Yes you’re right. For the one they announced they bid for it. Not finalized

Posts tagged Value Pickr

Syrma SGS an Export Substitution opportunity in EMS sector (30-10-2024)

As per the management the company will grow by 40-45% this fy and 35%+ for the next years to come.

Considering the management commentary, the company should do a revenue of around 8500cr by FY27.

Assuming EBITDA margin of 7% and PAT margin of 4% (base case), the PAT should be 350cr and EPS as 19INR.

Now, depends on the valuation given by the market, the share price can be anywhere from 1300 to 1500INR.

19 x 70 = 1300 (2.6x)

19 x 80 = 1520 (3x)

Considering the government push for the EMS sector and the large addressable global market, the market leaders are expected to grow at a very healthy rate for years to come. Now-a-days electronics components are the part for everything that we use, from automobile to consumer appliances, digital devices, etc. So, the TAM will only grow from here on.

There are many Chinese EMS companies such as Shenzhen kaifa technology, DBG Technology, etc. with Mcap over 30Billions USD. The biggest one in India is Dixon with Mcap close to 10Billion.

In India, the market leaders are Dixon, Kaynes and Syrma (cheapest valuation out of them). So, they all should grow for years to come.

Disc. This is a back of the envelope calculation, not a stock recommendation. Invested and biased

Holmarc Opto-Mechatronics – R&D play (30-10-2024)

Actually competetion is very low in this business because of govt. policy. Thanks to the post above on GeM Class-I Local Supplier lead, I was able to hunt down a bit more.

Govt. has been pushing govt. funded institutions to procude through the GeM portal and also insisting preference be given to MSE/MII (Medium/Small Enterprises / Make In India certified)

MII (Make in India) certificate can be procured only if you have > 50% localisation (Class-I) or 20-50% localisation (Class-II). Some tenders even seem to reduce margin of L1 if you are a MSE/MII (like within 15% of L1) or outright reject ones without MII cert. This is what seems to be giving Holmarc the advantage

As for reason for margins being down – its because hiring when capacity wasn’t ready. Last year the company went from 215 employees to 265 employees even as they were funds to come in to put up capex. This year again this 265 number has gone up to 335 and as I had highlighted, these people are currently being trained and yet to be productive since machinery is still being installed.

Margins won’t improve in H1 either though topline should go up. Hiring has continued and from 335 its now close to 350 (though pace has slowed while waiting for commissioning of equipment)

From H2 onward we should see sequential margin improvement as part of capex will be done for H2 and from H1, FY26 productivity should go up considerably when compared to FY25/FY24. As for sales, I am certain demand is robust going by tenders and exports.

These sort of businesses require patience and cannot be played from quarter to quarter as there’s no liquidity and spreads are huge. Over time though with policy tailwind, strong exports, it will do alright.

Disc: Invested

Krystal Integrated Services Ltd – Share Analysis – Facilities Management Services Industry (30-10-2024)

Some observation regarding RPT during concall

Madhur Rathi: So, just 2 final questions. Sir, our cash has reduced from Rs. 88 crores to Rs. 18 crores between the March quarter end closing and as well as this quarter end closing, as well as your loans have increased and mostly these are the related parties, they have increased from Rs. 72 crores to Rs.94 crores. If you could just explain this, sir.

Sanjay Dighe: It is basically the utilization of the IPO funds that were received, which has reflected in the numbers being a little different this time. I think while we talk to you in the next results call, you will find the numbers being very stable at that point of time.

Madhur Rathi: And sir, this loan that was provided to related parties, sir, so do we plan on reducing this? Sir, this has kept on increasing as we understand.

Sanjay Dighe: These are all short-term and we plan on reducing this.

Can someone clarify this in simple terms?

Srestha Finvest Ltd: A Strategic Shift Towards Green Finance and Sustainable financing (30-10-2024)

Any idea when will be result announcement and any idea do they will maintain profits same like last quarter

Microcap momentum portfolio (30-10-2024)

Hello @visuarchie, I have been following your threads for some time now. Thank you very much for sharing your system transparently.

Regarding value momentum, I find the concept of stage analysis to be very useful. When a stock from Stage 1 base has just broken out, it enters momentum territory(Stage 2). This is Value Momentum in a way. I have been using this framework for some time now and it has worked well for me. I don’t have a systematic framework around this but you may refer to Stage Investing thread on VP. You may also refer to this blog to understand how the system works Entry Exit Strategy in Stocks- Stage Analysis – Venus Alpha Capital . This strategy is based on Stan Weinstein’s book. He has illustrated it with a number of examples. Mind that if one uses this strategy, they have to be ruthless with selling.

Another way to do this would be identifying fundamental triggers in a business and when they play out, the stock enter momentum. Although, this is a more difficult approach as one needs deep insights in multiple businesses and sectors.

Bull therapy 101-thread for technical analysis with the fundamentals (30-10-2024)

I agree historically this hasn’t happened and probably won’t this time too but history doesn’t repeat but rhymes as they say. Pre 2008, capital goods, infra, manufacturing did quite well but post 2009, companies like page industries did very well and so on. When we look at different slices of history, smallcaps from different sectors have become midcaps/largecaps. There is a tendency for certain sectors to outperform others and this has more to do with what’s happening outside those companies as well though we tend to give them and their management all the credit.

Historically we havent had GDP growth without credit growth either – but now we are seeing govt. led capex even as private is sitting on lean balance sheets with cash – so there’s no credit growth though there’s GDP growth which is also confusing people.

