Due to qip promotes stake comes down not aware about others. For this u can check investor presentation it is mentioned in the presentation

Posts tagged Value Pickr

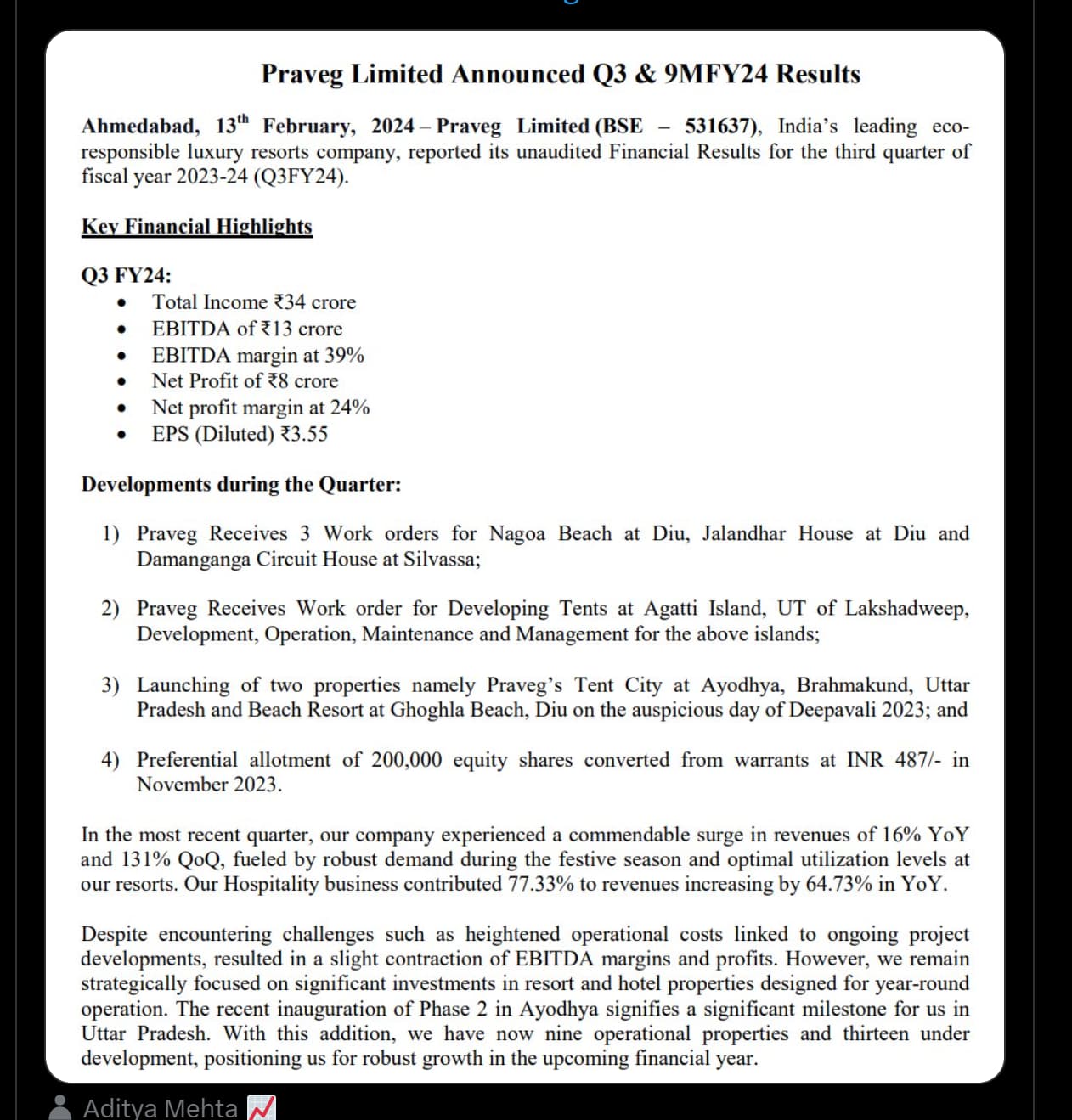

Visaka industries ltd (13-02-2024)

Of course, results are not good. However, the clear technical breakout and stupendous volume buildup, the historic wipeout with two tall bars, leave me asking for more, more information, that is. The results – and – move, are on two extremes and can leave one perplexed.

