Is anyone aware of the list of water treatment players operating in the private space?

Posts tagged Value Pickr

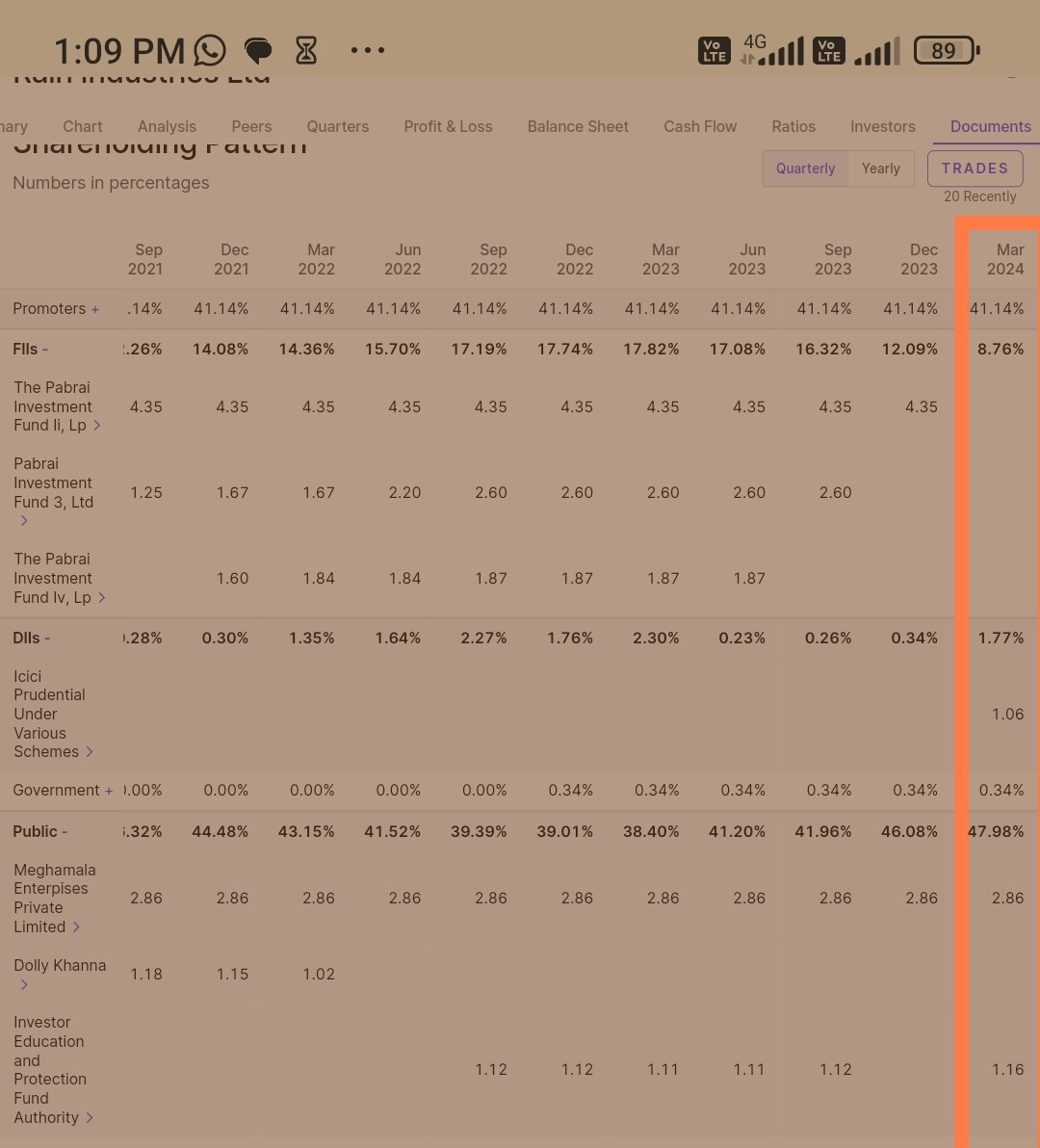

Rain Industries – An oversold de-leveraging play (10-04-2024)

Pabrai has exited Rain Industries completely in March quarter, this time no notification from the co.

An expected move from Pabrai.

Good thing is most of the selling got consumed without much(any) downside on the share price.

Gulf oil demerger (10-04-2024)

Hello members,

My first post here.

Was doing some back of the envelope calculations on the land value. GOCL claims it will sell 264 acres for Rs. 3,402 crores, which works out to around 12.88 cr/acre.

The going rate as per property websites is between Rs 40-55 cr/acre.

Even at Rs 13cr/acre the company looks attractive, but was wondering if there’s something fishy, or if there’s a rational explanation for the underpricing.

On another nots, I observe that GOCL lost its case against Udasin Mutt both in the High Court, and in the Supreme Court (in 2023).

