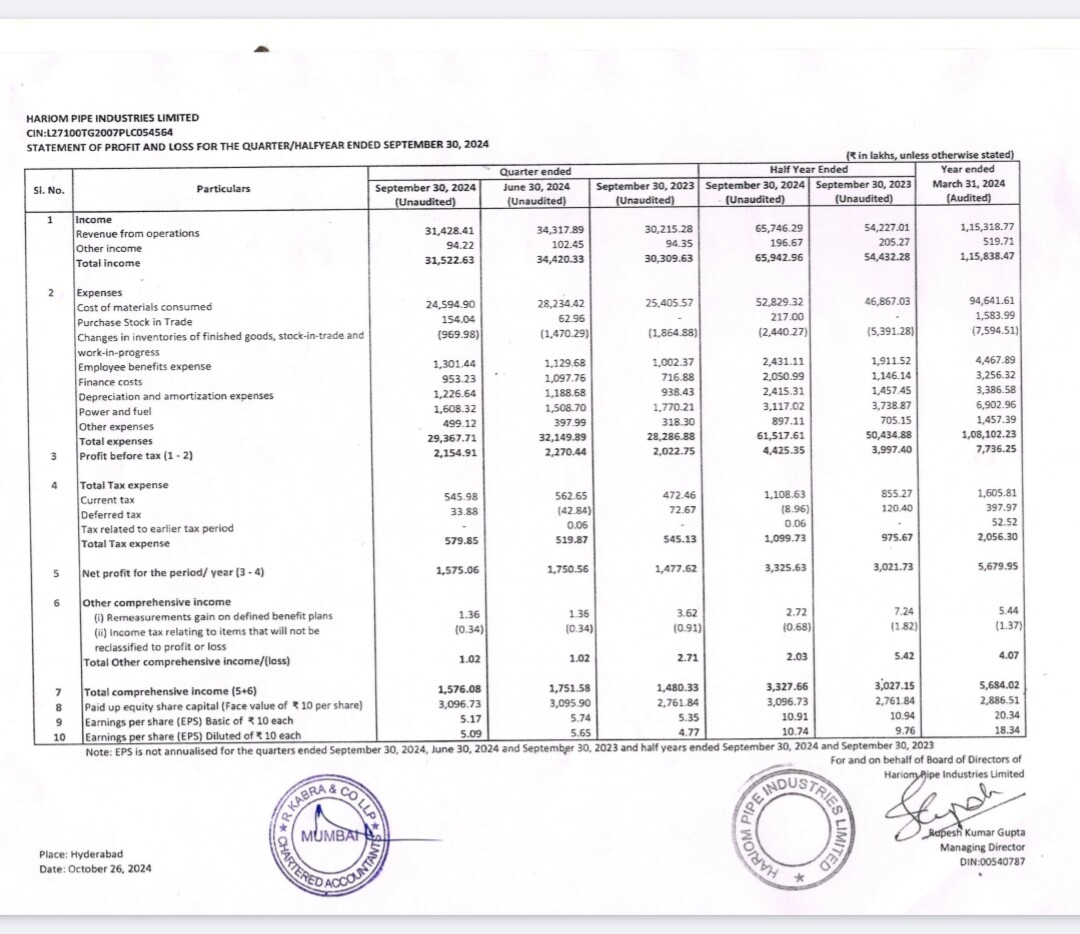

Hariom Pipe Results

Stable Set not as per Growth, but as per operation perspective

Rev Growth of 4% YoY n -9% QoQ

EBITDA Growth of 16% YoG n -7% QoQ

Margins up at 13.4% vs 11.7% YoY n 13.1% QoQ

PAT Growth of 7% YoY

OCF Strong at 53 cr vs -60.8 cr

Debt & WC Req🔻

CFO already pointed out about weak results & I feel market had already discounted it as fall more ATH is more than 30%

Good part is Strong OCF, which led to lower Debt & WC Req

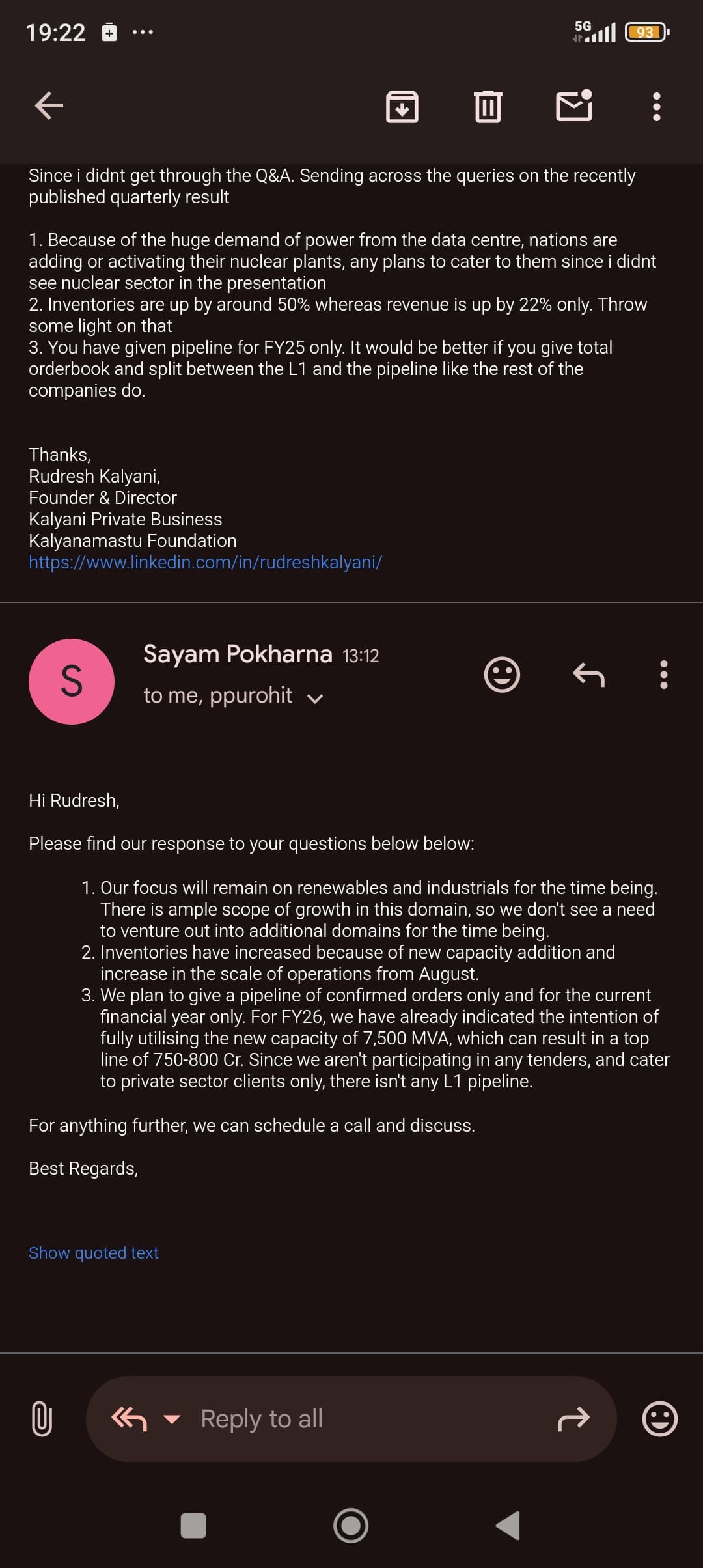

With this Q about Fund Raise is a big suspense!!

Concall might give some boost or will clear many doubts

No Reco

Disc: Invested & will continue to hold