Visit new website: BFBV V14

Posts tagged Value Pickr

Tips Industries Limited – Ready to RACE ahead! (19-02-2024)

Globally I think the markets are realizing the longevity of growth & terminal value that exists in these business on the back of their IP.

Monetization of music IP will only expand over the years, short format monetization has just started in the global markets and changes within streaming players wherein only streams over a certain count will be counted for monetization are some of the recent steps that further improves the monetization for these players.

In India music labels are even better placed as they have both master recording & publishing rights, plus some players like Tips have entire IP with no royalty and thus margins are higher. The growth is obviously top notch for Tips as it has gone from inefficient player to a decent player.

(Disclosure: SEBI Registered RA. Invested and Active recommendation in Research Service)

Companies with 20%+ growth guidance for next few years (19-02-2024)

Hey Nitesh, they said that in the last AGM:

I couldn’t attend the AGM but @nirvana_laha captured the same in his notes:

Also, I stand corrected that they didn’t say “next couple of years” explicitly – it was FY24 outlook.

Campus Activewear – betting on the India Consumption Theme (19-02-2024)

Further to your observations Mathew10, Asian is advertising on TV at a very high decibel clearly demonstrating the increasing competitive intensity in the industry. The loss of B2B (Udaan and Ajio) has cost Campus dearly. Maybe it stopped focusing on the offline distribution network after tasting success on the ECom platforms.

As a brand / product, Campus has a distinct hold in the marketplace.

The promoter has skin in the game (significant shareholding) and they lead from the front.

Promoter has created 2 hugely successful brands in the industry “Action” and then “Campus” demonstrating their ability.

Everyone jacks up the numbers for IPO… we all have seen it time and again… they also seem to have done the same…

As the industry turns and its stock price falls (200 odd levels may happen) the investment case for Campus should again become strong

invested…

Pondy Oxide & Chemicals (19-02-2024)

I am worried because exceptional eps of 35.6 in last Q4. Otherwise quarterly eps was around 4. Quarterly eps was POCLQtrEps23Q3…/8.71 /4.89 /3.53 /35.64 / 9.31 /10.12 /9.975 /9.055 / 12.15 /12.925/7.375 /3.845 /2.735 /0.925… 20Q2 POCL and hence I worried after result of 23 q4 if normal , ttm will drop down to 24 level from present 52 level .

Does anybody knows the reason of sudden jump in eps of 22q4?

Disc. I have exited from the stock after holding from 2016. I may be wrong.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (19-02-2024)

Sorry. I have no idea about the said target company and purported hostile Takeover bid.

Campus Activewear – betting on the India Consumption Theme (19-02-2024)

