A well thought out change. I think that you also need to widen your fishing area (cover more names) as well as find the fastest way to be in the best fishing spots (ongoing price bullishness), keeping fundamentals as the bedrock since a lot of questionable stocks go up during bullish sentiments. Best of luck.

Posts tagged Value Pickr

Shareholding pattern (26-04-2024)

Goodevening members,

How do you analyse the shareholding patterns/DII/FII investments to understand good investment opportunities??

I came across few fundamentally strong growth stocks ( as per my limited analysis knowledge) but found decreasing dii and fii pattern.

How do I seprate wheat from chaff!

Mudit’s Portfolio (Passively Active) (26-04-2024)

As anybody can see from my earlier posts , I was a Fundamental-oriented investor from start. Reading Annual reports, concalls, credit rating reports ,brokerage house reports, following news related with my portfolio companies, watching Management Interviews etc is what my M.O. for selecting and tracking the companies. I was never into technical analysis and never beleived into it…and even today also I don’t beleive more detailed technicals and I consider it as hoodoo.

And in last 2 years, when overall market was in strong bull phase ( and still is in)and even my mutual fund investments were giving very good returns, my direct stock portfolio was giving very very ordinary and disappointing returns. All my stocks were good. take Bajaj Finance, SRF, Pidilite, Divis Labs, Nestle, Tata Elxsi, LTI MIndtree, Kotak Bank, HDFC bank, Muthoot Finance etc. All are good quality companies and I was tracking them fundamentally and still Portfolio performance was so-so. And I was desperately finding the reason for my poor performance. And I came to know about Stage Analysis and read Stan Weinstein’s book…and it kinda opened my eyes.

Companies may be good quality , having moats, superior business models etc…but one thing was missing in my portfolio stocks and that one thing was momentum.

We make money, when share price of our companies go up …very simple truth…not when our companies make good profits , although that also can happen simultaneously.

First time when I started seeing Price and volume charts of my companies and it gave me a shock to see companies like Bajaj finance, consolidating for 2 years at a stretch , LTI Mindtree at same level for 1-2 years and I am blindly holding them , hoping that the price will appreciate soon, not understanding that there are currently more sellers for these stocks than buyers. Then I applied Stage analysis to all my stocks and when I entered into them and I was shocked that I was actually buying them either during consolidation or during their downtrend. That was the reason for my failure.

While those companies which I bought during stage 2 , uptrend like Trent, KEI, Polycab, have doubled in just 1 year or so.

We need to understand that share price of our stocks will increase when more people buy our companies and in large quantities. And such buyers are invariably big players, either promoters or Institutional investors, insiders. And we have to agree that they have informational advantage over us. We would like to think that there is no insider information or informational asymmetry but in practical world everybody knows that we are the last people to get any information about our companies. All results, all critical information first goes to big guys. And if they act on that information, it will be seen in the chart on price and volume. So we cant know the exact info but we can piggyback these big guys by following this price and volume action. Thats the only option we have. Ultimately all information will translate into price. Then why not track the price?

And I am not talking of trading here. Investing by piggybacking big investors through the price-volume action…Thats Momentum.

Then I started applying Stage 3 and stage 4 rules to my failed investments like Laurus labs, Divis Labs, LTI Mindtree and came to know that had I applied stage 3 rules, I would have exited these stocks much much earlier thus saving myself from big losses. And also by avoiding consolidation phases, I would have deployed my funds in growing stocks. So most important thing I realised is to avoid stage 3 and stage 4 stocks and if any of my stocks enter in such stages, I would exit at earliest.

Mudit’s Portfolio (Passively Active) (26-04-2024)

As anybody can see from my earlier posts , I was a Fundamental-oriented investor from start. Reading Annual reports, concalls, credit rating reports ,brokerage house reports, following news related with my portfolio companies, watching Management Interviews etc is what my M.O. for selecting and tracking the companies. I was never into technical analysis and never beleived into it…and even today also I don’t beleive more detailed technicals and I consider it as hoodoo.

