Requesting the esteemed members to please elaborate on the impact this investment may have on the KSL.

Posts tagged Value Pickr

TARSONS products ltd (14-02-2024)

In the recent investor presentation Rohan Sehgal quoted the following. ” Our recent strategic acquisition of Nerbe, a Hamburg-based distributor specializing in plastic labware products, enhances

our global presence through channel partners, facilitating quicker access to larger markets. Nerbe serves as a gateway for expanding our footprint in Europe, accelerating our geographical growth in the long run”

I am already invested in Tarsons.

Jagran prakashan (14-02-2024)

I agree with your anti thesis pointers in the narrative, but in my opinion till the EBITDA margin expansion + revenue margin thesis here is intact, there is significant scope for the stock to deals with these overhangs.

Even if I am very conservative in my assumptions and take Q4 revenue as flat over Q4 last year and 20%+ margins (already delivered in Q3) as the margin base, it gives me an estimated topline for this year of ~1900 Cr. At 20% OPM, EBITDA is ~400 Cr and PAT is 200 Cr+. At even historical median valuations, there is still is significant upside in share price in my thesis. And this is base case.

What I anticipate would be bull case as like I mentioned above I expect strong revenue tailwinds from central election advertising in Q4 and Q1, coupled with the added benefit of reducing newsprint pricing and operating leverage play out. Revenue could be significantly higher than 1900 Cr for the year in that case. Projections look even much better than above if that happens. I think this is rightly reflecting in DB Corp/HT Media but not in Jagran, yet.

Not only upcoming Q4, Q1 should also be strong with the election advertising peaking in March/April/May.

Disclosure : Invested, biased. Same as above

Jagran prakashan (14-02-2024)

I agree with your anti thesis pointers in the narrative, but in my opinion till the EBITDA margin expansion + revenue margin thesis here is intact, there is significant scope for the stock to deals with these overhangs.

Even if I am very conservative in my assumptions and take Q4 revenue as flat over Q4 last year and 20%+ margins (already delivered in Q3) as the margin base, it gives me an estimated topline for this year of ~1900 Cr. At 20% OPM, EBITDA is ~400 Cr and PAT is 200 Cr+. At even historical median valuations, there is still is significant upside in share price in my thesis. And this is base case.

What I anticipate would be bull case as like I mentioned above I expect strong revenue tailwinds from central election advertising in Q4 and Q1, coupled with the added benefit of reducing newsprint pricing and operating leverage play out. Revenue could be significantly higher than 1900 Cr for the year in that case. Projections look even much better than above if that happens. I think this is rightly reflecting in DB Corp/HT Media but not in Jagran, yet.

Not only upcoming Q4, Q1 should also be strong with the election advertising peaking in March/April/May.

Disclosure : Invested, biased. Same as above

My portfolio updates and investment journey (14-02-2024)

JP ji.

What would be your rationale for exiting HFCL ?

if i remember correctly this was fairly recent addition.

Did you achieve your target or did you find unexpected development after your investment ?

NALCO – lowest cost producer of alumina and bauxite (14-02-2024)

Normally one expects private sector to do well over public sector firms

However Nalco-Hindalco seems to be one anomaly.

| Metrices | NALCO | HINDALCO |

|---|---|---|

| 1 Year ROCE | 15.1% | 11.3% |

| 3 Year ROCE | 20.6% | 12.2% |

| 7 Year ROCE | 15.8% | 10.5% |

| 10 Year ROCE | 14.4% | 8.92% |

| P/B 10 Year Average | 1.1 | 0.9 |

| P/B 5 Year Average | 1.1 | 1.1 |

| Current P/B | 2.1 | 1.1 |

| 10 Yr Sales growth CAGR | 8% | 11% |

| 5 Yr Sales growth CAGR | 8% | 14% |

| 3 Yr Sales growth CAGR | 19% | 24% |

| TTM Sales growth | -11% | -3% |

| 10 Yr Profit CAGR | 11% | 14% |

| 5 Yr Profit CAGR | 17% | 16% |

| 3 Yr Profit CAGR | 124% | 38% |

| TTM Profit growth | -24% | -20% |

Sales growth wise Hindalco has been better than Nalco over all the periods analyzed; however Profit wise Nalco has started outperforming over last 5 Years; What caused this? Since Novelis acquisition was in 2007, that cant be responsible for the bad performance of Hindalco.

