i understand, but many Promoters prefer to do a buyback to avoid taxation, rather than Dividends which will put them at hishest tax level. Also they tender at last minute, just enough shares to keep at the 75% limit, based on shares that are tendered by other shareholders.

Posts tagged Value Pickr

Kilburn Engineering – Huge undervaluation (30-03-2024)

Management Guided for total consolidated revenues of Rs. 450-500Cr by FY-25 with 18-20% Margins easily achievable.

Also, the company will close this year with consolidated orderbook of Rs.310-320Cr and expects orders worth 150-200Cr to flow in first four months of FY 25.

Also, the management was bullish on ME Energy which can give better revenues as post consolidation Balancesheet Strength would increase which could help ME Energy bid for high value orders going forward.

Alufluoride Limited-conversion of waste into wealth (30-03-2024)

Sir, that looks like a rising wedge to me. I think a breakdown’s more probable.

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (30-03-2024)

In the recent concall,management is talking about the delay in the implementation of new education policy and hence the lack of proper demand in the market currently as the publishers are acting cautious.

Any update by when is this going to happen?I tried searching for the same on google but couldn’t find anything specific related to the education policy implementation.

Also,my another concern is(as already mentioned by one of the folk in this thread)that management is not planning any specific capex for raising the topline,i wonder if the management will be able to taste the fruits of the expected flood in demand in future.

Any comments on this please.

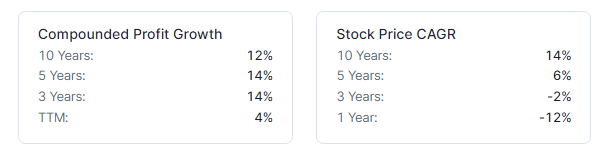

Hindustan Unilever (HUL) (30-03-2024)

In the past 3 years, profit has grown by 14% while stock price has compounded at -2%. Given that it’s HUL and points i mentioned earlier

HUL seems a good defensive, reasonably priced stock to me.

Counter views invited.

Thanks

Yogesh Portfolio (30-03-2024)