Rrp s4e innovation pvt ltd (10-04-2024)

RRP S4E INNOVATION PVT LTD (Defence sector manufacturing company)

![]() How is this company fundamentals

How is this company fundamentals

![]() Feedback

Feedback

![]() UNLISTED SHARES

UNLISTED SHARES

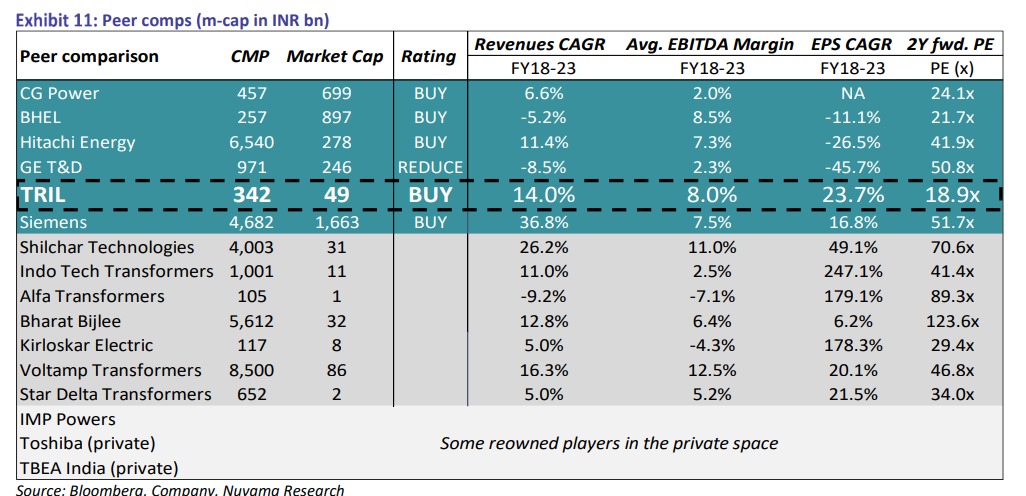

Transformer & Rectifier India Limited (10-04-2024)

Page 5 is quiet funny,especially where Nuvama has given projections for the names out of their coverage. According to the analyst: Shilchar’s earnings are going to halve or fall even more,BBL’s earnings are going to fall by 75%,Star delta’s earnings are going to fall by 50-60% over the next 2 years and so on! All this while TRIL is going to have breakneck growth mostly due to low base of FY24(owing to various company specific issues)

Analyst seems to have extrapolated the revenue CAGR of Fy18-23 for all these names and extrapolated the exact margins. Thus,11% in Shilchar’s case,2.5% in Indo tech’s case,5% for Star,etc. seem to have been extrapolated. I doubt anyone would be so ill-informed to think that only one company(TRIL) with no particular niche is going to make 14-15% EBITDA while the rest are not going to have any margin expansion. The current numbers are already way better than extrapolated in the report. Other than Shilchar that derives major revenues from exports & thus makes margins head & shoulders above the rest,the sector is mostly homogenous & it’s not possible that only one company is going to benefit from power demand in the country & globally. Moreover,the pref & 500 cr QIP will lead to further dilution in TRIL’s case.In the meantime,no other transformer company has come to the markets to raise money.Even the ailing Alfa that turned around only this year has not raised money…so far atleast.

But other than somehow proving that TRIL is the cheapest name in the sector,the report was good.

Disc.: Not invested in TRIL…views maybe biased.

Walchand Peoplefirst Ltd Dale Carnegie master franchisee (10-04-2024)

Walchand Peoplefirst Ltd is listed on BSE (BSE Code 501370). They have a market cap of Rs.64 crores. CMP Rs.221.

Their website is https://www.walchandpeoplefirst.com/.

Walchand Peoplefirst is a corporate training company. They are master franchisees of Dale Carnegie Institute. They recruit other franchisees in tier 2 and tier 3 cities. Dale Carnegie was the author of ‘How to win friends and influence people’, a bestselling book which has a cult following. In 2022 they became master franchisees of Dale Carnegie Institute and will now be recruiting franchisees themselves. As per the 2023 AR, they have taken Rs.10 lakhs as franchise fee.

They opened a Franchise in Pune recently:

They are expanding.

I found a video about them. Start watching from 3:05 because till then they are talking of Dale Carnegie and not Dale Carnegie India.

Dale Carnegie India: The Full Story

On their website they claim to have ‘8,500 + clients including top Government, Corporate, Education and Social sectors.’ and claim thave trained over

650,000 people.

They teach soft skills, which I think are going to be in demand even after a lot of other areas are automated by AI.

They have two independent directors who have a good profile – H. N Shrinivas and Jehangir Ardeshir. Both have worked with the Tata Group in senior positions.

Their sales have been stagnant for the last decade. From Rs.17.18 crores in FY13 to Rs.17.81 crores in 2023. In FY21, they reported losses.This seems to have been because of Covid and the lock down. Their training was mainly in person. Now their training is also online and they are profitable.

