-

Do you have a view on longevity of the cycle for jackups? In UDWs, the last cycle lasted for almost 10 years with utilization being above 90% which peaked in 2014 for reasons you have already mentioned above. It is important to see how long can these elevated earnings last.

-

Do you know how the current day-rates stack up vs the last upcycle? In UDWs, day-rates had touched $600k/day for high spec rigs in 2014. However, in the current cycle, we are seeing day-rates just levelling at those levels and no higher for contracts which are being signed for 2026-27. I would have expected day rates to be at-least 20-30% higher if we just adjust for inflation and also keeping in mind that the current fleet of rigs is much higher spec (8th gen now vs 6/7th gen in last cycle). Do you see significant upside in day-rates in jackups from where they currently stand because the cash flows will look very different then.

-

How does the current orderbook in jackups look like and where do day-rates have to be to incentivize new-builds? I’m looking at the current day-rates of average 80k and if I assume 40% EBITDA margin, that would be (80k * 365 *0.4) $13mm of annual EBITDA for a jackup which costs $200mm, i.e. 6.5% annualized returns which are below cost of capital. So my preliminary understanding is for rates to be much higher with a higher visibility on contract duration to incentivize any newbuilds. So either supply will remain constrained or day-rates increase materially which should both be positive for Jindal Drilling.

I also see that the operating margins have gotten materially impacted year on year despite increase in revenue which seems odd given the operating leverage.

Time technoplast (04-11-2024)

major effect of QIP on stock price:

Just trying to understand the major effect of QIP on stock price, I came across following major points. Hope it will help other new investors as well:

-

Dilution: Issuing new shares can dilute the value of existing shares, which might lead to a decrease in stock price.

-

Market Perception: If the QIP is oversubscribed, it indicates strong investor confidence, which can positively impact the stock price.

-

Use of Proceeds: The impact also depends on how the raised funds are used. If used for growth initiatives or debt reduction, it can lead to positive market sentiment and a rise in stock price.

-

Discounted Pricing: If shares are issued at a discount, it might signal lower demand, potentially causing the stock price to fall.

feel free to add if any other major impacts are left.

Solex Energy – Undervalued Solar PV Manufacturer or Microcap Value Trap? (04-11-2024)

Management proving latest updates and guidance in the below Investor connect:

Solex Energy Ltd. & Arihant Capital | Bharat connect conference – Rising Star September 2024

FY25 revenue guidance is 800cr, more than double from FY24. Also, the 1.5GW module line will be running on full capacity for Q4’25. By June next year, they are aiming to bring online the entire 4GW module capacity, and by mid CY26, the cell line should also begin which will be entirely captive for their own modules.

As per management, 4GW module line can translate to 4000cr of annual revenue runrate (given prices don’t fall). Their target is 9-11% margins. Cells will boost margins once available.

Disc: Invested and biased

EFC – Entrepreneurial Facilitation Centre (04-11-2024)

We work had big corporate governance problem as well, I am sure if somebody would do some google they would find , as to how promoter was building wealth form himself. +

They expanded to various unrelated industries like We live etc etc , on the other had we have EFC one of the most prudent spenders with the highest profitability in the industry. Not a fair comparison at all

EFC as on date is not into just coworking they do D&B and furniture as well do we have 3 verticals.

The most important part is they are the only company to get SM REIT approval of 500cr and in SM REIT I have to bring in income generating properties so EFC existing properties would be put in here. The real estate cycle right now is so strong that if we don’t have a problem for the next 3yrs we don’t know what the mix of EFC would be at that point

As per my understanding maximum would be bought in REIT, there I am replacing the landlord so where is the question asset liability mismatch?

The promoter also prudently wishes to use debt as explained in my earlier post.

This industry is not about SL model or MA model it is about balance sheet strength EFC has the best balance sheet in the industry today, I mean at least 5-10 coworking players equity we will have to add to reach EFC equity

The meaning of balance sheet strength is every body will die before me and I will be the last on to die, I think if they are smart in a crisis they significantly increase their market share as all small once would die no doubt.

All the above are just concepts and nobody know how this would pan out all boils down to promoter execution capability and how profitability you can build the business

The only thing I am sure of is EFC would be among the last ones to die

can be wrong, thnx

IRB INVIT TRUST- new game in the town! (04-11-2024)

The current InvIT structure of IRB own 4 BOT and 1 HAM assets. So in case there is no futher asset additions, the trust would continue to distribute NCDF to unitholder. In case NCDF cashflow discounted value are higher than current market cap of unitholders, then unit holder would receive excess amount over NAV as dividend. In case the discounted value of cashflow is lower than current mark cap (due to lower traffic, frequent issue of farmer protest etc), and tenue of asset get over, the investor would have to write down undistributed capital outstanding at end of last assets and book loss. However, while there may be accounting loss, the likely loss of capital appear low probability to me.

Since listing in May 2017 to November 2024(including Sep24 quarterly distributon with declared but not disbursed), IRB has distributed Rs 68.35 per unit as distribution. Of these, nearly 71% portion came as interest distribution (Rs 48.35 per unit in agggregate), 28% portion came Capital redemption (Rs 18.88 per unit in aggregate) and 2% (Rs 1.12 pre unit in aggregate) distributed as Dividend. So, signficant portfion of cashflow are distributed as Non-capital redemption in form of Interest/Dividend and hence I see limited probabilty of cashflow based loss on investment.