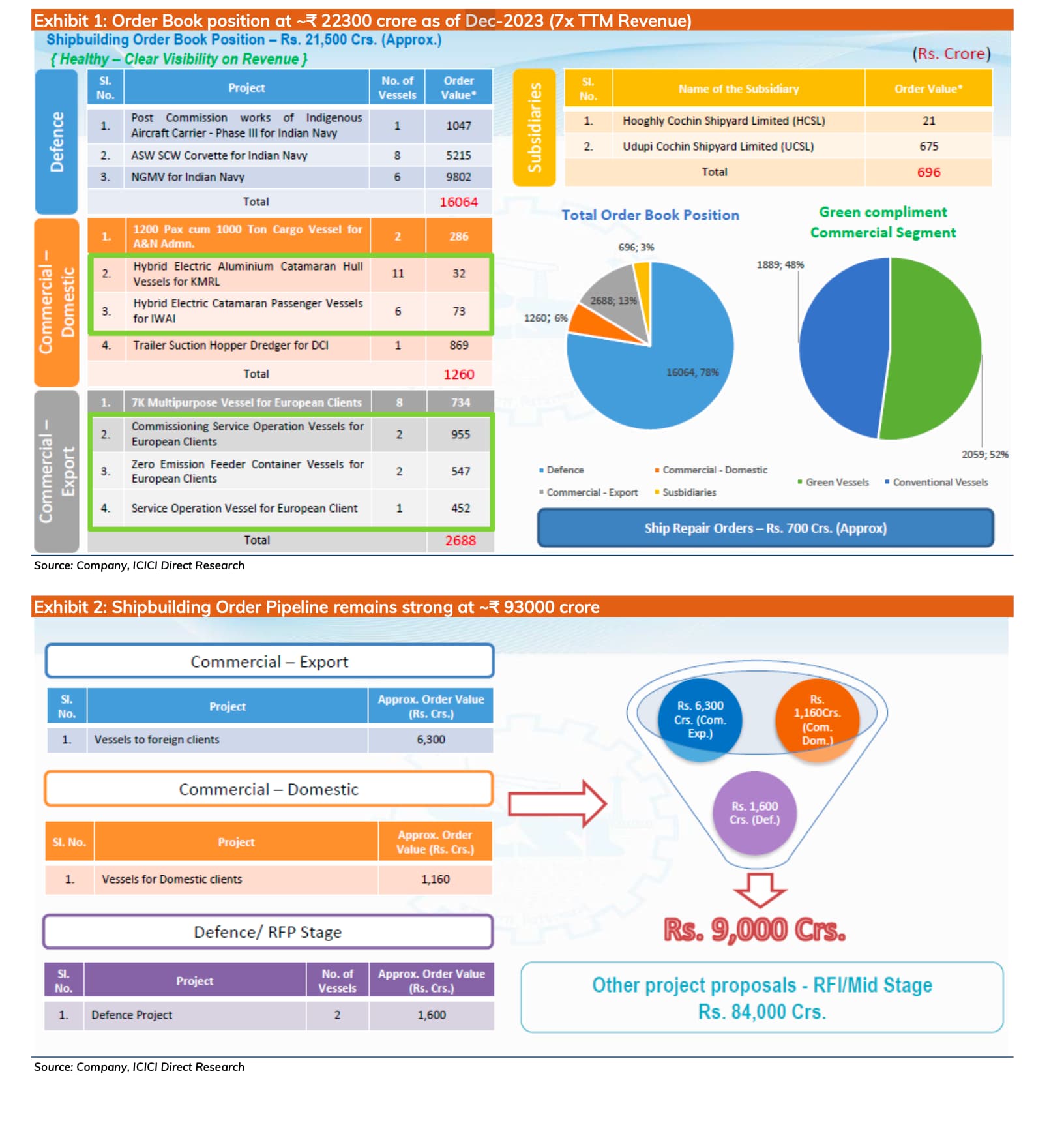

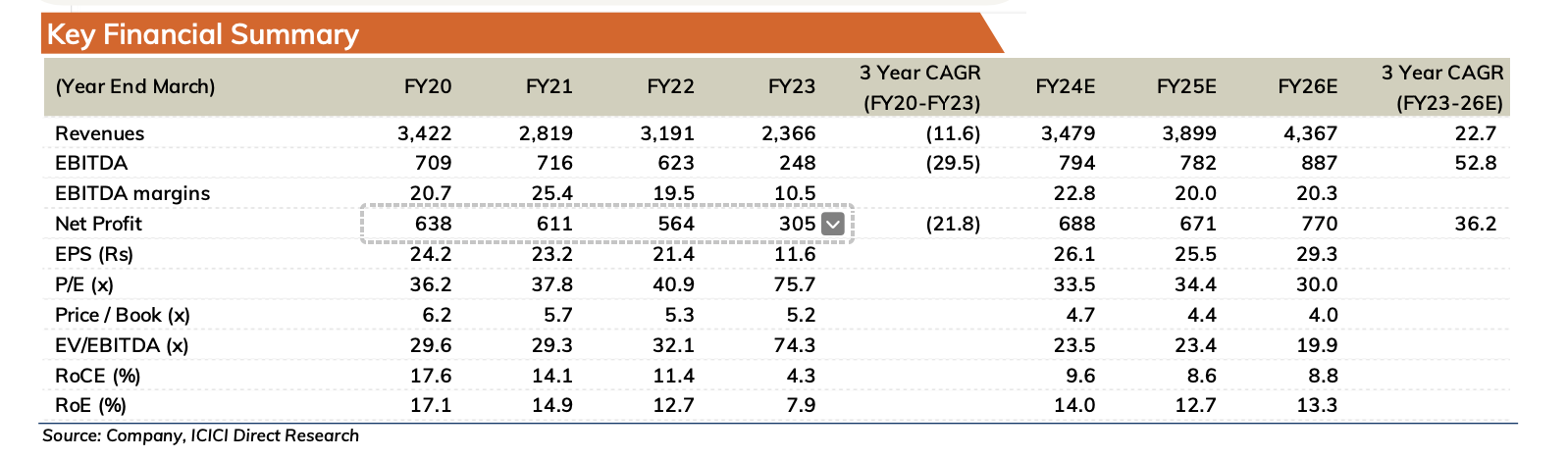

Cochin Shipyard

Anticipated Breakout and Financial Growth Trajectory

Breakout is expected in near future as stock is currently in a consolidation phase, with its price oscillating between ₹800 and ₹900 with volumes drying up. It exhibits a robust growth trajectory, reflected in the ascending trends of its revenue, operating profit margin (OPM), and net profit. The order book stands impressively at seven times the trailing twelve months (TTM) revenue, signaling strong future earnings potential. Over the next three years, the company is projected to achieve a compound annual growth rate (CAGR) of 22.7% in revenue and an even more impressive 36.2% in net profit, underscoring its promising financial outlook.

