Let’s explore Aditya Birla Fashion and Retail Ltd.’s diverse business areas, strengths, and areas of concern.

Business area of the company:

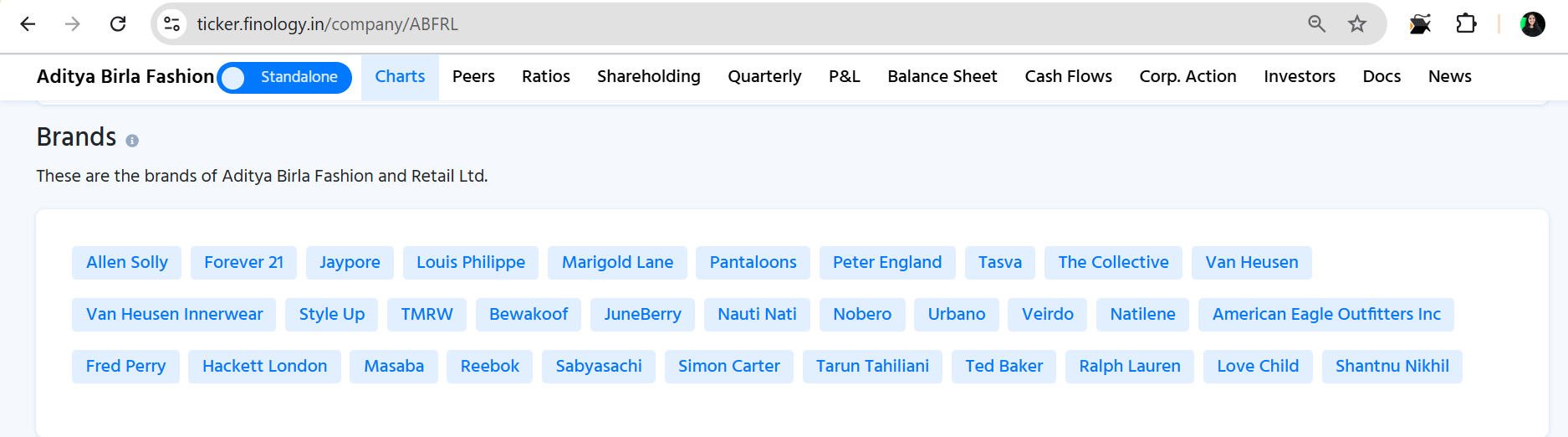

ABFRL is a prominent player in the Indian retail industry, known for its wide-ranging portfolio of brands. Let’s take a closer look at ABFRL:

-

Lifestyle Brands: It houses some of India’s most iconic names: Louis Philippe, Van Heusen, Allen Solly, and Peter England. These brands are market leaders within their respective segments. Their signature styles, high-quality products, and differentiated in-store experiences have earned them immense customer loyalty and recall.

-

Pantaloons: Pantaloons, India’s favorite fast fashion destination, caters to the modern Indian’s apparel and lifestyle needs. It offers a variety of house labels and national brands, spanning casual wear, ethnic wear, formal wear, party wear, activewear and Non-apparel.

-

Fast Fashion: In July 2016, ABFRL secured exclusive rights to the India network of California-based fast fashion brand, Forever 21. This partnership marked a significant milestone for ABFRL, positioning it as the largest integrated branded fashion player in India. The popularity of fast fashion among the country’s young demographics further fueled this achievement.

-

Notable brands in their portfolio include:

-

Van Heusen Innerwear: Offering comfort and style in innerwear.

-

Jaypore: Celebrating Indian decadence.

-

Shantanu & Nikhil: Representing modern grandeur.

-

Simon Carter: Part of their international business.

-

The Collective: India’s largest international multi-brand retailer.

(Image Source: Finology Ticker)

Using Finology’s Ticker platform we found some concerns in ABFRL’s business:

- Sales vs. Profitability: ABFRL seems to have shifted its focus toward sales growth, but at the cost of profitability. The graph shows increasing sales over the last 5 years, but profitability has taken a hit, resulting in losses in the past 3 years.

As investors, we need to closely monitor this trend. While growth is essential, sustainable profitability matters equally.

-

Interest Coverage Ratio (ICR): Despite having a debt-to-equity ratio below 1, ABFRL’s ICR is weak. An ICR below 1 indicates that the company’s earnings aren’t sufficient to cover its interest payments. This can be concerning.