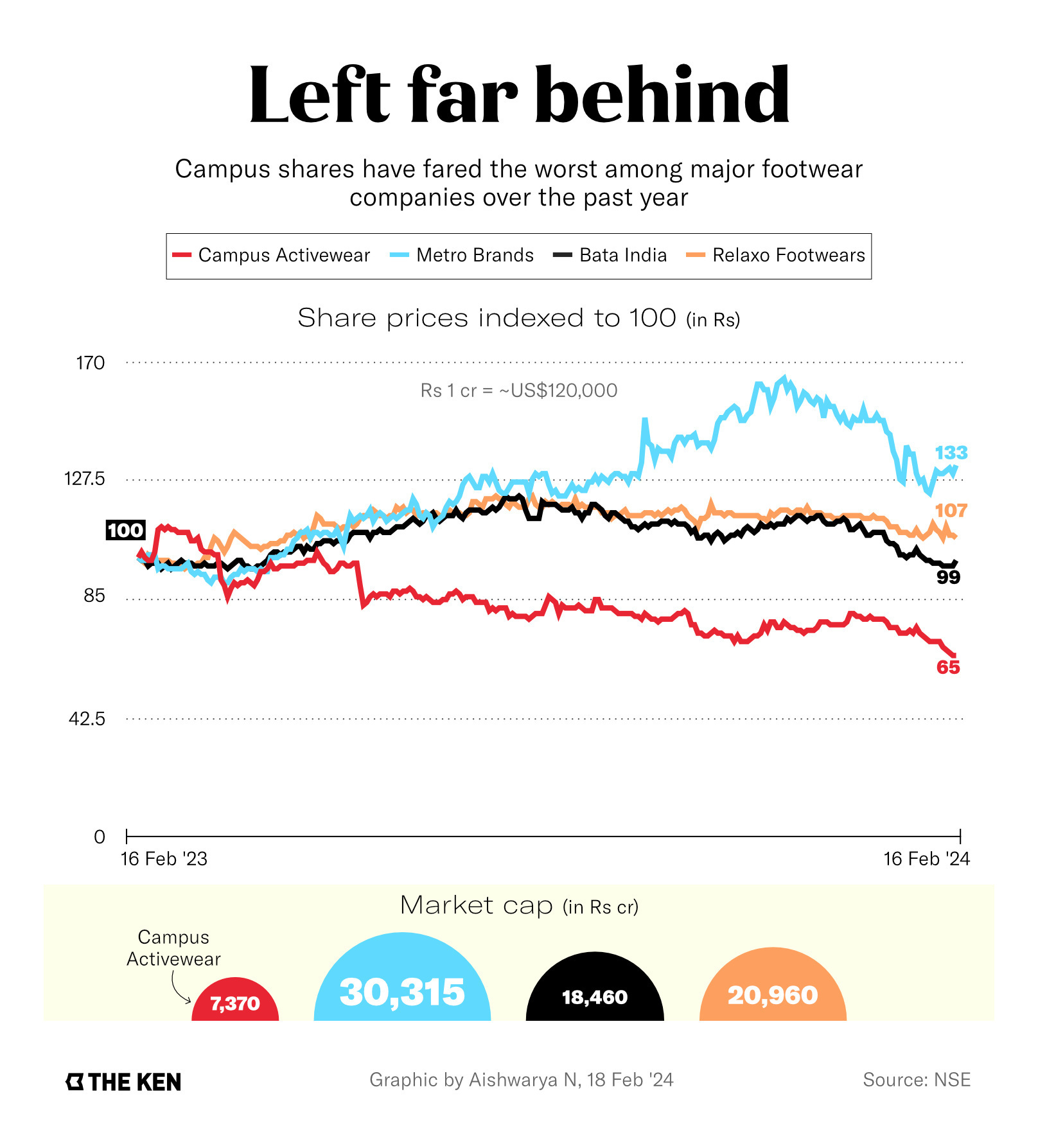

The Ken’s story today is about Campus.

It’s a paywalled story. But here are the main four talking points:

- With its cheap, trendy sneakers, Campus Activewear pipped Puma as India’s top athleisure-footwear brand in FY21

- It went public in May 2022 and doubled in value, to US$2.2 billion, in five months

- But its market cap has since slid to under US$890 million, thanks to slowing demand for its shoes and problems with e-commerce platforms like Udaan

- Campus’ biggest challenge, though, is rising competition, particularly from Abros, which is run by a former COO of Campus

Here’s the link to the full story: Campus shoes beat Puma and wowed investors. Then came the troubles – The Ken

Yasho Industries (19-02-2024)

Posting the Q3 Concall Notes –

- EBITDA Margins stood at 19.5% and PAT margins at 10%

- Increase in volume @ 21% YoY and 5% for Nine months (Signaling Demand recovery)

- Dahej Plant’s Trail run has began and since the EBITDA margins of the products from new plant is 20%+ new leg of margin expansion will come from here

- Industrial segment accounted for more than 87% of the revenue out of which export accounted for 62% total revenue

- Incorporated subsidiary in US making it area for future growth

- Downward revision in the guidence of total plant capacity → Pakhajan can do 550 to 600 crores of revenue and Vapi can do 650 Crores (earlier guided for 700 to 750) at optimum utilisation (90%)

this downward revision is just on account of correction in RM prices - The prices of RM are correcting i.e. Inching Upward, but not at the speed it dropped

- The company is seeing spark already but too early to comment weather this will be fire or fizzle down

- current capacity is utilization 85%

- Will complete trial, will take govt approvals and then only can start taking orders as client will need everything before placing orders. Will get govt certification within 4 – 8 Weeks

- Peak EBITDA will be 120 crores from Vapi facility

- Depreciation is on lower side as some asset have got fully depreciated

- Peak debt will be 500 crores including WC

- Markets will rebound overall within next 2 quarters as the demand comes back in European as well as Asian country

- Vapi is completely saturated @18% EBITDA margins any new improvement will come from pakhajan only

Jyoti Resins & Adhesives Limited (with bloated reserves) (19-02-2024)

From the last concall, this might answer your question.

Disc: Invested