Posts tagged Value Pickr

Natco Pharma: Focusing On Complex Products (22-02-2024)

Conference Call summary as below from screener.

In call one of the participant asked management why market is massively undervaluing company. ![]()

Financial Performance:

- Revenue milestone achieved: INR3,000 crores of revenue and INR1,000 crores of PAT year-to-date

- Q3 FY ’24 results: Consolidated total revenue of INR795.6 crores, 55% growth; Net profit of INR212.7 crores, 3.5x growth

- Guidance for FY ’24: Expecting to surpass INR1,200 crores PAT and sales close to INR4,000 crores

Business Segments:

- Segmental split for Q3: API – INR46.3 crores, Formulation domestics – INR99.4 crores, Formulation exports – INR605.6 crores, Crop health – INR14.1 crores

- AgChem business performance impacted by weather patterns, expecting growth in international markets

- U.S. market performance: Copaxone, Everolimus, Lanthanum, Lapatinib performing well, focus on complex generics

- Domestic formulation business: Oncology driving growth, looking to expand portfolio

Strategic Initiatives:

- Update on Kothur facility FDA classification awaited, risk mitigation strategy implemented

- M&A strategy: Looking for a large acquisition in Emerging Markets, strong financial position with net cash at INR1,800 crores

- RoW subsidiaries: Brazil and Canada performing well, expanding to Colombia and Indonesia, looking for acquisitions to grow business

- Investment in Cellogen for CAR-T therapy program

- Strategic investments in new technologies like gene therapy and CAR T-cell therapy

Product Development:

- NCE development: NRC-2694 Phase II trials in the U.S. and India for niche indication, strategy around NCE for future growth

- Phase II progress on new products

- Future product pipeline and potential for new revenue drivers

Capex and Expansion:

- Capex spending for the current year and future projections

- Impact of capex on fixed asset turnover

- Future outlook on capex and capacity optimization

- Expansion into agrochemical business and future growth prospects

Market Opportunities and Risks:

- Export opportunities in the agrochemical sector

- Differentiation in agrochemical portfolio compared to competitors

- Major risks including currency, inspection, and pricing risks

Other:

- Consideration of corporate actions like buybacks

- Return on capital expectations for acquisitions

- Future guidance on Revlimid sales and performance

- Closing comments and appreciation for investor interaction

D: Invested

Rahul Singh Portfolio (22-02-2024)

Result update:-

Sumuka Agro– Sumuka has posted its profit of 80lakhs which is lowest in 4 qtr. Margin has been continuesly following from 13% gross to 6% now. Sumuka is seeing pressure in its bottom line. Although revenue posted by company is record high. Generally this pressure is seen when company wants to enter in market and wanna gain some market share.

Distribution – products are still not found on online on AMAZON and Dmart, only 2 sku were visible on flipcart

Jupiter life line hospital:- company has posted its highest profit this qtr, partly due to its repayment of debt. Company is walking the talk they said IPO funds will be used to repay its debt and they have done this. Company operate independently on

owned land.The proportion of the Indian population of 60 years or more is expected to rise to 12.5% by 2026 from nearly 8% in 2011

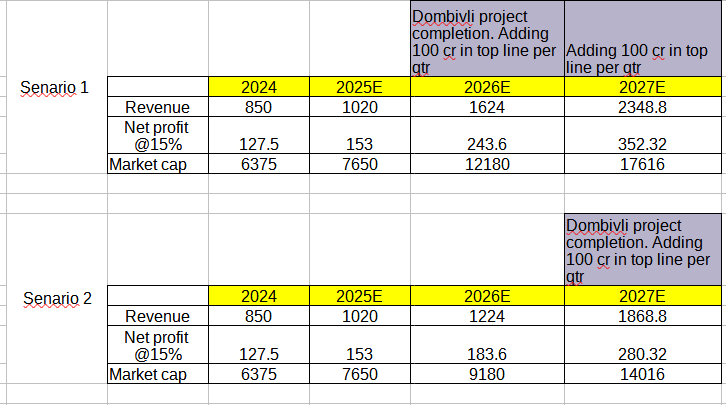

Capex update:- Company is doing a capex in Dombivali east for 500 beds. Kalyan dombivali region comes under smart city plan of central goverment. Project is very near to Lodha palava city and proposed metro line. Many residensial real estate plans are about to be completed.

