Thanks visuarchie for sharing the list. Could you please share how do you calculate a year and 6 months back prices? For e.g if today is 18th March 2024, which date will you pick for 12 and 6 months back and how?

Posts tagged Value Pickr

Dhruv’s Portfolio: Comments Appriciated (16-03-2024)

@sameernics Thanks for reply

I completely align to this. But I’m betting on the volume growth over next 10 years in india, with realestate cycle going up and one more thing for my view, when we paint the house we ask for the brand of paint which is being used by contractor, well this is stuff I see lot happening with Fevicol and everything, this is just my safe bet

Well I believe that eyeing and reaching is two different thing, surely grasim couls achieve this due to it’s reach in dealership and everything because of ultratech but I strongly believe this is not gonna be possible with the dominance which Asian Paints commands.

Yes Paint is Bread and butter for them but

- No. 1 Integrated Home Décor Player

- No. 1 in Decorative Lighting

- No. 2 in Fabric & Furnishing

- No. 1 in Wallcovering & Textures

Although these are segments which does not generate a lot of revenue or profit but they are actively foraying in different domain. Asian paints at P/E of 90-100 is not worth the money but at multiple of 50, there is not a lot fo risk and in this overheated markets (strictly my view), it’s better to find safe pockets.

RACL Geartech Limited (16-03-2024)

RACL continues their growth trajectory (17% sales and flat EPS) and are confident of reaching 548 cr. sales in FY25 (implying 37% absolute growth). Concall notes below.

FY24Q3

- Nominated as a Tier 1 supplier for passenger car segment for the first time. This is for entire subsystem for park lock mechanism and from a new customer for an electric sports car using a new platform coming in 2027 ($38mn business over 7-8 years starting FY27). Competitors were Chinese and European companies. This can change the trajectory of RACL’s business (from 500 to 1000 cr.). Will be manufactured in Gajraula plant (which is now running on 100% green energy)

- Inaugurated plant 2 in Noida (26k sq.ft vs 11k sq.ft of earlier Noida plant). Equipped with clean rooms and invested $1mn capex. Doubled manpower from 120 to 250. Will export new electric bicycle product, earlier plant was only catering to domestic market

- For the electric bicycle product, their customer’s competitor is selling 2mn bikes/year

- Started invoicing KTM Austria locally on a weekly just in time basis

- Capex: 80-85 cr. in FY24, 60 cr. in FY25. Have invested 25 crs. in last 2-years for housing colonies for engineers and managers.

- Still have 10 acres of land

- Sales should reach 548 cr. in FY25

- With 22 customers, RACL is present in every segment (100 cc 2-W, 49 ton truck, passenger cars, tractors, off-road vehicle for sand, snow, etc.)

- With EVs and their low-weight requirements, have seen manufacturers shifting to non-ferrous materials (aluminum, titanium, etc.). Also have seen huge increase in demand for precision machining

Disclosure: Invested (position size here, bought shares in last-30 days)

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (16-03-2024)

It is very difficult to predict the timelines of “unbanning”. However, there have been times when companies have achieved it within a year. HDFC Bank’s CC ban lasted for around 8 months [HERE]. Mastercard’s ban lasted approx a year [HERE].

In the case of IIFL, management is claiming that they have rectified the issues and going to request a special audit from RBI. If I am not mistaken, the special audits could take 6 months (if successful) but for safer side, I will assume a year.

What we should also consider is the broader implications: the customers, future growth, and possibilities of valuation de-rating under the categorization of poor CG.

Disclaimer: I may or not be invested in any of the names mentioned here. This is not a BUY/SELL recommendation. These are my views and I often go wrong or change my views without being able to inform anyone.

Aarti Industries – Integrated Diversified Player on Benzene Derivatives (16-03-2024)

PE is high due to depressed earnings. Price has increased recently due to anticipation in recovery.