Although ABFRL benefits from strong parentage, we should still pay attention to this observation. Remember the cautionary tale of Vi (Vodafone Idea) and its debt struggles. -

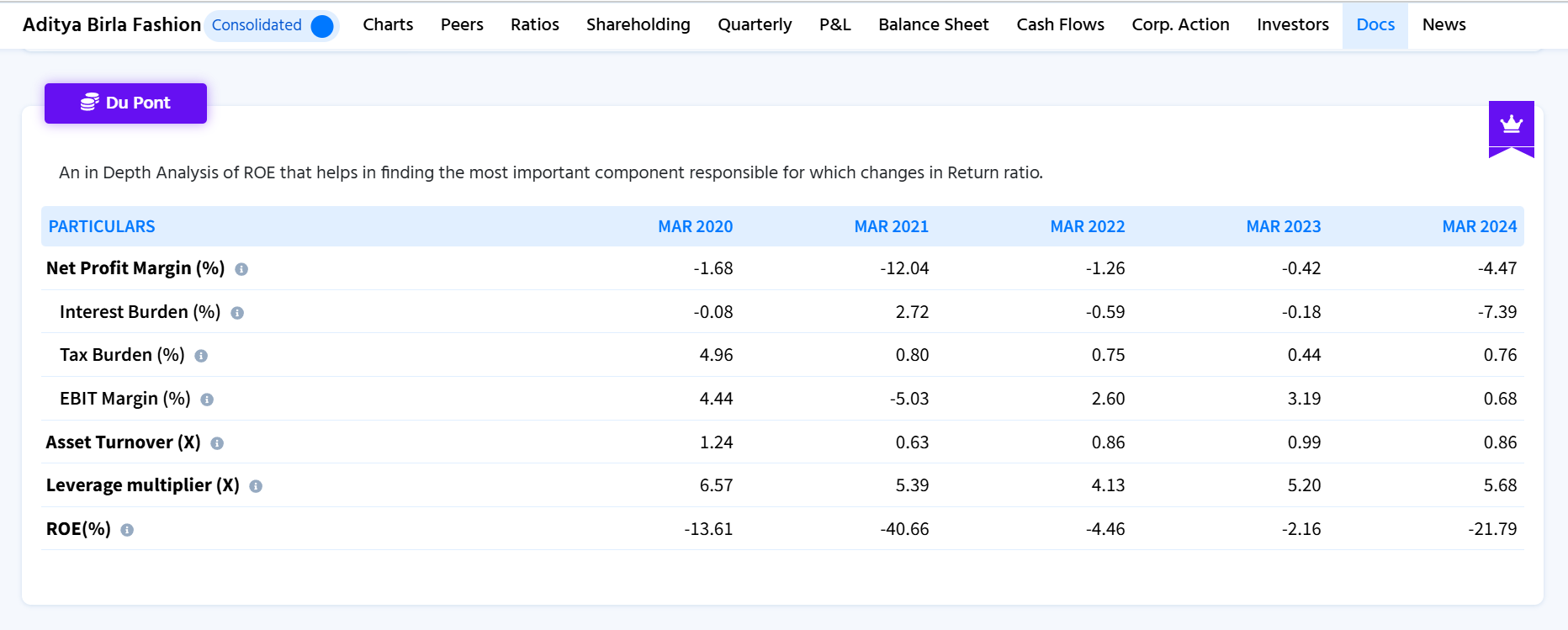

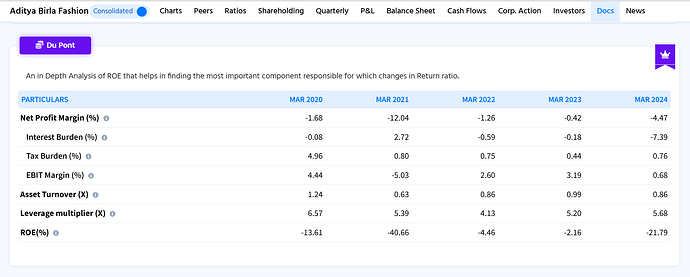

Du Pont Analysis: The drivers of ROE—profit margin, asset turnover, and leverage – reveal interesting insights:

- Profit Margin: Net margins have been poor over the last 5 years.

- Asset Turnover: A declining trend suggests inefficient asset utilization.

- Leverage: Indicates a debt burden on the company.

(Image Source: Finology Ticker)