Sir, but Intrinsic value being shown in Screener as 36.2/-

Your take please.

Posts tagged Value Pickr

KMC Speciality hospital (27-03-2024)

Nilkamal – Back on Track? (27-03-2024)

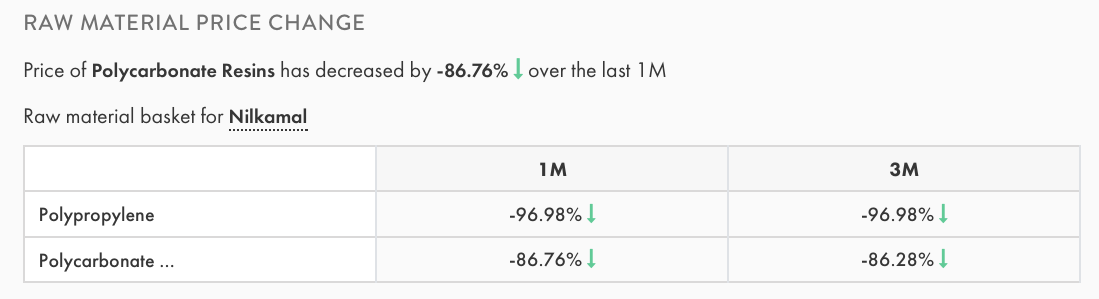

The observed reduction in raw material costs, notably an 86.76% decrease in the price of Polycarbonate Resins over the last month, signals a positive development for the company’s financials. Notably, the company has been engaging in significant capital expenditure over the past two years. Although the specifics of these investments remain undisclosed due to the absence of investor conferences, the potential for these expenditures to enhance the company’s long-term value should not be overlooked. Concurrently, there has been a notable decline in share prices recently, the cause of which is not entirely clear. It would be beneficial for stakeholders to consider both these capital investments and the reduction in material costs when evaluating the company’s future prospects.

Natco Pharma: Focusing On Complex Products (27-03-2024)

My view is that : Natco Pharma looks all set to run from here:

- EPS of 70+ is sure for FY 24 and even taking a moderate 25 PE valuation make it reach Rs 1750 in short term.

- Cash surplus of 1800 Cr.

- With its developments in Oncology segment, next 2-3 years look really good for growth.

Annapurna Swadisht Ltd – A Swadisht FMCG investment? (27-03-2024)

Positive development

Annapurna has entered into the edible oil business via acquisition of Arati brand. Hopefully this would also provide with backward integration with consumption of oil manufactured in-house, increasing margins.

Press release: https://nsearchives.nseindia.com/corporate/ANNAPURNA_27032024133842_Intimation_SE_PR_ASL.pdf

Usha Martin- Coming out of Chaos (27-03-2024)

Usha Martin .pdf (648.9 KB)

CFO and whole time director of the company – both being changed together after the existing ones have resigned.

The resignation of the CFO is dated 6/1/24 means this must be planned since a while. Maybe the exchange should have been notified sooner?

Shivalik Bimetal Controls Ltd (SBCL) (27-03-2024)

This is behind Pay wall. It is better you list out salient points if it is not infringing on the copyright issues. If there are copyright issues , then posting the link is not advisable.

MOLD TEK PACKAGING—dividend plus growth (27-03-2024)

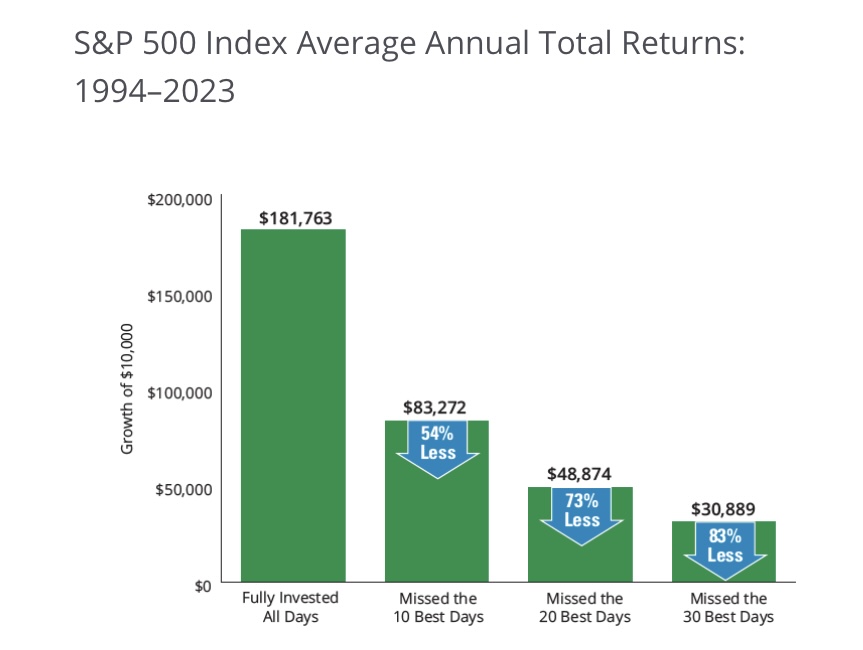

The debate we are having is time in the market vs timing the market. I personally do not have the confidence to time the market.

Missing just a few good days can have massive detrimental effects to long term returns. When stocks move they move very aggressively and we have seem the same with Mold Tek in the past, when gains have come they come super fast. Stock went from 200 to 1000 in less than 2 years time frame, during that journey there were weeks when stock price has doubled. Yes it is in consolidation now but fundamentals are quietly strengthening. Institutional investors have many advantages over retail investors. They have private meetings with promoters, they have access to industry reports worth 1000s of dollars etc. The only advantage we have is our ability to stay invested during hard times as we dont have the pressure to show gains to clients every month or quarter. We have to hold on dearly to that advantage if we wish to outperform.

Apollo Pipes Ltd. ~ From the house of APL Apollo (Erstwhile Amulya Leasing & Finance) (27-03-2024)

the Company has completed the acquisition of 53.57% share

capital and voting rights in KML on March 26, 2024, as per terms of the definitive documents executed

in this regard. As a result of capital infusion, Kisan Moldings Limited has become the subsidiary of

Apollo Pipes Limited.

MOLD TEK PACKAGING—dividend plus growth (27-03-2024)

100 baggers is perhaps the worst book to follow. It is like saying 10 people jumped from a ledge and landed successfully so it is something that has good success. It doesn’t talk about potentially 1000 people who failed the jump. You cannot make learnings about success stories without looking into counter examples where the companies who did the same thing still failed. In that the case the trait might be harmless or worse.