Piccadily Agro Industries Ltd (16-03-2024)

Yesterday, at a liquor shop in posh South Delhi locality, I saw miniature bottles of Indri (50 or 60ml ones). Although miniature bottle versions are quite common outside India, it is quite a novel concept here for premium whisky.

In response to my query, the store sales guy said that it is the best selling premium whisky in their shop with sales trajectory increasing with time.

Further, Dubai Duty free has now started selling Indri and it is being launched in Nepal as well.

Rudra’s PF and Information attic (16-03-2024)

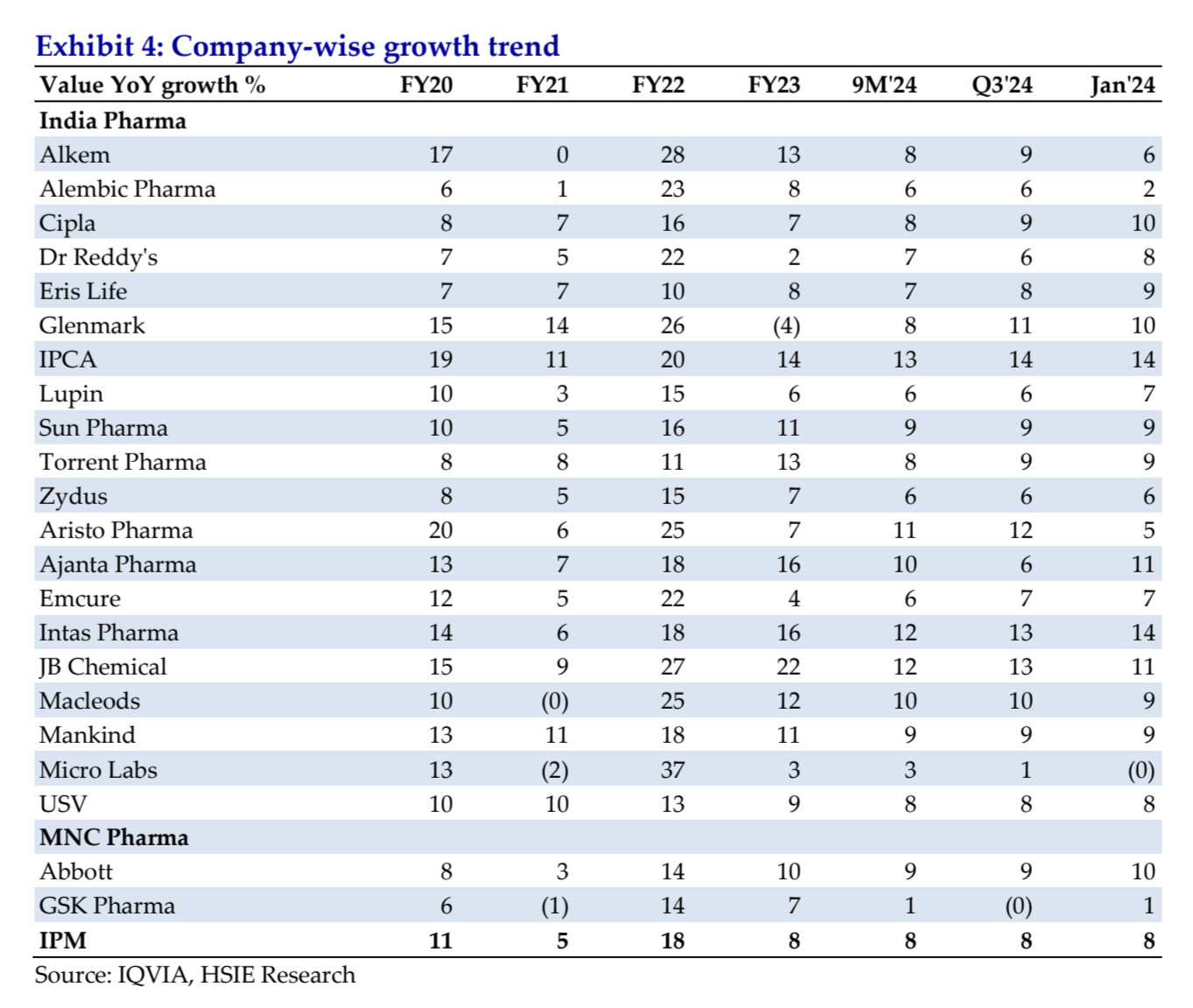

