Forgot to factor in revenue and profitability of epc segment

Posts tagged Value Pickr

3B Blackbio DX Ltd (21-02-2024)

While the points you make are true, I don’t think they are holding back the discovery of the company. I also don’t think the market misunderstands the nature of the company’s business/ operations. I make this statement basis following:

1. The company, in its earlier avatar of Kilpest, was able to get US FDA approval for RT PCR kits, and was promptly recognized and rewarded by market.

2. The company has been meeting analysts and other investment firms/community from time to time.

3. Though the company doesn’t do concalls, the presentation all through has been giving enough information to decipher COVID and non-COVID revenue.

4. The market has also realized the one-time nature of COVID revenue, with the company being valued at 2-5 PE basis peak profitability in the past.

5. Above all, in a bull market, when people are searching for reasonable opportunities, a company of such nature (by financial numbers) is sure to pop up in screeners and is unlikely to escape attention.

The one-time rerating (from 300-400 odd levels to 850 odd levels) for the company is done and dusted, IMO.

Further performance trajectory would mainly depend on the following:

1. Utilisation/Misutilisation of the cash reserves.

2. Earnings growth.

3. Ability to tap into the opportunities thrown open by UK subsidiary.

Sanghvi Movers (21-02-2024)

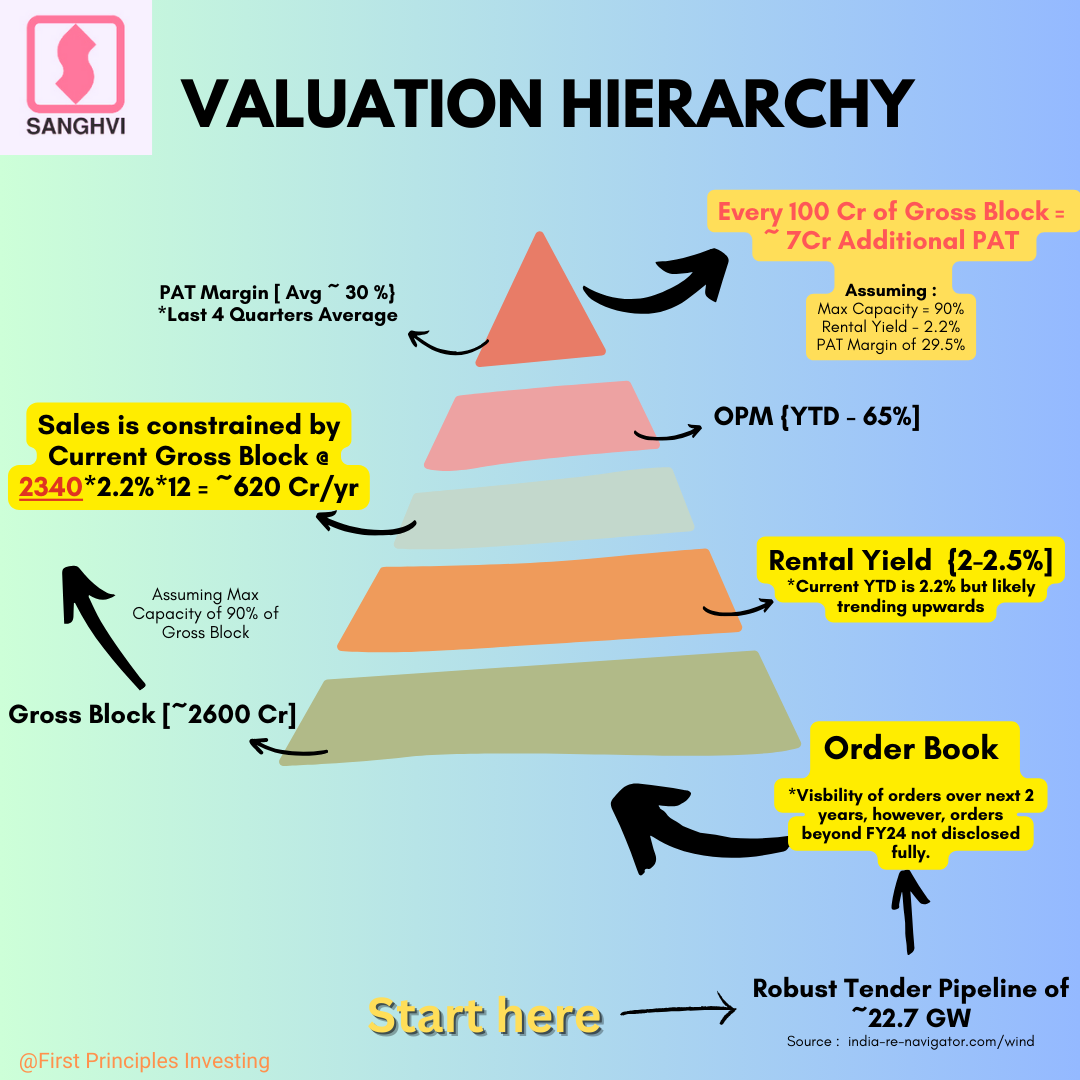

Valuation Note 3 [21st February 2024]

Current Valuations can only be judged from the vantage points of How the future turns out.