Disclaimer: Not buy or sell recommendations, only for educational purpose

Invested ~ 8.5% of total capital @ 890

Johnson Controls-Hitachi Air Conditioning (30-03-2024)

Seems Johnson Controls Hitachi is on block

Milwaukee-based Johnson Controls has been working with its advisers to sell its residential and light commercial businesses, including a U.S. business and a 60% stake in an air-conditioning venture with Japan’s Hitachi (6501.T), opens new tab called Johnson Controls–Hitachi Air Conditioning, the sources said, requesting anonymity as the discussions are confidential.

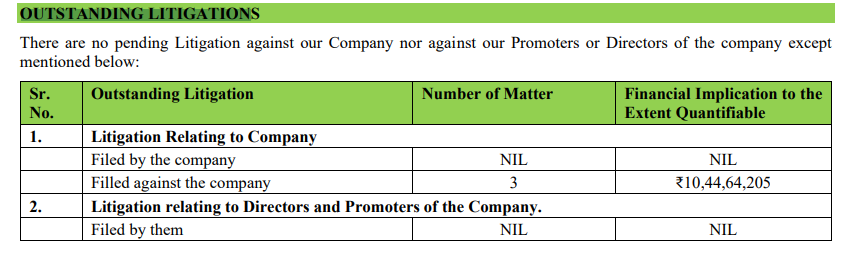

Hi-Green Carbon Ltd – Play on Renewable energy endeavoring wealth from waste (30-03-2024)

Does anyone have clarity on the Outstanding Income tax demands due with the company.

-

As per the DRHP, ‘the company has filled a response for the outstanding demand of INR 4.1 Crore for AY 2013-14 and the same is under consideration by the department’ – The response was submitted on 21.09.2022.

-

As per the DRHP, the company has made an appeal against the order passed by AO assessing total income at Rs. 6,09,50,000/-, as fictitious loan from RNG Finlease Private Limited is nothing but the devise to bring unaccounted money into books of account and claimed the same as fictitious loan. This is pending adjudication.

L&T – Bluechip, Value play, Digital giant in making (30-03-2024)

Three pronged play in middle east

- Traditional oil and gas

- Value add – plastics and chemicals

- New energy transition

At this rate L&T is more of a global play now. Roughly One third each from

- Middle east

- Digital services from west

- India

Yogesh Portfolio (30-03-2024)

