Decent results if we look at YoY. With this it will now be available at a PE of around 22, why is the pessimism, is it because of the AI threat? Or has the impact of job cuts at DNEG has spooked the investors? Even Basillic Fly is available around 20 PE, seems like the market is not willing to give any premium to this whole sector.

Posts tagged Value Pickr

Arman Financial Services Ltd (30-05-2024)

Arman has the highest ROE amongst MFIs and this trend has more or less been sustained over the years. Can’t compare with MAS, which is more of a wholesaler for MFIs

Growth is more or less in line with CA and Satin, and on a smaller base. Arman grows its loan book conservatively, this has always been the case since Demonetization

Recent Growth has been driven by geographical and product expansion, into UP/Bihar new geographics and into MSME loans away from MFI, and now growing into LAP and Individual business loans. Management has been giving clear sequential numbers for each business in transcript and presentation.

Monte Carlo Fashions-Branded Apparel Stock at Good Valuation (30-05-2024)

I tend to disagree. Brand carries great aspirational value in Tier 2 and Tier 3 cities. Anyway no brand makes money from LFS and mall stores as rentals are extremely high and Metro guys buy in discount sales only .

Once you have sale, they will go to 4 floors etc.

One important thing that i have noticed with Monte Carlo is that their winter wear sizes and fits are designed for Indian population’s physical attributes which makes it popular.

My comments are based on experience from few stores in Tier 2 cities in Himachal and M.P.

Problem with Monte Carlo is that they are winter focused. I don’t know how they will address this issue but they need to find a solution.

Monte Carlo Fashions-Branded Apparel Stock at Good Valuation (30-05-2024)

(post deleted by author)

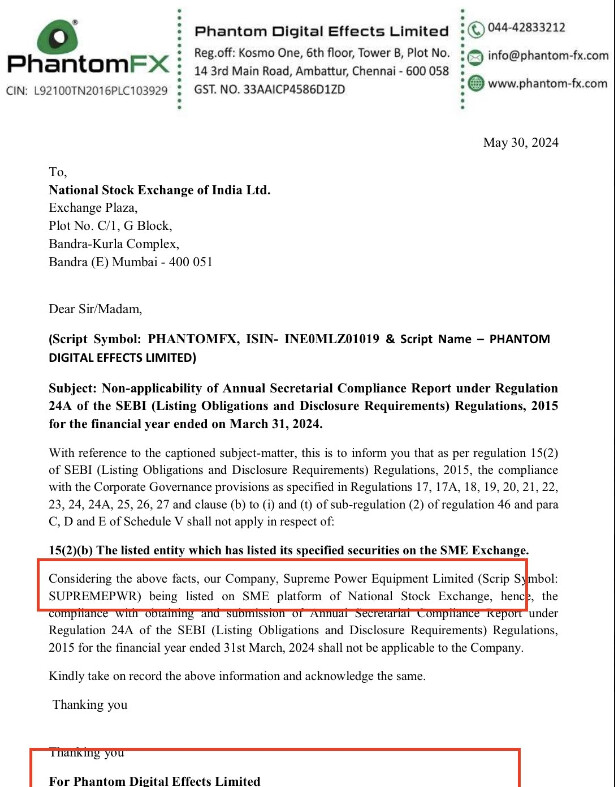

Phantom Digital Effects Limited (30-05-2024)

One VFX company messes up with the results (basic_mistake_lic) and rectifies it few days later after damage is done. This one uses template from different company.

Hope their VFX work is not all about copy/paste (errors)

Hitesh portfolio (30-05-2024)

