I dont really understand this well, even at AGM management didnt explain this very well. But I guess their volumes might be higher in recent times, and with correction in commodity costs, overall revenues look muted. But this is just a guess.

Posts tagged Value Pickr

Zen technologies – A micro cap in the defense space! (24-02-2024)

Sales not important it is important to see weather they have IP in ADS or not

Tips Industries Limited – Ready to RACE ahead! (24-02-2024)

I feel the growth would be high, whether it would be 30% or 5-10% here or there I don’t know.

The biggest low hanging fruit currently is proper monetization of shorts, Tips has already pulled its content from Instagram and I think the new deal would happen at a substantial amount whenever that happens.

And in the longer run, people will have to pay for convenience of streaming music like they are paying for now for say food delivery etc and that would trickle down to music labels.

I have shared some thoughts on monetization of convenience here if you are interested-

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (24-02-2024)

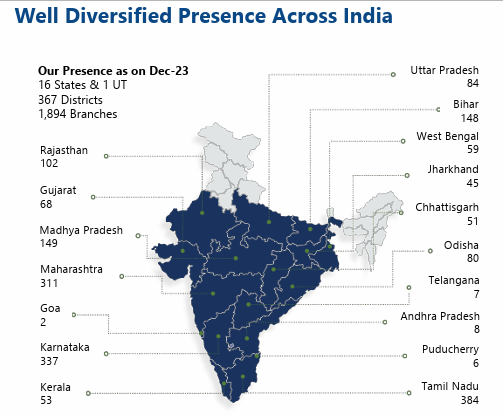

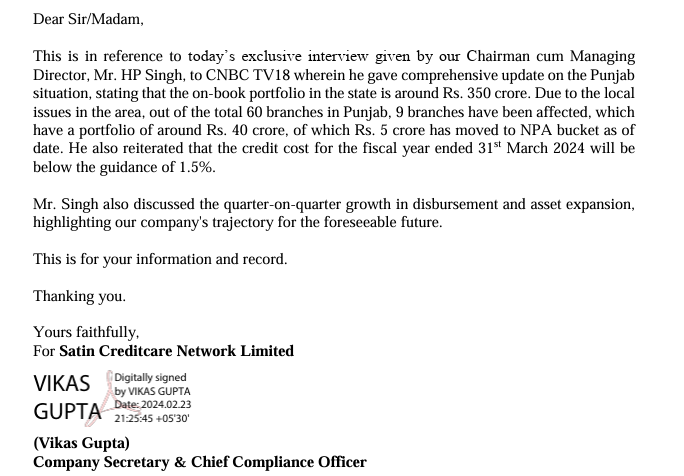

Satin is struggling in Punjab.

Any other state where there is trouble as such from Microfinance point of view.

And if Credit Access has exposure to that state ?

If not then Market Leader shall command better valuations

Diamines and Chemicals Ltd – Navigating for a long-term growth (24-02-2024)

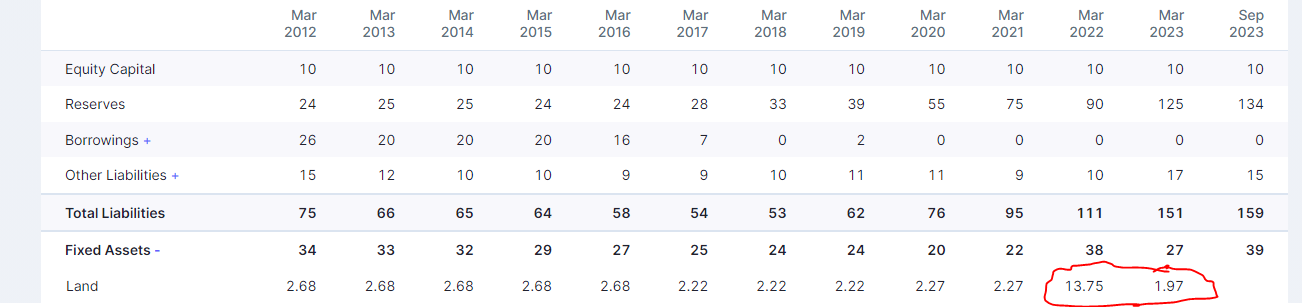

What happened here where did the land go ?

MTAR Technologies – A wager on innovation meeting economies of scale (24-02-2024)

Really thought provoking questions + write up by @ankit_george above. Going through the earnings call for Q3, I’d like to take a shot at answering all the Qs asked above:

- FY24 revenue guidance is INR 610 crore, significantly lower than the earlier estimates. Definitely shakes confidence in the estimation capabilities of the management.

- Couldn’t deduce whether it was a revenue recognition issue, but the management highlighted stabilization issues at Bloom Energy which disrupted delivery schedule. They believe the worst is over and things should become smooth from Q4.

- 500+ hot boxes delivered to Santa Cruz in Q3. 664 hot boxes estimated to be shipped in Q4.

- Expecting orders of 300 units from Fluence Energy in FY25, which could increase to 1K units in FY26 and 3K units in FY27.

- 44 electrolyzers shipped in Q3. 60 electrolyzers expected to be shipped in Q4. No comment by management on transition to high volume mass manufacturing. No comment on volumes over the next few years – however, management sees electrolyzers as a BIG OPPORTUNITY.

- No exact commentary on this, but given a lower revenue guidance I don’t think they’ll achieve the INR 150 crore domestic sales #

- Expecting order book to close at INR 1,400 crore for FY24.