They own a building on Ballard Pier, South Mumbai named Construction House. The parent company is Walchand & Co Pvt Ltd. The land (806 square metres) on which the building is built is leased from Mumbai Port Trust is in the name of the company.

Mumbai Port Trust:

See serial no 516. Land admeasuring 806.86 square metres in name of Walchand Capital Ltd (old name of Walchand Peoplefirst Ltd).

This company was incorporated on 1920-07-06.

This is the building, specs and picture:

https://property.jll.co.in/office-lease/mumbai/ballard-estate/construction-house-ind-p-001akg

As of March 31, 2023, they had cash and investments of over Rs.25 crores and debt of less than Rs.6 crores. So net Rs.19 crores cash. Their net profit so far this year has been Rs.2.4 crores. I do not know their current cash position.

The concerns:

Their company secretary quit recently.

Management remuneration has been higher in recent years. The two main directors themselves take about Rs.3 crores as their salary.

They spent on buying an expensive car in FY23.

In recent years, even in FY23, a lot of their profit is from ‘other income’. Without this, they would be in losses.

What is the value of their land and building at Ballard Pier? Can they monetize this?

When will they become profitable?

Why are they into losses despite being the master franchise of a world known brand and being a service company?

Disclosure: I have invested in the stock of this company. This is not a recommendation.

Walchand Peoplefirst Ltd Dale Carnegie master franchisee (10-04-2024)

Walchand Peoplefirst Ltd is listed on BSE (BSE Code 501370). They have a market cap of Rs.64 crores. CMP Rs.221.

Their website is https://www.walchandpeoplefirst.com/.

Walchand Peoplefirst is a corporate training company. They are master franchisees of Dale Carnegie Institute. They recruit other franchisees in tier 2 and tier 3 cities. Dale Carnegie was the author of ‘How to win friends and influence people’, a bestselling book which has a cult following. In 2022 they became master franchisees of Dale Carnegie Institute and will now be recruiting franchisees themselves. As per the 2023 AR, they have taken Rs.10 lakhs as franchise fee.

They opened a Franchise in Pune recently:

They are expanding.

I found a video about them. Start watching from 3:05 because till then they are talking of Dale Carnegie and not Dale Carnegie India.

Dale Carnegie India: The Full Story

On their website they claim to have ‘8,500 + clients including top Government, Corporate, Education and Social sectors.’ and claim thave trained over

650,000 people.

They teach soft skills, which I think are going to be in demand even after a lot of other areas are automated by AI.

They have two independent directors who have a good profile – H. N Shrinivas and Jehangir Ardeshir. Both have worked with the Tata Group in senior positions.

Their sales have been stagnant for the last decade. From Rs.17.18 crores in FY13 to Rs.17.81 crores in 2023. In FY21, they reported losses.This seems to have been because of Covid and the lock down. Their training was mainly in person. Now their training is also online and they are profitable.

They own a building on Ballard Pier, South Mumbai named Construction House. The parent company is Walchand & Co Pvt Ltd. The land (806 square metres) on which the building is built is leased from Mumbai Port Trust is in the name of the company.

Mumbai Port Trust:

See serial no 516. Land admeasuring 806.86 square metres in name of Walchand Capital Ltd (old name of Walchand Peoplefirst Ltd).

This company was incorporated on 1920-07-06.

This is the building, specs and picture:

https://property.jll.co.in/office-lease/mumbai/ballard-estate/construction-house-ind-p-001akg

As of March 31, 2023, they had cash and investments of over Rs.25 crores and debt of less than Rs.6 crores. So net Rs.19 crores cash. Their net profit so far this year has been Rs.2.4 crores. I do not know their current cash position.

The concerns:

Their company secretary quit recently.

Management remuneration has been higher in recent years. The two main directors themselves take about Rs.3 crores as their salary.

They spent on buying an expensive car in FY23.

In recent years, even in FY23, a lot of their profit is from ‘other income’. Without this, they would be in losses.

What is the value of their land and building at Ballard Pier? Can they monetize this?

When will they become profitable?

Why are they into losses despite being the master franchise of a world known brand and being a service company?

Disclosure: I have invested in the stock of this company. This is not a recommendation.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (10-04-2024)

So it begins. Since Model code of conduct is ongoing, allottment and final decision is pending.

RIL and L&T lead. But Welspun looks a good bet if allottment gets confirmed.

Any thoughts @1957

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (10-04-2024)

So it begins. Since Model code of conduct is ongoing, allottment and final decision is pending.

RIL and L&T lead. But Welspun looks a good bet if allottment gets confirmed.

Any thoughts @1957

Oil India- has its time come? (10-04-2024)

Sure. But gain Execution, Pricing and other skills are important in Green Energy too. But yes money is here to be made. All a function of patience and timing.

But we are digressing from main OIL part of the thread. So I will stop here