This was a great listen, so many different mental models in 1 place. Thanks for sharing.

Posts tagged Value Pickr

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

Even i’m not able to find the link to the conference call. Anybody?

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

IIFL scheduled a meeting on today 8.30am(5th Mar) to discuss about gold issue, but I am not able to find any meeting link or number. Can anyone help me with this

Manappuram Finance (05-03-2024)

can manapuram become number 2 again?

Highly probable

How will this affect the industry?

Players might become alert good for people who follow the rules

Is the industry so diluted that no single player will make gains from this ?

Most likely

Is our company following compliance?

Hope so

Give me your opinion

TARSONS products ltd (05-03-2024)

Few comments on what I understand from the Concall and Credit rating reports:-

- The growth potential for the plastic usage in the lifescience market exists. However, the company presentation provides market intelligence only till FY2025. I would have preferred an overview till FY2027/28

- Nerbe is the 1st ever acquisition for Tarsons. Even though the pricing and valuation look reasonable, the management has no experience in M&A. Some of the companies like Affle who have grown via M&A also take 12 to 18months for developing synergies. The management guidance to derive benefits from Nerbe in 8 to 10 quarters sounds too pessimistic. Probably inexperience of M&A ?

- The operating margins have dropped due to higher sales of consumables. Tarsons is entering into new products and management already plans push sales with some promotional offers. Even though the guidance is to retain EBITDA margins, I am not convinced the untested waters will allow it. Specially, since economies of scale will not be available for a couple of years

- As per the concall, the utilization for the new plants are expected to take 4 to 5years. This is slightly slower than the industry target of 3 to 4years. However, it means the PAT may stay subdued for the next couple of years. The 1st commercial production expected in Q3FY25.

- Another red flag is the sudden increase in working capital. It seems the sales are not getting converted to cash. A sign of push sales.

- Another risk I see is the concentration of Manufacturing units in WB. There is a economic advantage to have most production units close by but some diversification would also help reducing risk.

- The credit agencies have switched the rating to “Under watch” due to certain non-disclosures of Nerbe acquisition. The Mgmt, plans to bring out all details by the next quarter. Waiting for the next credit report.

- Red sea crisis will have an impact on the sales as the smaller customers have either put their orders on hold or postponed the same. Already the share of export revenue is considerably down in FY24. I expect the trend to continue, thereby impacting the margins further in coming quarters.

Overall, even though the mgmt has done well over the last 4decades, at this point I see too many uncertainties in the business. I would personally choose the option to wait and watch from the sidelines and see the story unfold. Prefer to enter with some light at the end of the tunnel.

Disc: Please do your due diligence. This is not a buy or sell recommendation. This is my personal assessment of the situation.

HDFC Bank- we understand your world (05-03-2024)

Good read to understand the bank –HDFC Bank’s Merger Pangs

52 week highs and all time highs strategy (05-03-2024)

JM financial confirmed breakout from double bottom formation above 84. The bottoms were at 57 and intervening peak was at 84. (marked in solid blue lines) Target for this pattern was 111. (marked in dotted red lines) From close to target range stock price has corrected. I have marked the 30 WEMA in dotted blue lines and its current value is at 94.

Regarding formation of cup and handle, its too early to conclude. In situations like current one ideal thing is to watch for a good weekly candle close and have a re look at the daily chart then. Any signs of reversal from this short term downtrend ( if it is a short term downtrend) should be watched out for.

Overall your observations are spot on. But the possibility of the stock behaving differently from what we expect should also be kept in mind. Overall the stock has been a laggard as compared to other big winners. ( things can change for it too, but as of now it only remains in my watchlist. )

52 week highs and all time highs strategy (05-03-2024)

Whenever a stock approaches a major resistance (52 week high or multi year high or all time highs)

In some cases it can breach through the resistance straightaway, and keeps going up. But usually after going some distance, it tends to take a pause, consolidate, or retrace back to breakout levels and undergo a retest. Or

In most cases it tends to consolidate within a tight range above or around the resistance level. And after enough consolidation has happened, it breaks out to higher ground. Or

The breakout fails and the stock price falls back from there and goes down a lot.