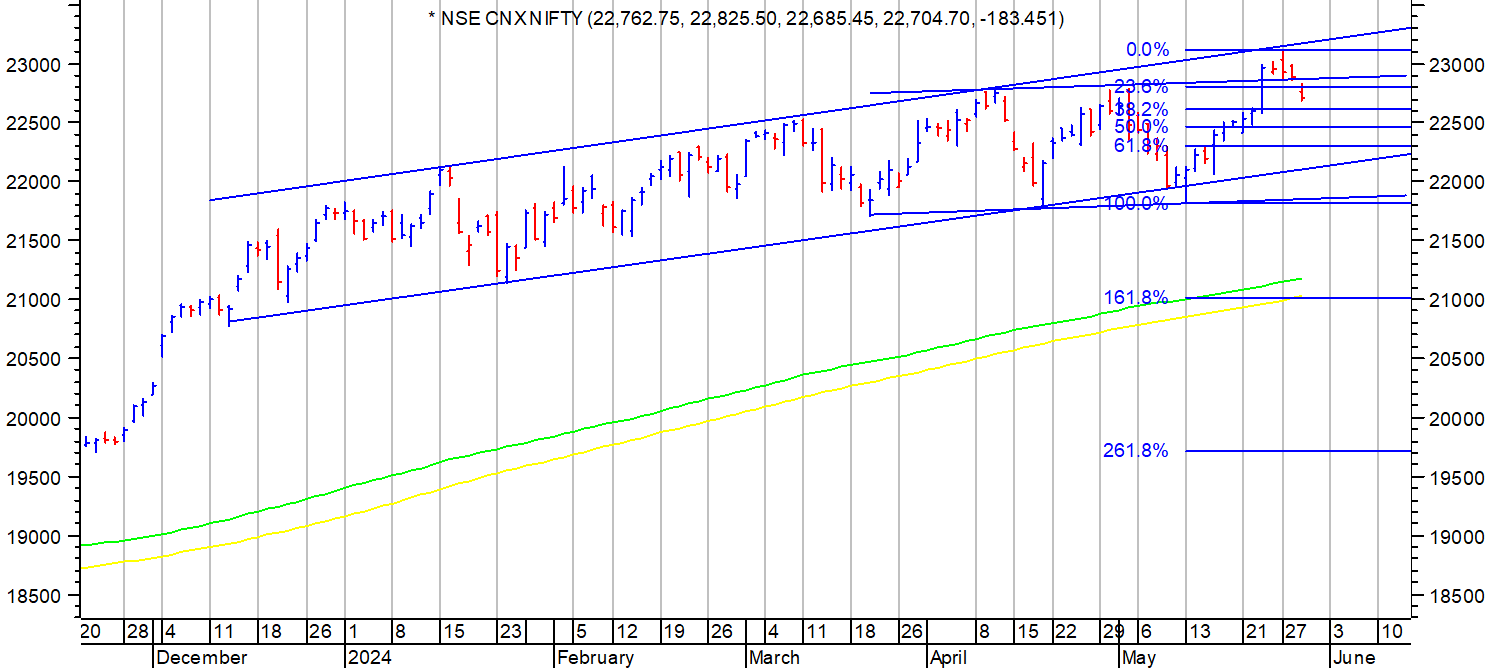

Over the last few days there has been a lot of nervousness and speculation about election results outcome. Markets have been on tenterhooks. Cat on hot bricks is an apt analogy to current markets.

To take away the noise, attached chart shows a rising channel within which Nifty has traded since Dec 2023. And in recent past we have had a triple bottom formation in range of 21700-800 with breakout and confirmation on clearing 22700-22800. Index made a swing high of 23110 on 27th May and has been in a corrective mode. Recent correction can be a retest after a breakout, or a failed breakout.

In either case, if double bottom plays out, we can be looking at potential target of 23700-23800 on Nifty depending upon election results However if we continue with correction, then levels of 22200-300 is rising channel support. Below that the previous triple bottom range support is at 21700-800. 22200-22600 is zone of retracement support wherein the 38.1%, 50% and 61.8% retracement levels of the previous rally are located.

If results are totally unexpected on either side, things can go wild on either side.

This is a totally objective chart of Nifty with well defined patterns, channels and levels. No recommendations, views. Just observing how things pan out. Hope for best and prepare for the worst.

Karan’s small/micro cap portfolio (30-05-2024)

While Mazda’s stock price has shown some volatility lately, it’s important to consider the bigger picture. The company remains debt-free, a significant advantage in the current environment. Additionally, valuations seem reasonable. Long-term, I believe Mazda’s future is promising, particularly with its well-managed engineering division.

Current Investment Strategy:

Despite my optimism about Mazda’s engineering potential, I’ve temporarily allocated capital elsewhere. This decision stems from concerns regarding the underperforming food division.

Here’s the crux of the issue: Capital allocation is split equally between engineering and food, yet engineering generates roughly four times the revenue. Ideally, I’d like to invest solely in the thriving engineering story. However, with equal capital going towards the food division, it dilutes the overall return potential.

Future Considerations:

If Mazda decides to de-merge the engineering division, I would be very interested in revisiting the investment opportunity. A separate engineering entity could unlock significant value.

Overall, while Mazda remains a company with long-term potential, the current capital allocation strategy creates a temporary pause on our investment.

Marksans Pharma- Can it be the next Pharma Biggie? (30-05-2024)

The export volumes were lower , Teva they have given incremental revenue guidance of 600 Cr for FY 25 . FY 24 revenue contribution was 50 Cr. The margin pressure is bcoz of some seasonality of products which would have to be dug in further , unfavorable forex – I don’t buy this , rupee has been stable despite good Q3 they said PAT is flat QoQ bcoz of some mark to mark losses but this time around rupee has been stable . Further higher employee cost bcoz of new hiring for new capacity . Let’s see what they have to say further about the result in con call.

Marksans Pharma- Can it be the next Pharma Biggie? (30-05-2024)

Not bad terrible numbers, but were expecting a little higher, EBIDTA took a hit due to red sea crisis and Teva requiring workforce.

Business still fundamentally strong and with a pipeline of 70+ new products, depending on how the product launches go and with Teva ramping up a topline of 3000 looks possible. Looking forward to the concall and management tone, generally Mark has always been conservative.

Disc: Not invested but tracking, not a recommendation.