Cost value chain would comprise Raw material Procurement, Production and Distribution.

Where might Nalco be performing better than Hindalco?

Price wise Nalco is almost twice its historic P/B valuation, while Hindalco is at its historic valuations.

My portfolio updates and investment journey (14-02-2024)

@ashutosh13 I shared my portfolio. I exited Paytm few days after unsecured loan slowdown alarm came through. My view on Paytm has turned more negative since then. I was banking upon their distritbution of loans which at some point of time should have given 3000 to 4000 crores of commission on disbursal of 1lakh crore of loans (in 3 years time). However, with PPBL related compliance notice, it is possible that many of the lending partners wait and watch to see how the situation is evolving. So I expect the situation to worsen before it gets better (in -terms of earnings). I am fine to be late in this than being early.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

PayTM (One 97 Communications Ltd) (14-02-2024)

The ken’s podcast on Paytm. However, there’s nothing new in it and everything that it tells is already in public domain.

My portfolio updates and investment journey (14-02-2024)

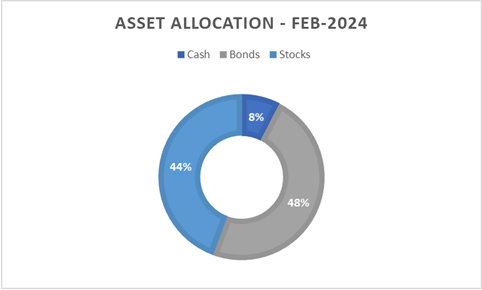

Portfolio update Feb 2024:

Post state election results in November 2023 I became bullish as political uncertainty came down drastically. However, in February screen was signaling softness. I raised my cash level as I watched earnings of the companies. Cash/bond now accounts for 56% of my net-worth and stocks 44%. I have shortlisted stocks where I want to ramp-up my position in the next few months.

I remain bullish on bonds as I think we are likely to see rate cut this year and that will have positive impact on bonds. Inclusion of India in various global bond indices will also percolate to private sector issuers. Some of the bonds in AA rating category continue to offer 10%+ yield. I expect my bond portfolio to provide 12% CAGR in 3 to 5 years due to rate cut over the next two years.

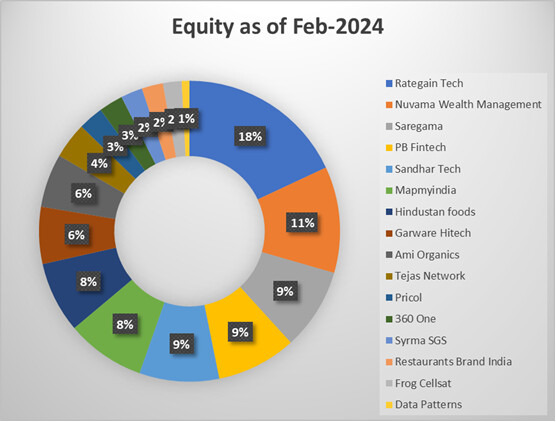

Equity portfolio:

I made a big decision of exiting Bajaj Finserv in this quarter. I was holding the stock for over 8 years and was anchor of my portfolio. I have become very sensitive of valuations I pay. So based on the combination of earnings and valuations I exited Shivalik, Permanent magnets, Clean Science, Tatva Chintan, Neogen Chemical, NAM-India, Divgi Torq and HFCL. As of today, I don’t have any R&D stocks in my portfolio.

As a result, concentration of my portfolio has increased. Now I own 16 stocks, top 5 account for 55% and top 10 – 87%.

| Feb-24 | Jan-24 | Aug-23 | Nov-23 | |

|---|---|---|---|---|

| Total stocks | 16 | 21 | 23 | 22 |

| Top 5 allocation | 55% | 46% | 42% | 38% |

| Top 10 allocation | 87% | 74% | 71% | 71% |

New entrants are Syrma (re-entry), Restaurant Brands India, and Data Pattern.

I ramped up positions in Nuvama, Garware Hitech and Sandhar owing to great results.

