dcx system research.pdf (1.3 MB)

complete research report by KR choksey

dcx system research.pdf (1.3 MB)

complete research report by KR choksey

dont know why they even have a call… they dont have answers for anything…

what i understand is that there is no compulsion for companies to have a investor call – then why do they even have it !!

promoter doesnt even know how much of capex company has been done… it is a small company… not a reliance…

Discl – have got fed up and exited.

Q3 FY 2023-24 Quarterly Results

Financial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b957fc84-7ce5-4387-bae0-e63f28ae3701.pdf

Vaibhav global seems to have gotten in wave 3.

Fundamentally, the business has reported a good result recently and looks ripe for operating leverage to kick in once the sales growth is back.

Requesting views from technical folks ( @hitesh2710 @phreakv6 and others ) on the chart

Hi @banjobaj,

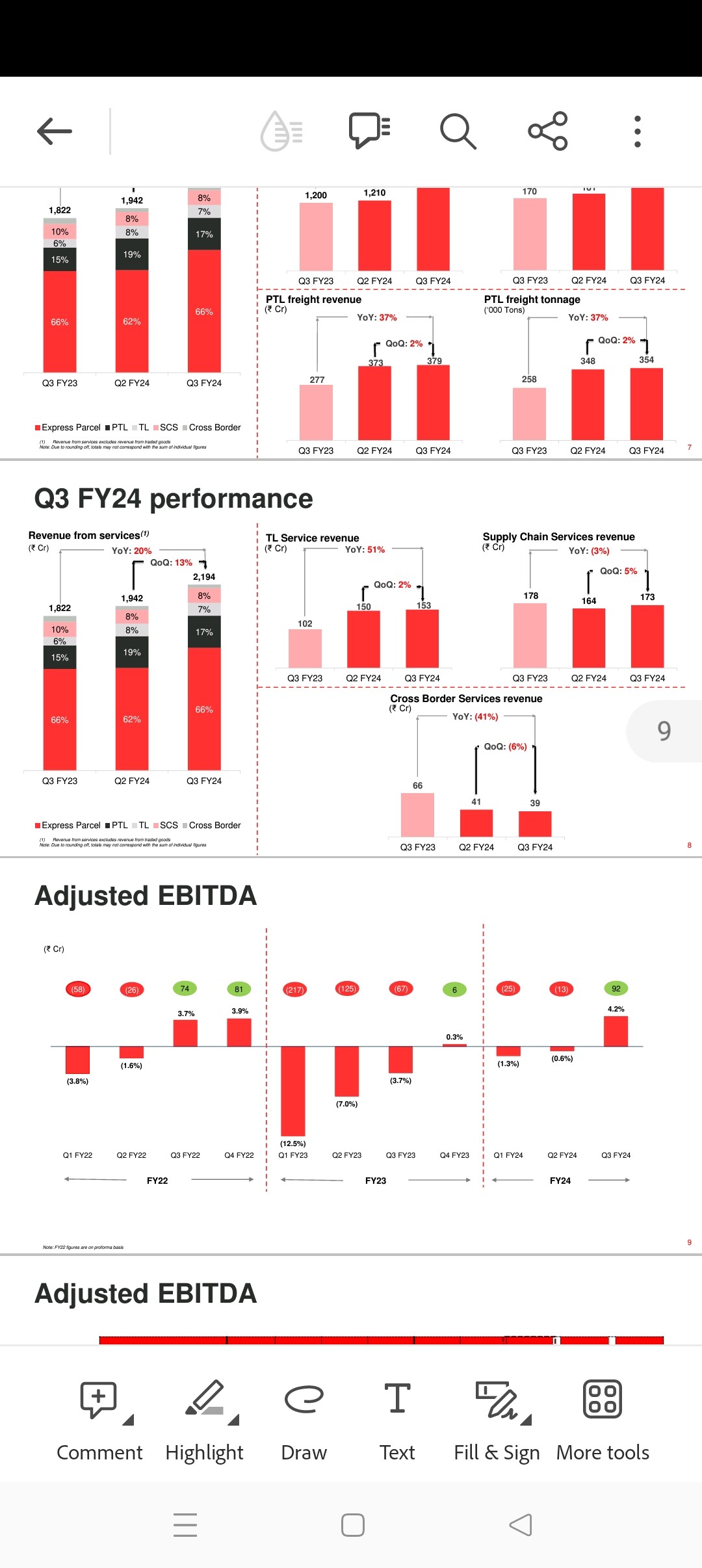

Delhivery’s part truckload (PTL) segment is the one into B-B express which has grown from 273 cr to 373 cr y-y in their q3 this year which is 17% of their revenue. (Check the screenshot-1 from their q3 presentation)Mahindra logistics also has B-B express (from Rivgo ). Both of them have aggressive expansion plans like our TCI express capex plan of 500 crores for fy-23 to 28. Please check this delhivery interview in CNBC for quick reference.https://youtu.be/MKDFzktOLP8?si=xNMAuyFl_oqZ58Nt

