But visa service and golf events have nothing in common. Could you please explain how is this move beneficial? To me it seems like something out of their domain at the moment.

Posts tagged Value Pickr

Shakti Pumps – solar shakti (power)! (25-10-2024)

From where this 215 number came?

IDFC First Bank Limited (25-10-2024)

I got the email regarding the transfer but not showing in Zerodha.

Probably will be visible on 28th

Poonawalla Fincorp formerly Magma Fincorp (25-10-2024)

I believe some skeletons of the previous management are coming out now as the current management has excess emphasis on risk management. They are also speaking of now opening branches which goes against their core of being a digital lender.

All in all, its now clear why the entire management was changed and a new one which is well experienced and is well reputed has been brought. They are looking to put the house in order. Clearly as they stated 4-6 quarter is the time they need to put a solid foundation for the future and change its DNA.

My personal belief is that its a painful 4-6 quarters for this stock however the good thing is that management has not scaled down its future guidance. I am a long term investor in this stock and yes its a tough decision to still hold it but i still will be holding this stock for long term.

Plz give your views on results as well

Indus Towers Limited (25-10-2024)

Any views on the latest results?

Even after good results , share price has been falling heavily.

InterGlobe Aviation – Indigo (25-10-2024)

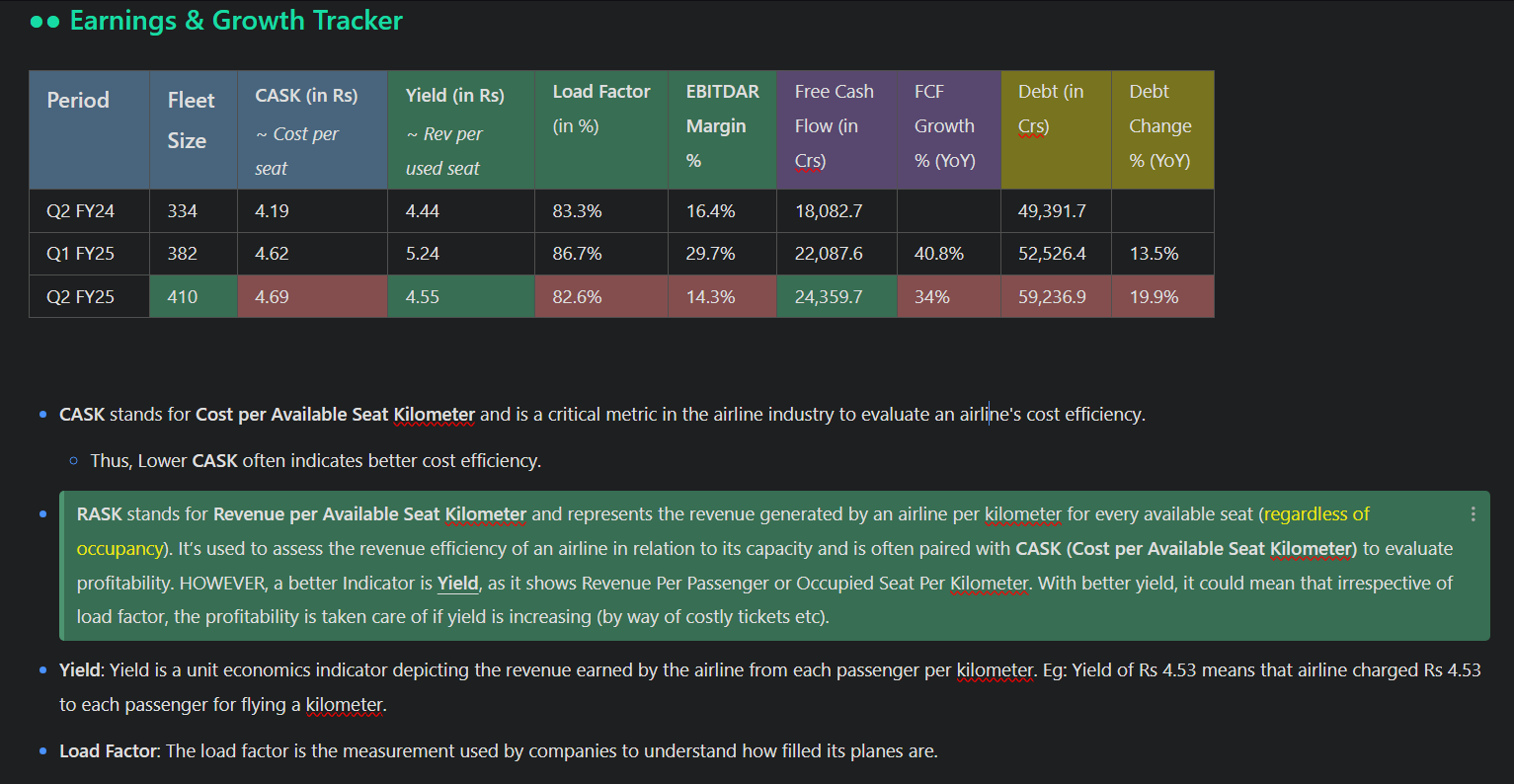

Out of the 59k Cr Debt, 57k Cr is lease liabilities, which represents their expanded fleet (as they operate on a leaseback model). The company does not have any long term debt on their balance sheet and have in fact reduced their short term borrowings by 4.8% this quarter.

Cupid Ltd – Helping the world play safe! (25-10-2024)

Have tried to cover the broader industry so this can give an idea about the stigma attached to the products.

Ranvir’s Portfolio (25-10-2024)

IMO – there are arguments for and against diversification which are well known

I personally feel that 15-20 stocks should constitute 80 pc of the portfolio. And that is what I try to do as well