I will study the line item breakdown this weekend. On quick glance I saw building materials increase but zero mention of the solar business (why!!??). I wish we had an investor presentation and management call, both of which seem to be missing.

We also have a Multi year Darvas box, looking to be broken.

Why would a big name buy 8lac shares a day before results?

Why is there no indication and guidance on the solar roofing vertical – which is the flavor of the (next 3-5?) year(s)?

Would be great if someone could do some scuttlebutt.

TCI Express – Logistics Sector niche player (13-02-2024)

They have been consistently under delivering after overpromising over the last few quarters. I feel the management tries to sugar coat instead of conveying challenges and measures being taken to address them. I would have expected them to grow at GDP+5%, but they are unable to do so. I had entered at much lower levels and exited today after seeing multiple quarters of business underperformance.

Everest Kanto Cylinders Ltd. – A long runway ahead! (13-02-2024)

This particular company has been chest thumping for a long time, it’s up to us to understand and act upon their messaging

PayTM (One 97 Communications Ltd) (13-02-2024)

Clarifying again with facts and not opinions:

- Paytm’s ECL is 5% which is high in lending domain (and that too when the defaults haven’t peaked as they are fairly new in this domain). Irrespective of the topline their bottomline will be wiped off with the ECL as that would be extended in some form of FLDG/cost sharing.

- Never said Postpaid was there revenue generator, but it forms bulk of their entry to other loans. It acts as a major feeder for personal loans, as it serves as a great underwriting mechanism in a short period as well as keeps customers from changing platforms. And this will be absent.

- With regulator’s action none of the lenders will want to participate with Paytm as a partner, as it will be viewed as going against regulator. Hence, mentioned the cryptocurrency topic.

- Paytm in only personal loans (not postpaid, not merchant loans) is not in top 5 and is even further beyond. To find names one can go to Google Playstore and find the apps ranking in Finance category. The ones doing lending among them in top 50 were doing more than what Paytm did last way back in FY23 end. (not namedropping companies as all of them are unlisted, PhonePe, Google are not the ones).

- Regulator never takes their step back and they have been taking action against Paytm for six years now in one form or other, hence the deadline has very minor chance of extension but almost impossible to reverse.

Few points to others that I noticed in other posts:

- No Paytm cannot get the CIBIL data of customers without their express consent even if they are doing bulk of their transactions using Paytm.

- Their UPI services will be up and running before the deadline, but the merchants KYC will need to be done for their wallet business and that is going to cost any entity a bomb (that’s in news today also).

- All PPBL services can be routed through other banks and in the future Paytm will get it done. PPBL was most probably a profitable entity, but the addition to the topline wasn’t much. However, the quoted figure by management as revenue drop is going to be much more than stated in the call.

Opinions:

- In any other field, still you get forgiven after sometime. In financial services, it takes a long long time to get your reputation back. Regulator doesn’t take extreme steps all of a sudden. So a lot must have been actually wrong with the compliance and regulatory stuffs at Paytm.

- Lending was the way ahead for major revenue generation. But with reputation loss and lending coming to a halt, the defaults are bound to go up and it will lay more difficulties for association with Paytm.

- When there are tons of stocks giving spectacular returns why gamble with something that is surrounded by so much negativity. Yes you may lose a bounce-back opportunity but the risk reward ratio is not in your favour.

Everest Kanto Cylinders Ltd. – A long runway ahead! (13-02-2024)

Concall was such a huge waste of time. Ended before 30 mins. Management couldn’t answer beyond a few staccato; analysts couldn’t, therefore, ask anything substantial.

PayTM (One 97 Communications Ltd) (13-02-2024)

The only problem here is that front end (PayTM i.e. OCL) and backend (PayTM payment bank) has almost same management (all main 3 people were on board of PPBL – Mr. Mahur has now left the board) so in phonepe case there was no linkage b/w yes bank and phonepe in terms of management. I hope they give the same treatment as they given to PhonePe but here it is a little a bit different case.

Bandhan Bank – in a sweet spot? (13-02-2024)

NCGTC forensic audit of evergreen loans

Same issues are raised last year around April 2023.

Waiting for the outcome to size the issue (if they found any)