If 1 year Down the line PAT growth is 30% or higher, and there is visibility for Robust Orders even beyond that, Current Valuations are approx ~ 20X P/E

If 1 year Down the line PAT Growth is 30% or higher BUT the order book starts to dwindle, the stock will be punished. Fast & Hard.

Therefore, What is cheap or expensive is based on our understanding of the future.

The question then becomes: How confident are we that Order book will remain Robust?

Firstly, Tender Pipeline for Wind/Hybrid projects & Awarded Capacity give us confidence that this most likely will be the case (Thanks to @rcinvestor999 for updating us on the same)

Secondly, the Management Commentary is bullish (Disclaimer: Management has a strong incentive to paint a rosy picture, so this is not always the most reliable Signal)

Given a 75% Market Share in Wind Energy Sector, plus a high % of Cranes with 100 MT and above capacity (most suited for higher Hub heights), Sanghvi is well placed to milk this Wind Energy boom.

The second question then becomes: If Demand is well taken care of for the foreseeable future, what can limit Sanghvi’s Growth?

My 2 cents : Its own capacity.

Even after spending ~400 Cr this year, Sanghvi has an Soft upper limit of ~154 Cr per Quarter of Sales or 615 Cr per year.

In FY24, Its already hitting that number (Q4FY24 Sales should be ~155 Cr),

If despite a huge capex of 400 Cr in FY24, Sales have a limit of ~154 per Quarter, where’s the 30% Growth going to come from?

- Rental Yields will need to increase

- More investments in buying Cranes

| Rental Yield (%) | 2.3% | 2.5% |

|---|---|---|

| Sales (Cr) | 646 | 702 |

**Assuming Current Gross Block of 2600 with 90% Max utilisation. Sales = 0.9*Gross Block Rental Yield

If Rental yield increases to 2.5%, Sanghvi can eke out as much as ~700 Cr. Nearly 80 cr more.

So, the same Crane Capacity can accommodate at least up to ~11% Sales Growth without spending more on increasing crane capacity (i.e – buying more cranes)

But there’s the kicker, an increase in Rental Yields to 2.5% goes straight to the bottom line.

This 80 Cr, on a post-tax (25%) basis, has the potential to increase PAT from 180 to 240 Cr.

A 30% PAT Growth.

Although the probability of Sanghvi being able to hit a Rental yield of ~2.5% should be viewed with a healthy Skepticism, it is NOT entirely outside the realm of possibility.

Either way, in my view there are 3 Growth Drivers :

- Robust Order book

- Rental Yields increasing

- A Sizeable Capex Program to Increase Capacity

Personally, given my understanding as of today I am least worried about point 1. The Demand for once does not seem to be a problem. Capacity might be.

My Guesstimate is that a combination of Rental Yields and Capex is likely to drive growth.

An announcement of a sizeable capex program in the near future should be an important trigger because it would be akin to “putting your money where your mouth is”

We’ve already got a sense of what Rental Yields can do for Sales and PAT, here’s a diagram that can help us understand the impact of Capacity on Sales and its limitations.

In short, Every 100 Cr spent on Capex can increase PAT by ~ 7 Cr. This means if the co’ spends another 400 Cr, PAT Growth is likely to be just about 15% (28/180 Cr)

Hardly inspiring.

This is why I believe, Rental Yields, Capex and Op. Lev Combined would be needed to hit a 30% or higher PAT growth, a minimum benchmark for us to conclude with confidence the Stock is Currently cheap or reasonably priced.

Look forward to hearing your views. Please Feel Free to point out any errors.

Cupid Ltd – Helping the world play safe! (21-02-2024)

Adtiya buying stake in tourism finance …Any views ???

KRBL- The King of Basmati rice (21-02-2024)

Sharing my notes on KRBL

Negatives

- Brand – India Gate cannot be compared to FMCG brands. It offers 20% margins to retailers which means it cannot be compared with FMCG players.

- Market Share of Competitor – Dawaat is equally penetrating brand in India. Both companies share roughly equal market share in branded Basmati rice. KRBL is not a clear leader here.