For the rest 20 pc – I generally buy another 20 stocks ( say 1 pc each ) – as it helps me keep reading + learning about newer companies, sectors. Here – I am quick to add / sell, do a little bit of opportunistic trading as well

That’s what I do – broadly ![]()

![]()

I think, there is no one way to skin a cat. My way is certainly not perfect – obviously

InterGlobe Aviation – Indigo (25-10-2024)

Results are saddening. I put up a table to analyse if there are some green sides I might be missing. Here it is:

Analysis:

- Its Yield has decreased, revenue per passenger…

- Its Load factor has decreased, the occupancy of flight. More Vacant seats.

- Debt has increased and the pace of debt increment has also increased.

- Cost and Expenses have increased.

Not much of an exciting results. Only good things I could find were:

- Free cash flow has improved, working capital seems to be not constrained.

- Fleet size has expanded, potential of more revenue stream.

Some inferences I could make are:

- The pricing power of Indigo seems to be losing. A quick search of flights between metro cities will show you that Air India’s low cost variant – Air India Express has better pricing than Indigo in many cases, and where it doesnt have, it is just shy of one-two hundred.

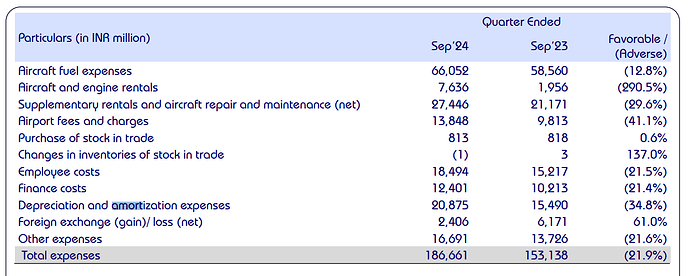

- The Depreciation-Amortization cost had increased this time, may be a one-time high increment as new aircrafts join the fleet. (2k from 1.5K Cr)

- Aircraft related costs were also high as seen below

Overall, a setback results. Perhaps, next quarter may bring back the profitability given the festival seasons and launch of business class adding to top line.

However, yield, load factor, and debt would be very crucial factors to follow.

Discl: Remain invested. Above words not to be construed as any advice.

Shakti Pumps – solar shakti (power)! (25-10-2024)

Results of Shakti Pump is fabulous YoY , as the base was extremely low. If one considers the results QoQ there is increase i revenue as well as net profit. The half yearly EPS is Rs 96.8 where as the entire year EPS for the FY 2023-24 was Rs 77. Company likely to touch yearly EPS of Rs 215 in the current FY. Lets see what the management says during the concall on Monday

shakti Pump.pdf (3.1 MB)