And in last 2 years, when overall market was in strong bull phase ( and still is in)and even my mutual fund investments were giving very good returns, my direct stock portfolio was giving very very ordinary and disappointing returns. All my stocks were good. take Bajaj Finance, SRF, Pidilite, Divis Labs, Nestle, Tata Elxsi, LTI MIndtree, Kotak Bank, HDFC bank, Muthoot Finance etc. All are good quality companies and I was tracking them fundamentally and still Portfolio performance was so-so. And I was desperately finding the reason for my poor performance. And I came to know about Stage Analysis and read Stan Weinstein’s book…and it kinda opened my eyes.

Companies may be good quality , having moats, superior business models etc…but one thing was missing in my portfolio stocks and that one thing was momentum.

We make money, when share price of our companies go up …very simple truth…not when our companies make good profits , although that also can happen simultaneously.

First time when I started seeing Price and volume charts of my companies and it gave me a shock to see companies like Bajaj finance, consolidating for 2 years at a stretch , LTI Mindtree at same level for 1-2 years and I am blindly holding them , hoping that the price will appreciate soon, not understanding that there are currently more sellers for these stocks than buyers. Then I applied Stage analysis to all my stocks and when I entered into them and I was shocked that I was actually buying them either during consolidation or during their downtrend. That was the reason for my failure.

While those companies which I bought during stage 2 , uptrend like Trent, KEI, Polycab, have doubled in just 1 year or so.

We need to understand that share price of our stocks will increase when more people buy our companies and in large quantities. And such buyers are invariably big players, either promoters or Institutional investors, insiders. And we have to agree that they have informational advantage over us. We would like to think that there is no insider information or informational asymmetry but in practical world everybody knows that we are the last people to get any information about our companies. All results, all critical information first goes to big guys. And if they act on that information, it will be seen in the chart on price and volume. So we cant know the exact info but we can piggyback these big guys by following this price and volume action. Thats the only option we have. Ultimately all information will translate into price. Then why not track the price?

And I am not talking of trading here. Investing by piggybacking big investors through the price-volume action…Thats Momentum.

Then I started applying Stage 3 and stage 4 rules to my failed investments like Laurus labs, Divis Labs, LTI Mindtree and came to know that had I applied stage 3 rules, I would have exited these stocks much much earlier thus saving myself from big losses. And also by avoiding consolidation phases, I would have deployed my funds in growing stocks. So most important thing I realised is to avoid stage 3 and stage 4 stocks and if any of my stocks enter in such stages, I would exit at earliest.

KP Energy – Lotus in muddy water (26-04-2024)

If any one tracking can share recent orderbook how much is executed and in pipeline

Thank you

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (26-04-2024)

The opportunity looks interesting with the management aiming to achieve INR 130Cr EBITDA in FY ’25. With 190 Cr of Debt and INR 720 Cr Market Cap, that makes the valuation reasonably attractive at ~7.5x FY ’25 EBITDA. However, there are a few questions I had, if anyone has had a chance to look at these :

-

Is the Orchid Hotel, Mumbai owned by the promoter entity Plaza Hotels Pvt Ltd (PHPL)? The company presentation says it is an ‘owned’ hotel but Plaza Hotels’ annual report says that it has been given for management and operation to KHIL and is owned by PHPL.

-

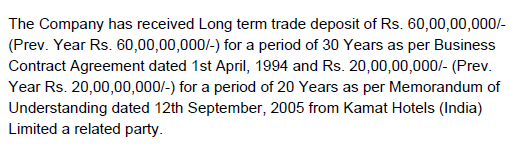

INR 80Cr of long-term trade deposits have been given by KHIL to PHPL interest-free. INR 60Cr was given for a period of 30 years in 1994 and INR 20 Cr was given for a period of 20 years in 2005. They should be up for renewal in 2024-25, if there has been any update on this.

-

KHIL paid INR 3.6 Cr of royalty expense to Plaza Hotels Pvt Ltd in FY ’23, for the leasehold land. How are these payments determined? Are they based on a % of revenue or are these fixed payments each year?

-

22 Cr loan (from the NCDs raised in Jan ’23) was given to Plaza Hotels Pvt Ltd by KHIL. KHIL received an interest of INR 80L on this in FY ’23. It is unclear why the loan was given and what is the rate of interest being paid to KHIL by promoter entity (PHPL).

- Contingent liabilities: As per clause 45.3 of FY ’23 AR, there are INR 60 Cr of contingent liabilities relating to a tax demand which have not been provided for. Couldn’t find much details about the tax demand.