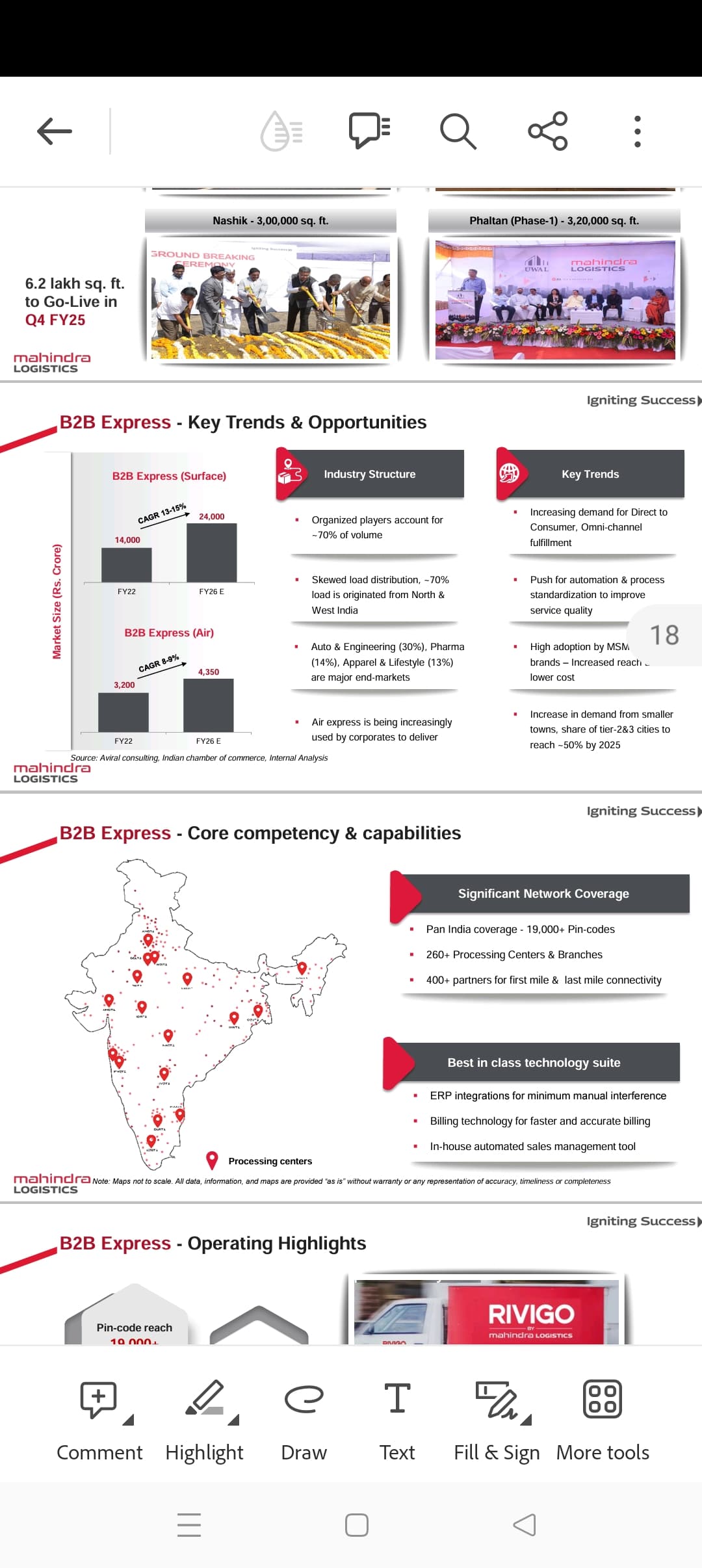

Delhivery is putting in 7% of their revenue as capex until Fy27 and 4% later on, with focus in PTL segment as that is the bigger opportunity. I am attaching here yearly growth guidance in Mahindra for their B-B express for your reference.