All these possibilities have to be borne in mind. That is where the fundamental analysis comes into picture. And the overall market sentiments also matter.

In case of Time techno, it crossed its previous ATH by a small margin and has been consolidating marginally below the previous ATH in a sort of triangular consolidation. This can happen in a lot of similar situations near previous major resistances. You can keep on observing charts where stocks have approached major resistances and see how they have behaved.

Attached daily chart of Time techno shows a consolidation in form of flag/triangle just below previous ATH. Also note a previous consolidation marked in the chart in form of a flag.

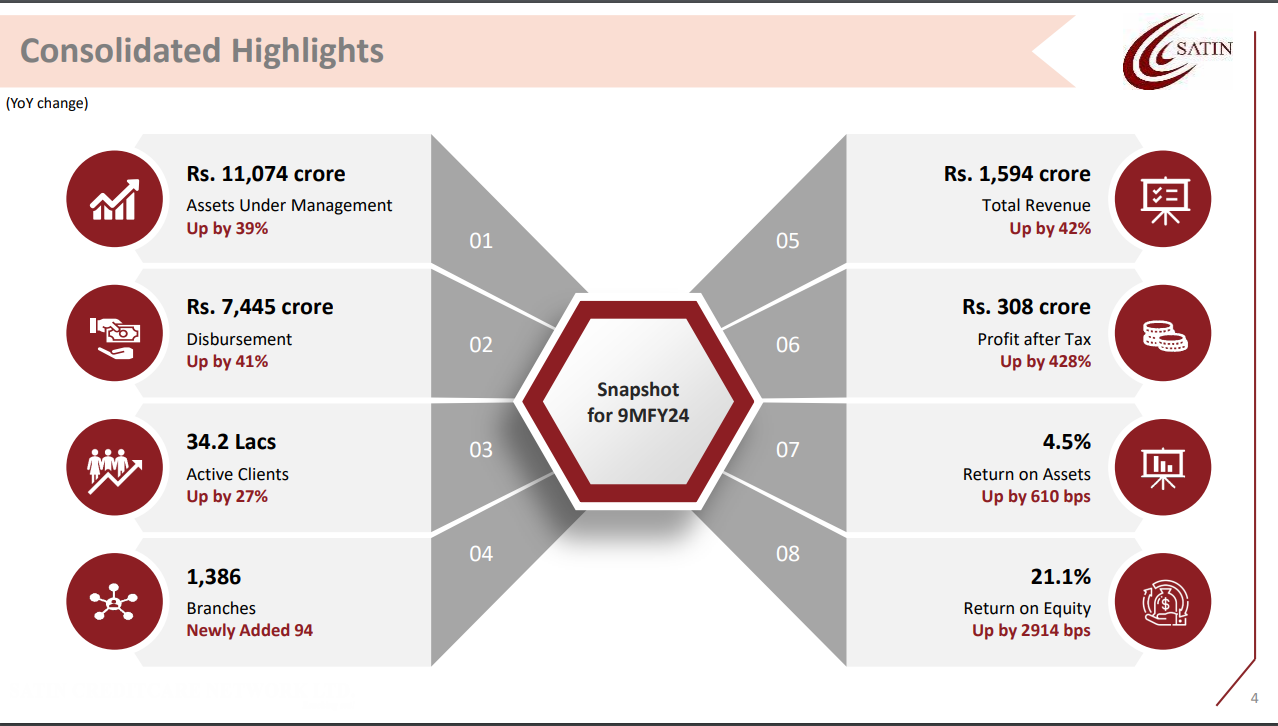

Satin Creditcare Network Ltd – Reaching out! (04-03-2024)

Satin came out with banger Q3 numbers, with RoA and RoE at 4.5% and 21%, a few more quarters of sustained profitability should help re-rate the stock to a minimum of 1.5-2x book (current BV is 205/sh)

Impressed with the management as they cleaned up the book and now are at historic profitability metrics, they not only delivered the projections before FY24 ended.

Invested and biased