Trim mode: Rategain is the only position which I intent to trim due to size. Results were fantastic. Mr. Bhanu Chopra has talked (in couple of interviews) about his aspiration to make the company a USD1 billion-dollar revenue company.

Tejas Network has been a big blow, down 23%, since I bought it. Results were also below my expectations. I hope company changes its trajectory from Q4 FY24. Margins I think will remain an issue. As it’s a Tata company I am fine to give it one or two more quarters.

PB Fintech and Rategain were the big winners in the last 3 month.

PB Fintech: Earnings momentum is strong. I am not sure of the outcome of tax survey but this company is at inflection. About 35% of incremental revenues is going to flow to EBITDA and bottomline. If take rates remain at same levels then by FY30 company should have topline of over 10K crore and PAT & EBITDA of over 3K crore. However, big risk is take rate (commission) suppression.

Anyone interested in PB Fintech kind of business then should read up on Goosehead Insurance in USA. This company is growing at over 30% rate from past several years despite being in low growth market. Their commission rate is 14%. Why I am mentioning this is because some of the investors think that commissions will be made 0%. If in USA, which is well penetrated market, commission is paid then it will not be taken away in an underpenetrated market like India. In fact, in March 2023 IRDAI removed the cap on commissions, earlier it used to be 20% and before that it was in 30% vicinity. I think PB fintech take rate is in 10-15% vicinity. Take rate reduction remains a risk and an investor should be able to react accordingly. Nevertheless, premium growth for PB fintech in my view shall remain in current trajectory of growth 30-40%.

Saregama continues to be below par. However, with industry change (paid subscription vs. ad supported revenue) I am expecting its earnings to bottom out in next couple of quarters and start showing 20% earnings growth from Q2 FY25. Finger crossed.

MapmyIndia: results were in line with my expectations. They won a big order of 400 crores with Hynduai and Kia. This order is almost 40%+ of order book they declared at the beginning of FY24. I am also excited for Q4 FY24 like the management.

Nuvama: Q3 FY24 earnings are very good. However, an investor should be careful of its high revenue in capital market segment. Capital market segment would be cyclical and any negative market sentiments may impact this segment’s revenue.

Please do not tail or copy my portfolio as you can see, I have a high churn and I can sell or buy any position at any time before informing/updating this group.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

Jyothy Labs ~ Post acquisition of Henkel India (14-02-2024)

Jyothy Laboratories –

Q3 FY 24 concall highlights –

Sales – 678 vs 613 cr ( up 10 pc- all volume led despite overall sluggish demand trends for FMCG industry )

EBITDA – 119 vs 84 cr ( margins @ 18 vs 14 pc – due fall in RM prices )

PAT – 91 vs 67 cr ( up 35 pc )

Fabric Care sales – up 11 pc ( includes wash and post wash categories ). Liquid detergents growing at a fast clip – both Henko, Ujwala liquids

Dishwasher sales – up 7 pc

Household Insecticides sales – up 5 pc ( category facing headwinds for quite some time now ). Company focussed on selling Maxo – liquids. Onboarded – new brand ambassador – Kareena Kapoor for the brand

Personal care sales – up 22 pc !!! ( Margo – new variants did very well )

Have been investing aggressively in expanding distribution depth and alternate distribution channels

Company is aiming to do a topline of 5000 cr in 4-5 yrs

Not focussed on M&A activity at the moment – at the same time, not averse to it ( primary focus is on organic growth )

Henko – liquids growing at rates much higher than category growth

Have slowly started taking – Ujala, Moonlight, Mr White detergents to more and more states

Company was distributing to 11 lakh retail outlets in Mar 23. Aim to hit 12 lakh outlets by Mar 24. This should help volume growth going forward

E-Commerce sales as a percentage of company’s sales at 6 odd pc

Company has worked a lot on the Margo brand, have innovated and launched new variants. Still lot of scope for this brand to grow. Likely to launch new products under the Margo brand name

Have under-levered brands like – ‘Fa’ in their portfolio. May re-launch them at some point in time

Since Liquid detergents, personal care categories are doing well, the gross margins are improving

Disc: hold a tracking position, biased, not SEBI registered