JTL Industries

Growth Ahead

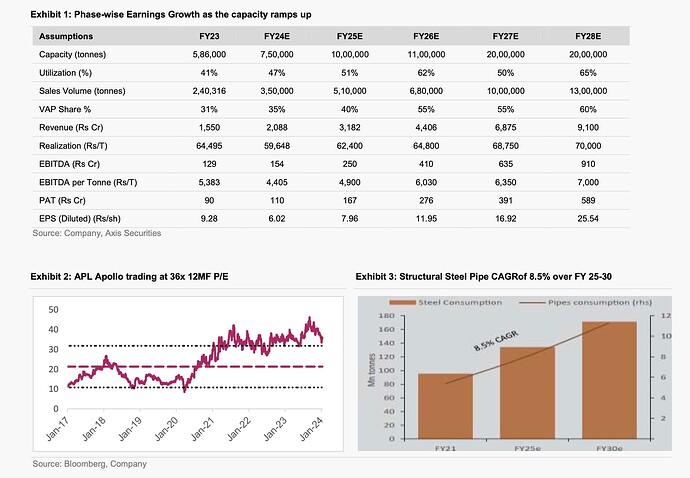

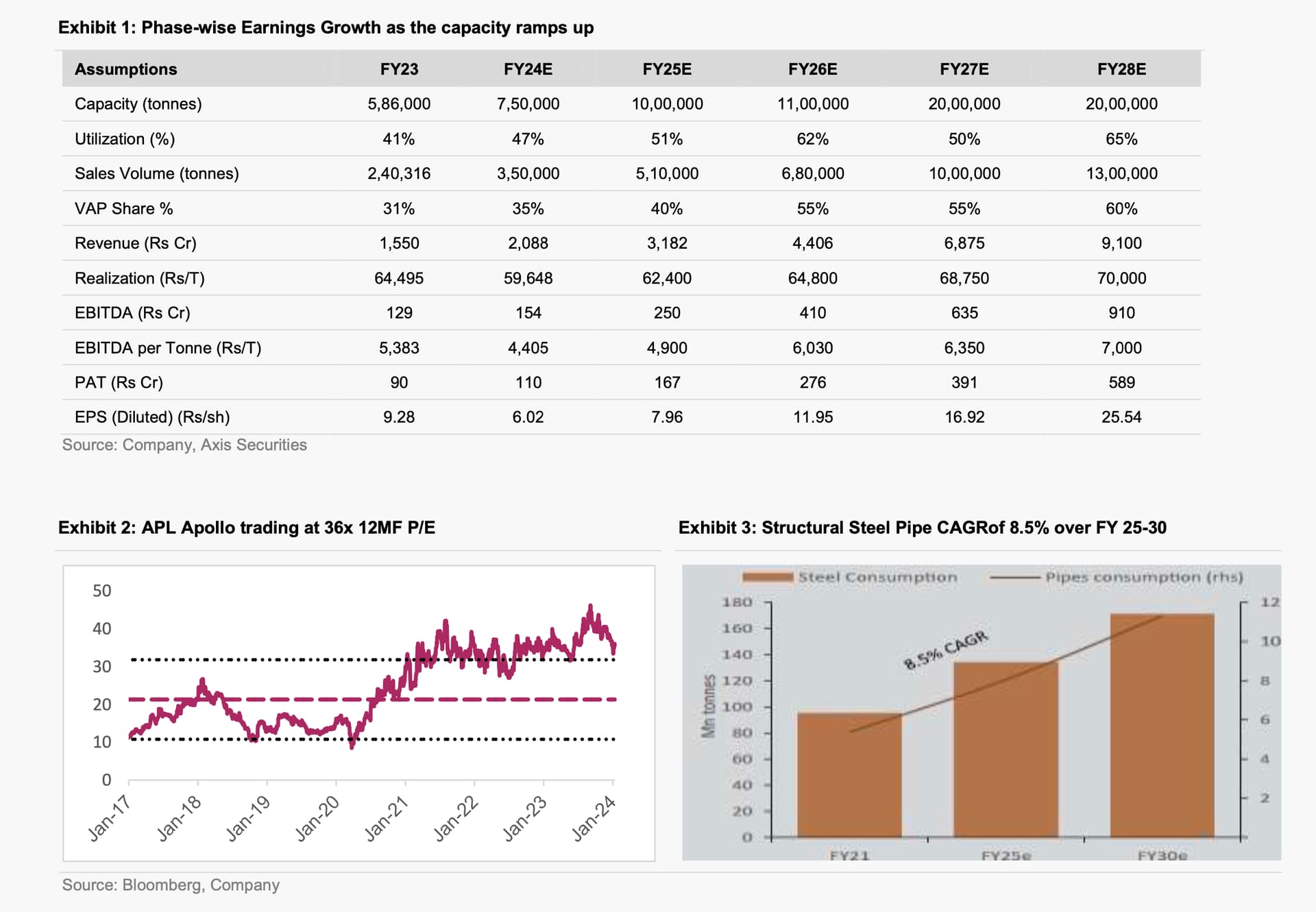

- Company’s announcement in Dec’23 to raise Rs 1,310 Cr to enhance the capacity to 2 MTPA by the end of FY27

- Capacity will reach 2MT by the end of FY27 and full utilization (max ~65% industry standard) on the 2MT capacity will be achieved in FY28

- JTL will enhance its SKUs from 1,000 to 4,000 by FY28 with a focus on VAP (Value-added products). This will translate to ~60% VAP share by FY28 as against 31% as of 9MFY24.