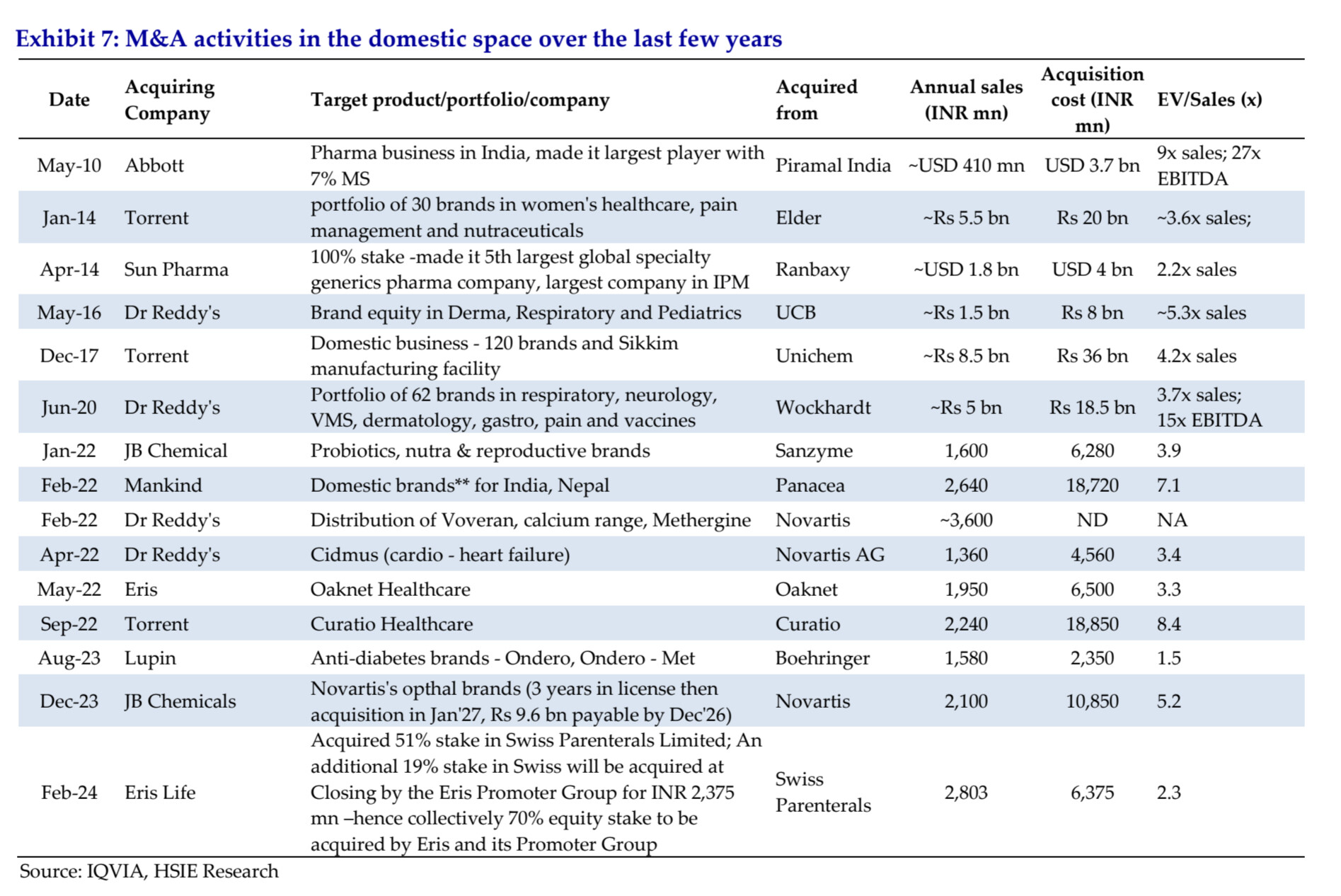

The Domestic Formulation players are very well poised for double growth. Pharmaceuticals could be a go to sector with stable returns despite of the regulatory overheads of price control.

Many companies have successfully tapped the inorganic route over the years

Is Buy and Forget a Myth? (16-03-2024)

When I see a car zigzagging at 100 Km per hour, I make a prayer for the driver, his family and the passengers.

I would rather drive safe.

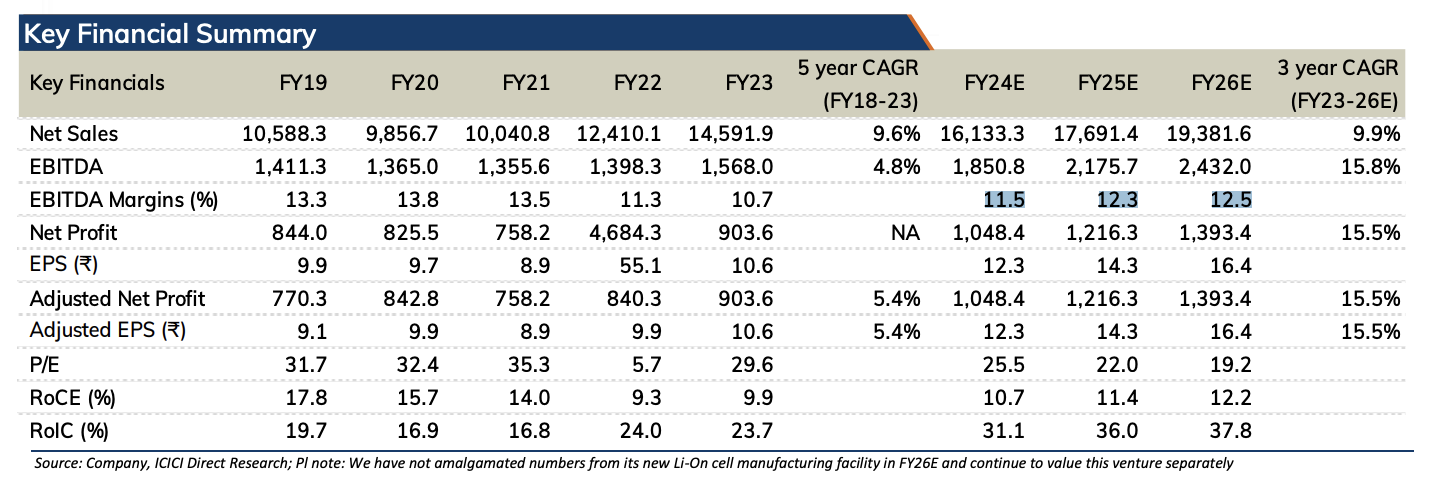

Exide Industries (16-03-2024)

Excerpt from ICICI Direct Research Report

…we expect margins to inch up to 12.5% mark by FY26E

Report Link: https://www.dsij.in/productattachment/BrokerRecommendation/Exide%20Industries.pdf

Report Date: 30 Jan 2024

Disclaimer: Invested. Not a buy/sell recommendation

Investing Basics – Feel free to ask the most basic questions (16-03-2024)

@Worldlywiseinvestors Sir I saw company in which PE was very high i.e 120 but after earning came PE decreased to 30-40.

So my point is that how to evaluate such a company whose PE is so high?

Note: Company made almost 4x return from 120 PE and It was hospital industry.