Above image shows 2 senario

Senario 1 – project completed in FY 2026. Considering 20% growth annualy on existing hospitals and adding 100cr qtrly revenue in top line. (100cr calculation as below

500 beds – 50% occupency – 50000ARR) . With net profit % at 15% 2026 profit would be 243 cr and 2027 350 cr while taking 50 multiples i have come to target market cap.

Senario 2 -project compeltion in FY 2027.Considering 20% growth annualy on existing hospitals and adding 100cr qtrly revenue in top line in FY 2027. with Annual profit of 280 cr and multiple of 50 market cap would be 14000cr

Risk and threats

- Delay in dombivali project compelation

- Growth of less than 20% in top line

- Reduction in Net profit %

With above optimist senario CAGR return which can be make seems low and compnay is fairly valued at this price.

Forensics and the art of triangulation (22-02-2024)

Agree with your analysis, great effort! ![]()

Though company may do well (or may not?), there are far too many red flags for comfort. Especially with thin margin of safety, currently much closer to dumping zone than the pumping zone.

Himachal Futuristic communication (22-02-2024)

In what way operator stocks are different from pump and dump stocks? Can you elaborate more on operator stocks?

Tara Chand Infralogistic Solutions Ltd (22-02-2024)

how long does it take one to migrate, when is it expected to complete ?

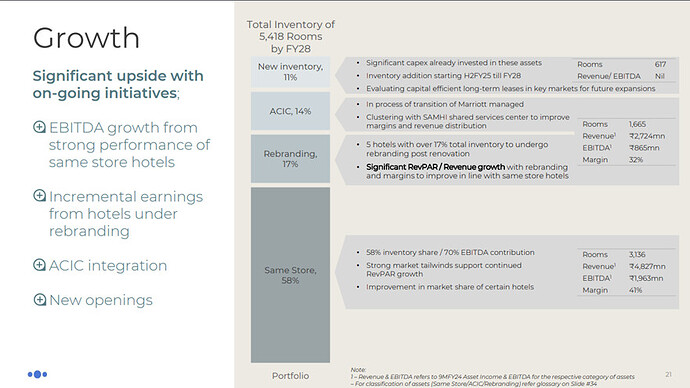

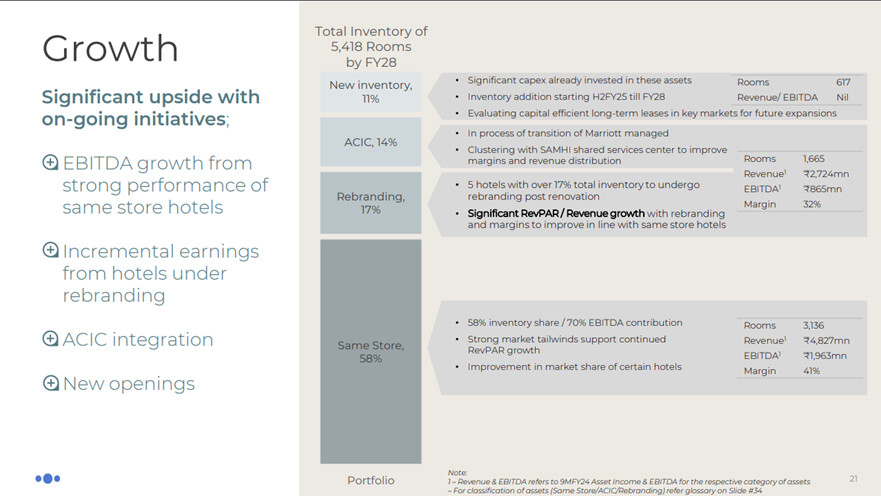

Samhi Hotels – Turnaround with Tailwinds (22-02-2024)