Overall PTL B-B express works like a niche space where service differentiation like delivery speed etc let the players enjoy a premium. Service offerings mix also varies among different players.New service offerings such as rail express, pharma cold chain express in TCI express is expected to grow faster. Business models also varies like PTL in Delhivery doesnt follow traditional hub and spoke, bit something different called Mesh. TCI is the most asset light one in my understanding as they dont own trucks. Competition is expected to intensify with aggressive capex plans to grab market share from unorganized and many of the peers will enjoy economies of scale and operational efficiency etc in coming years.The main worry for me is as with TCI express ‘s adamant stance on not giving away a bit of margin, will they be left far behind.?Delihivery reporting their first PAT was a surprise for me last quarter.

Those with deeper industry knowledge can comment better in comparing competitive advantages and who could potentially gain the most in coming years.

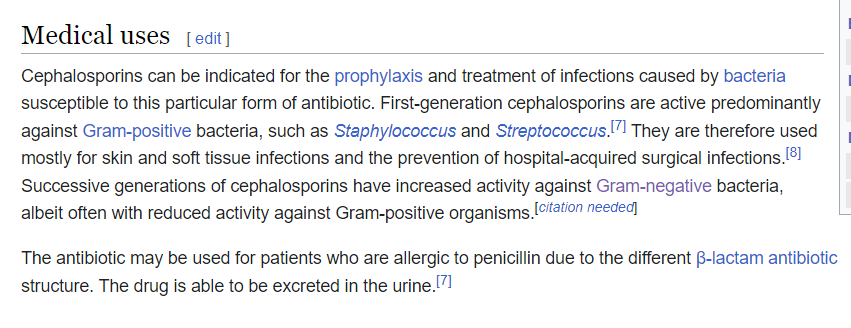

above image explains why gram negative bacteria are more difficult and pose serious threats as compared to gram positive bacteria.

The cephalosporins (sg. /ˌsɛfələˈspɔːrɪn, ˌkɛ-, -loʊ-/[1][2]) are a class of β-lactam antibiotics originally derived from the fungus Acremonium, which was previously known as Cephalosporium.[3]

Together with cephamycins, they constitute a subgroup of β-lactam antibiotics called cephems. Cephalosporins were discovered in 1945, and first sold in 1964.

Cephalosporins are bactericidal and, like other β-lactam antibiotics, disrupt the synthesis of the peptidoglycan layer forming the bacterial cell wall. The peptidoglycan layer is important for cell wall structural integrity. The final transpeptidation step in the synthesis of the peptidoglycan is facilitated by penicillin-binding proteins (PBPs). PBPs bind to the D-Ala-D-Ala at the end of muropeptides (peptidoglycan precursors) to crosslink the peptidoglycan. Beta-lactam antibiotics mimic the D-Ala-D-Ala site, thereby irreversibly inhibiting PBP crosslinking of peptidoglycan.

Third-generation cephalosporins have a broad spectrum of activity and further increased activity against gram-negative organisms. They may be particularly useful in treating hospital-acquired infections, although increasing levels of extended-spectrum beta-lactamases are reducing the clinical utility of this class of antibiotics. They are also able to penetrate the central nervous system, making them useful against meningitis caused by pneumococci, meningococci.

Ceftobiprole has been described as “fifth-generation” cephalosporin,[34][35] though acceptance for this terminology is not universal. Ceftobiprole has anti-pseudomonal activity and appears to be less susceptible to development of resistance. Ceftaroline has also been described as “fifth-generation” cephalosporin, but does not have the activity against Pseudomonas aeruginosa or vancomycin-resistant enterococci that ceftobiprole has.[36] Ceftolozane is an option for the treatment of complicated intra-abdominal infections and complicated urinary tract infections. It is combined with the β-lactamase inhibitor tazobactam, as multi-drug resistant bacterial infections will generally show resistance to all β-lactam antibiotics unless this enzyme is inhibited

Q3FY24 results – https://www.bseindia.com/xml-data/corpfiling/AttachLive/4a93bd5d-47c7-46ad-8f3f-cc4704d5b74b.pdf

Sales have grown 65% YoY and OPM have expanded to 14%

chart also looks great with consolidation ongoing for the last 6 months.

It’s just profit booking. Since stock has 5% circuit limit (under ASM), it has been in Red for last few sessions. I believe it’s corrected 25% from the top, in the last 3-4 sessions, which is pretty much the same for all small caps stock that ran too much ahead of their valuations in last 1 year.

I believe it’s more of an industry issue. All the logisitcs companies (VRL, Navkar, Allcargo, Mahindra Logistics etc) have come up with bad numbers, much worse than TCI express. But I can’t figure out what and where the issue is in indian logistics industry. I thought with uptick in economic activity, logistics sector should have a natural tailwind.