I covered the Q3 earnings call HIGHLIGHTS + LOWLIGHTS in this article if anyone wants a deeper dive.

Again, amazing thought activity @ankit_george !

Disclosure: Not invested. Tracking QoQ performance.

Praveg Ltd: Play on Indian Tourism Industry! (24-02-2024)

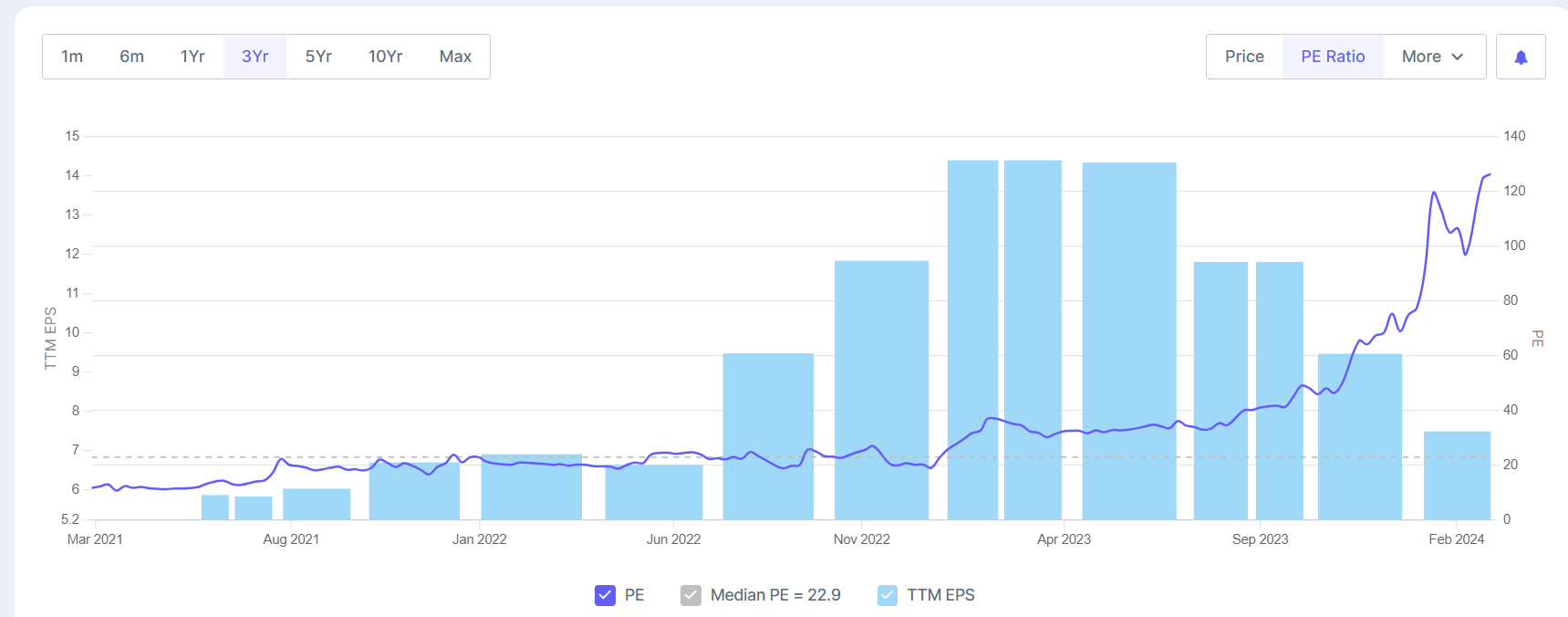

Refer all company announcement on allotment of equity shares after Dec 2023 (Q3) and try to estimate EPS on dilution basis for Q4 and FY2024.

Expecting correction in share prices as it should align with mean PE ratio

Patanjali Foods ~ Erstwhile Ruchi Soya (24-02-2024)

Sub-optimal results for the quarter; However company on the right track

Two things should be looked in Patanjali’s result for a long term investor →

- Sales growth in Foods business (% mix of food)

- Area of tree plantation

Rest of the numbers are significantly variable –

- Patanjali’ edible oil business is a commodity business with severe price fluctuations; The revenue growth is unpredictable.

- Foods business is significantly impacted by inflation, as Patanjali is selling “me too” FMCG products primarily, where it is difficult to pass on cost to customer.

If you look at result from the lens mentioned above, it was a good result –

- Foods contribute to 30% revenue now Vs 20% in FY23 and 10% in FY21

- Palm oil plantation will reach >70k hectares by end of this year, it was 60 k in FY22 → This is a long term bet. After> 10-15 years, I believe this will help detach company’s profits from global fluctuations in prices

Tips Industries Limited – Ready to RACE ahead! (24-02-2024)

@ankush12495 Thanks for the update.

What is your view on the sustenance of growth (30% topline and bottom line) beyond 3 years?

What I feel, following are the growth levers

- New listeners: Music library getting older day by day is my concern. However, paid listeners should keep on increasing for downstream platforms as a secular trend for longer.

- New monetization channels: Short video content, Instagram – probably these are the only few monetization ways with some juice left.

Would like to hear other’s thoughts?

Buy Unlisted Shares (24-02-2024)

3 questions from my side-

Has this person met promoters? or someone who knows promoters closely?

Has this person went to polymatech factory to visit?

Has this person questioned lead bankers and auditors for any irregularities?