-

4800+ Rooms across 31 Hotels

-

Owns the properties – Refurbishes, renovates and then lets out the hotel to big hotel brands to manage it

-

Samhi doesn’t manage or operate the hotels itself

-

Passes on the management fees and retains the F&B and rental incomes

-

75% is room rental; 25% from F&B

-

Hotels / Brands:

- Courtyard by Marriott

- Fairfield by Marriott

- Sheraton by Marriott

- Renaissance by Marriott

- IHG

- Hyatt Place

- Hyatt Regency

- Holiday Inn

-

Owned by Samhi and managed by Marriott / IHG / Hyatt (charges mgmt. fees to Samhi)

-

90% of their revenues come from Tier-1 cities

-

Hotel traffic tends to be higher in these cities

-

ARRs are higher in these cities

-

Good geographical diversification protecting it from unforeseen situations in a certain city / region

-

Focuses a lot on office space absorption, which is on the rise (lot of scope in cities like Bangalore, Mumbai, etc.)

-

Commercial activity has picked up and expected to stay robust going forward

-

Air passenger traffic remains strong, showing good travel demand

-

Demand is not a problem as per management

-

Creating supply takes time and that provides companies like Samhi with high pricing power – driving up the ARR, Occupancy and therefore, the RevPar

-

Good time to play the upcycle until the supply comes in and demand starts peaking in a few years

-

Three categories of hotels:

- Upper Upscale – ARR – 9300+ (43% of Revenues)

- Upper Midscale – ARR – 5700+ (42% of Revenues)

- Midscale – ARR – 3700+ (15% of Revenues)

-

Remains a debt heavy company, but most of the IPO proceeds have been used to pay off the debt (900Cr used for debt reduction) – finance cost has fallen

-

Management expects the growth in profitability to aid in debt reduction going forward

-

RevPAR is on the rise, growing at 20% YoY in the recent quarter

-

EBITDA margins at 32%

-

ACIC Hotel Chain acquired. Being managed by Samhi as of now, will be passed on to Marriot to manage by Q1 or Q2 FY24

-

962 rooms in ACIC Portfolio; 22% of the revenues as of now

-

As all these rooms become operational and occupied, EBITDA margins are expected to touch 40%+ (8-10% improvement)

-

Being a primarily business hotel model, occupancy on weekdays is better for Samhi compared to weekends (78-80% on Tue, Wed and Thu; 64-67% for Sat-Sun)

-

Weekend occupancy is also expected to improve in FY25-FY26 as per mgmt.

-

Not acquiring too many new hotels; major focus is on increasing revenues from existing hotels through renovation and refurbishment

-

Made provision for lease cancellation issue of around 7Cr

-

Finance cost has come down from 132Cr to 65Cr; expected to come down further as they deleverage

-

Samhi is pursuing a long term lease arrangement (which will be tied to revenues)

-

Will become a completely asset light model – reducing depreciation and help margins further

-

Expecting strong H2 performance in FY25 with new inventory boosts

-

Looking to turning profitable by Q1FY25

Risks:

- Extremely cyclical sector

- Company has a lot of debt

- Yet to turn profitable

Disc: Invested

Himachal Futuristic communication (22-02-2024)

Nice details lakshay !

If i may ask,

Q1.Who are all HFCL’s peers/competitors catering to public communication,defence and railways ?

Q2.The focus market (Optical Cables,5g products,defense fuse,defense optics) is showing any change ?

Why i asked, i wish to know wheather the focus market is showing upward trajectory and if all players in the sector are to benefit from it ?

D-Invested from ~70s, added more now its 80.

Ujjivan Financial – Small Finance Bank (22-02-2024)

Got it. The mgmt said it might take another 1 or 2 quarters.

Geekay Wires Ltd (22-02-2024)

Harsh,

For coming few quarters demand will be seen ?, If yes please let me know the rational in domestic and export.

Thank you! Highly appreciate your help.