So depending on how far back in history you go, you can always find some similarities to what’s happening currently. We have been a services and consumption driven economy in the recent 10-15 years which is why our Nifty today looks like this – heavy on financial services, fmcg, IT, Auto etc.

Our govt. has taken a bold step to tax heavily both direct and indirect and invest heavily in capex. This govt. driven capex is what is driving earnings in small/microcaps (To some extent midcaps too) but not in largecaps because these became large in the consumption driven economy in the first place (except a few like L&T, Cummins, Siemens, ABB etc). This has a precedent in a country like South Korea. I feel this is a fundamental shift in approach from the govt. and as long as this policy stance is in place, I will stand by what I said.

Why do I think this policy stance can continue? See the fiscal deficit print from today

Collections are higher, expense flat, capex is down (due to elections CoC, will pickup big time in H2 as we are seeing in tendering activity), < 30% of target for year means it will remain in control for full year. Our earlier concerns with this approach has been fiscal deficit and foreign capital fleeing and currency weakening and so on – now we have strong reserves, strong domestic flows if FIIs flee and deficits are well under control.

As long as there aren’t elections to win and votebase to appease, this might be the stance. What was nice was the govt. didn’t let up the stance even in election year which is telling us something. But this cannot come at the expense of consumption, so I would think a rate cut should come sooner or later which will ease consumption concerns (auto inventory, fmcg issues) but the govt. capex should resume full swing in H2.

So when people say correction is coming in smallcaps, the perception is that its completely driven by irrational flows. There’s always more to it when such simplified answers are provided. I think its a combination of govt. policy favoring these companies which were beaten down, the earnings driven performance bringing in more capital and of course the eventual fomo driven expensive valuations in some pockets – but as long as the policy stance remains intact there will be adequate spaces to fish in for a bottoms-up investor imo. As long as Nifty composition remains as it is, it may never reflect the actual economy which is a bit more accurately reflected in the smallcaps (re-rating is penciling in future growth as well, assuming policy stance continues, so of course it has overshot).

Equity capital is cheap as is evident from the number of QIPs and general market levels. Generally equity capital is more expensive than debt capital but the flood of equity capital has lowered perceived risk in equity causing this behavior. Nano/SME space – please read the dispatches some of these companies trading at 100x+ P/E or are loss-making are sending and check the noise on twitter or the buy calls on sms/telegram etc. Current rally being retail driven – I think you can see lot of supporting evidence on cnbc where they cover who sold/bought and how much retail is buying etc.

I think that’s enough with the macro gyan which is more likely to be wrong depending on how far from the future you look back at.

As for where I have put my money in, so far 3 results are out and all are stellar –

I have done some research on ceinsys and have added those inputs in the geospatial thread and the ceinsys thread. This one seems to be getting better and better, the more we unravel. Nothing new on Wockhardt as we wait for trials to complete in the next couple of months. Hopefully results in these two also would show good trajectory.

Other than this, have taken a new bet on Holmarc – covered in the Holmarc thread. Its a purely fundamental bet but technicals also look quite strong with a year long consolidation with volatility contraction and a breakout this month.

Disc: Have positions in all names mentioned. I am not qualified to advise.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (30-10-2024)

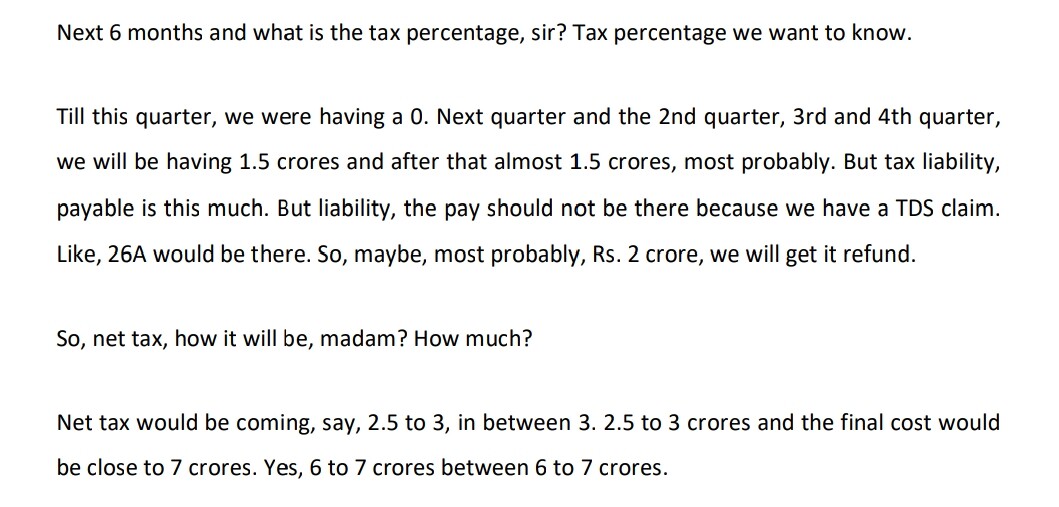

For interest cost it should be 6.3cr for H2 maybe they are rounding off.

For the taxes there was again a comedy.

So 2.5-3 + 2.5-3 = 6-7 (not 5-6). Also what about -2? And what was this 1.5?

At this point, I am just waiting for a strong enough reason to exit but I do think that the H2 will be good.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (30-10-2024)

Actually they said they will do 100cr ebitda in FY25 and H2 margins will be at 30%. Haven’t seen a more confused management when it comes to numbers