I’ve also posed these questions to the IR. Awaiting their response, but it will be helpful if anyone has already spent time on this diligence.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (26-04-2024)

The opportunity looks interesting with the management aiming to achieve INR 130Cr EBITDA in FY ’25. With 190 Cr of Debt and INR 720 Cr Market Cap, that makes the valuation reasonably attractive at ~7.5x FY ’25 EBITDA. However, there are a few questions I had, if anyone has had a chance to look at these :

-

Is the Orchid Hotel, Mumbai owned by the promoter entity Plaza Hotels Pvt Ltd (PHPL)? The company presentation says it is an ‘owned’ hotel but Plaza Hotels’ annual report says that it has been given for management and operation to KHIL and is owned by PHPL.

-

INR 80Cr of long-term trade deposits have been given by KHIL to PHPL interest-free. INR 60Cr was given for a period of 30 years in 1994 and INR 20 Cr was given for a period of 20 years in 2005. They should be up for renewal in 2024-25, if there has been any update on this.

-

KHIL paid INR 3.6 Cr of royalty expense to Plaza Hotels Pvt Ltd in FY ’23, for the leasehold land. How are these payments determined? Are they based on a % of revenue or are these fixed payments each year?

-

22 Cr loan (from the NCDs raised in Jan ’23) was given to Plaza Hotels Pvt Ltd by KHIL. KHIL received an interest of INR 80L on this in FY ’23. It is unclear why the loan was given and what is the rate of interest being paid to KHIL by promoter entity (PHPL).

- Contingent liabilities: As per clause 45.3 of FY ’23 AR, there are INR 60 Cr of contingent liabilities relating to a tax demand which have not been provided for. Couldn’t find much details about the tax demand.

I’ve also posed these questions to the IR. Awaiting their response, but it will be helpful if anyone has already spent time on this diligence.

Dhruv’s Portfolio: Comments Appriciated (26-04-2024)

Hey Saiguhan,

Thanks for the comments.

I completely align to this view, I entered it around 700 ish and got exited at 1000 ish, I moved that money to HDFC Life, I’m big on insurance as it is my proxy play to indian healthcare sector too.

Absolutely Agree with this one, My father also invest in the market, He has exposure to AMC’s like HDFC AMC with exposure upto 10% of the portfolio. I don’t like to have same stocks in both portfolio’s. Just a safety thing. I have my eyes open to stocks like CDSL, CAMS, BSE and some brokers and wealth management services. I don’t like the current valuation and I believe we are going to have slowdown in them with saturation of new users. I’m also looking for the small term downturn in markets and these companies would be most affected.

More of, I have increased my positions in cash and long term bonds, preparing myself for short term opportunities and looking to extend my positions in Kotak (I have exhausted myself i HDFC Bank positions of over 25% now in HDFC), Bajaj Finance and HDFC Life in Large caps and also increase exposure in small cap banks (small finance banks) and chemical sector.

So lot’s of action ahead! Looking ahead for further discussions. Would love to listen about your observation on different sector!

Dhruv’s Portfolio: Comments Appriciated (26-04-2024)

Hey Saiguhan,

Thanks for the comments.

I completely align to this view, I entered it around 700 ish and got exited at 1000 ish, I moved that money to HDFC Life, I’m big on insurance as it is my proxy play to indian healthcare sector too.

Absolutely Agree with this one, My father also invest in the market, He has exposure to AMC’s like HDFC AMC with exposure upto 10% of the portfolio. I don’t like to have same stocks in both portfolio’s. Just a safety thing. I have my eyes open to stocks like CDSL, CAMS, BSE and some brokers and wealth management services. I don’t like the current valuation and I believe we are going to have slowdown in them with saturation of new users. I’m also looking for the small term downturn in markets and these companies would be most affected.

More of, I have increased my positions in cash and long term bonds, preparing myself for short term opportunities and looking to extend my positions in Kotak (I have exhausted myself i HDFC Bank positions of over 25% now in HDFC), Bajaj Finance and HDFC Life in Large caps and also increase exposure in small cap banks (small finance banks) and chemical sector.

So lot’s of action ahead! Looking ahead for further discussions. Would love to listen about your observation on different sector!

Shakti Pumps – solar shakti (power)! (26-04-2024)

Very solid q4 numbers. Way above management guidance of 500crs revenues. Significant margin expansion because of low solar module prices!!!