- Ageing Rice – KRBL talks about aging rice and comparing it with wine. But fact is that India is mass market with price conscious customers, happy to buy cost effective products. This also shows up in krbl numbers for India, where only 10% volume comes from India gate classic , its most valued product.

- Exports – During last few years, there is always one reason or other for exports not working out in the middle east. It may be distributor issue in Saudi or sanctions in Iran

- Legal cases by ED in scams – This is well known to all and has been a drag for the stock during last few years.

- Management Over-optimism – MY read based on management concalls is that management has track record of over commitment and under delivery.

- Distributers – In middle east which is highest margin geography for KRBL, distributors are very powerful. They command there own brands and ask for exclusive distribution in entire country. KRBL is facing multiple issues to appoint Saudi distributor for retail and HoReCa since last many years.

- Selling price of branded rice is not independent on ongoing paddy prices for current year espically among price conscious customers.

- Growth – Pace of growth will not be very fast, as migration of people to branded rice is gradual and takes time. CAGR of 8% probably is optimistic.

- In inflationary environment, Indian cost conscious customers, trade down. Basmati is not a mass market product in that sense.

Positives

- Negligible debt / Strong balance sheet in capital intensive industry, that needs inventory built up during 6 months in a year is a feet in itself

- Buyback (350 Cr) during depressed stock price.

- Long term trend – Migration to branded rice is a long term trend in India that will be exploited in this industry by only two players.

- Adjacencies – Plans to grow by tapping adjacencies like regional branded rice, and investing in the same.

- Customer stickiness to brands, once they start using it, they dont shift to other brands easily.

- Focused on Margins – Runs operations focusing on margins, not on volumes.

- Branded Exports is more profitable than domestic business but unpredictable. KRBL does have grip here but it is not able to perform during last few years.

- Threat from FMCG players – No other FMCG company able to crack branded rice industry. Everyone has tried their hands and moved on.

- Paddy buying – Cash rich balance sheet allows KRBL to buy paddy at opportune price with minimal debt.

- Processing plant – KRBL has Largest rice processing plant in the world currently running at 50% capacity. Economies of scale will kick in at higher capacity. Difficult for anyone to compete on this parameter.

- Unity, Horeca brand, for biryani scaled up very well, which now commands 750 Cr revenue.

- Pricing power – Though perceived as commodity, KRBL does have some pricing power

- FSSAI & GST – Introduction of FSSAI standards for basmati and introduction of GST on non branded basmati, are positive for KRBL in long run.

- Advertising costs as a percent of sales is miniscule, its difficult for new player to compete without burning money.

- Competitor – LT foods looks to ME as low margin (EBITDA 9% vs KRBL 18%) and debt laden company. Its competition with KRBL is in India. KRBL commands 35% of its revenues from Middle east where LT Foods has negligible presence. At the same time LT foods generates 35% of its revenues from USA (Royal Brand) where KRBL is very weak.

Facts

- 10% Basmati produced in India is sold by KRBL

- KRBL holds a ~25% market share in the branded Basmati exports from India and a ~30% share in the branded Basmati sale in the domestic market.

- India rice consumption is 92 million ton, out if which 2 million ton is basmati consumption

Points to ponder

Growth will command investing in inventory, which means profits will be plowed back in inventory. Generally speaking, inventory is the easiest place to bury all frauds. If investor trust the inventory numbers that company claims, then business produces good ROCE on incremental investments.

MTAR Technologies – A wager on innovation meeting economies of scale (21-02-2024)

Concall notes available on screener

NCC: Extremely undervalued (21-02-2024)

Compared to 5, 10 year multiples (10-12), it’s definitely a premium of around 30%. Plus infra is a highly cyclical business so reratings don’t tend to be as dramatic as you may see in a, say, retail or technology business.

ABB India – Next Gen Technologies Power-packed (21-02-2024)

hi

Noticed a trade volume of 46 lakhs for ABB india on 21st Feb 24, result was announced today, its parent in switzerland acquired a new company, but the volume still looks way too high.

Apart from some algorithmic trading trying to manipulate it, is there any other explanation.

The reason this volume looks very high is

- no block/bulk deals that are reported yet

- one third of all retail holding will need to be traded today for this quantity (given stock holding and stock count and assuming promoter/fii/dii will not sell other than in block/bulk deal,

detailed match)

detailed math

total stocks = market cap/stock price ~ 105k cr/5k ~ 21 cr ~ 20 cr

tradable holding (only retail) = 0.075 * 20 cr = 1.5 cr

total traded = 46 lakhs ~ 50 lakhs

so 50/150 ~ 1:3 retail shares were traded. Have not seen such volume actions before. Am I missing something. The math uses a lot of rounding to make it easier to follow. Am a noob so dont know enough about this, any info will be useful.

Thanks

Apurba