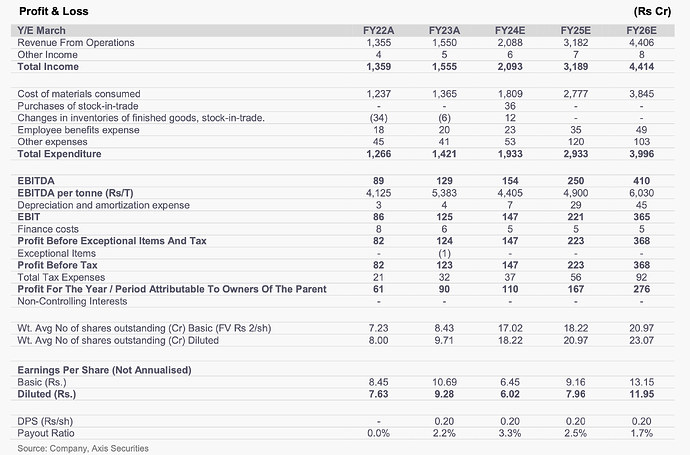

- The newer VAP products will have EBITDA/t of Rs 9,000- 11,000/t, against the general products at Rs 2,000-2,500/t, which will drive the blended EBITDA/t to ~Rs 7,500/t by FY28 (Rs 5,383/t in FY23).

- The expansion plan from 0.56 MTPA to 1 MTPA is on track and will be completed by FY25.

- For the next 1 MT incremental expansion, JTL will focus on enhancing its product profile by adding more DFT lines, introducing color-coated products, and pre-galvanised sheets

Company Outlook & Guidance

- Sector Outlook: Positive

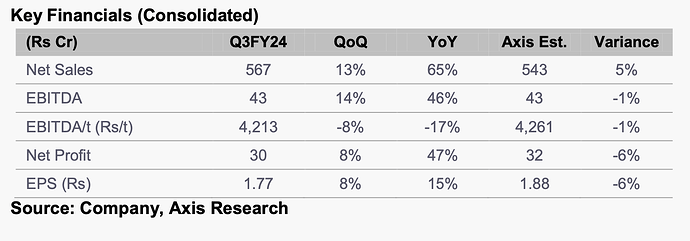

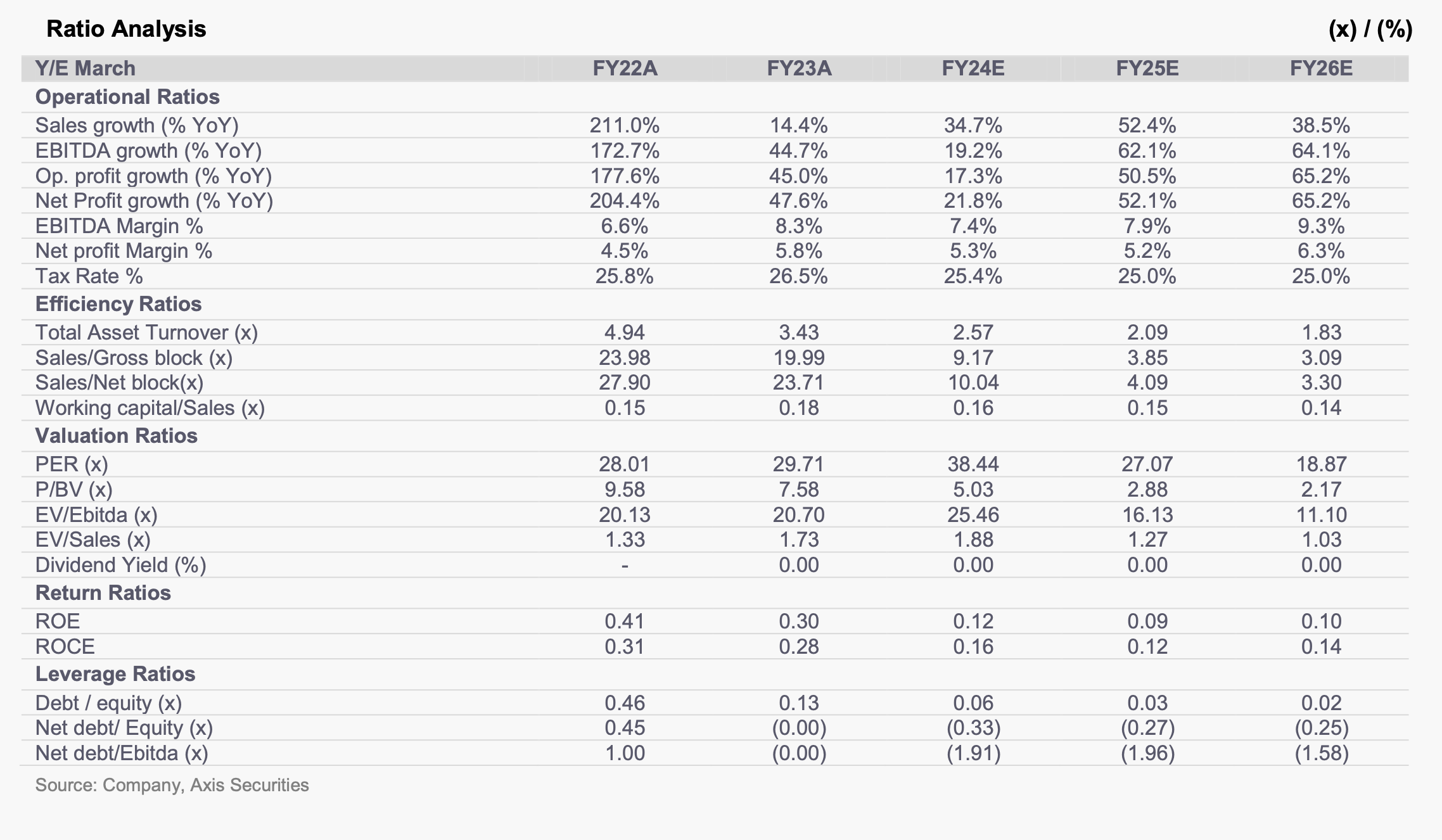

- Post strong Q3FY24 sales volumes, FY24 sales volume to reach ~3.5 Lc tonnes, up 45% YoY, ahead of earlier growth guidance of 30% YoY.

- In Q4FY23, the VAP share could bounce back to 40% (~35% for FY24) from 20% in Q3FY24, as the maintenance of the galvanizing pot is over. 0.56 MT to 1 MT expansion is on track and will be complete before FY25.

- DFT facilities of 2 Lc tonnes out of the total incremental capacity of 4 Lc tonnes will start from Q1FY25.

Concall Highlights Q3FY24

- The company plans to invest Rs 1,200 Cr in its subsidiary company JTL Tubes Limited to set up a Mega Project in the state of Maharashtra at Mangaon. The Capex will be partly incurred from the company’s internal accruals and partly from the proposed issue proceeds (preferential/ QIP).

- In Q3FY24 exports volume stood at 3.6kt, down 19% YoY and 17% QoQ, as the company focused on the domestic market led by strong domestic demand

- JTL currently has 800 dealers pan India out of a total dealer network of 1,000-1,100 dealers, thereby having 80% of dealers catered by it. As more VAP and SKUs share rise in future, more dealers will get on board with the company.

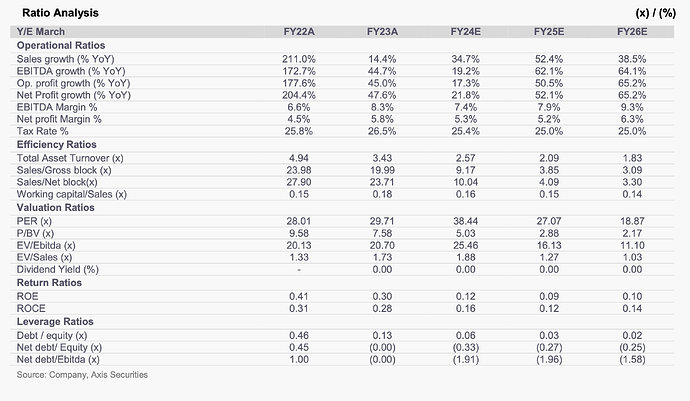

- It currently holds a ~9% market share in the industry and after the onset of the entire 2 MT capacity, its market share will double to 20% by FY28. The market share has moved from 3% in 2019 to 9% in 2023.

- ERW pipes industry is expected to grow at a faster pace than the steel industry at 12-13% in FY24 vs. 10% growth expected in the steel industry.

- Post FY24, the ERW pipes industry is expected to grow by 8-9% for the next couple of years as it replaces traditional long products that were previously used in construction.

Key Risk

- Delay in project execution for the 2 MTPA expansion at the Mangaon Maharashtra plant

- Volatility in the steel prices will drive destocking at the dealer’s end, impacting EBITDA/t.

- Lower-than-estimated demand scenario to hamper the off-take of volumes, impacting our sales volume growth forecasts

Phase Wise Growth at JTL Ahead

- APL Apollo Tubes, which is the sector leader, is currently trading at 36x consensus 12MF P/E, a premium to its long-term average of 21x given the pace of infrastructure growth in the country.

Disclaimer: Not buy or sell recommendations, only for educational purpose

Invested ~ 8% of total capital @ 190