I may be interpreting this news incorrectly. But, MFs (HDFC amc) , Insurance entities (their investment portfolio) etc are looking to increase holdings in these banks. Due to being promoter of these entities, HDFC bank has to take approval.

It is not the case the that HDFC bank is increasing holdings in these banks.

Posts tagged Value Pickr

HDFC Bank- we understand your world (11-02-2024)

Rategain – Fast Growing SaaS Leader (11-02-2024)

Q3 Fy 24 Concall (held in Feb 2024)

Increased revenue guidance to 69% from 60%

Organic growth will be 20-25% CAGR, Target to double the revenue in 3 yrs – 26% CAGR

Cash 1000-1050 cr

Actively looking for acquisition, typical range is 150-200 cr

Beat revenue and margin guidance given post IPO

our top 20 customers can give us $20 million each. Our 20 to 100 customers can give us 5 million and 100 to 1000 can get us a million

It is less than a percent in terms of revenue contribution from India

Disc: Invested

How to take leverage to go long in market (~2 years)? (11-02-2024)

I have been leveraging my portfolio and this has actually given me an edge while hunting on special situations & Small cap opportunities.

I mitigate the double whammy situations by dividing my Pf into large caps and compounders. Large caps is where i have subtle return expectations (Bluechip preferably). I have RIL, LTTS & Infy in my PF.

The lower returns should be compensated by the other half of the PF.

Also, There should be at least 25% more securities pledged up and above the bank’s 50% margin Or else they will destroy our cibil as well as spam us with margin requirements.

Used to have kotak & now moved to Yes bank due to service issues.

Just shared my exp

HDFC Bank- we understand your world (11-02-2024)

HDFC Bank instead of selling it assets is currently planning to increase its stakes in six other banks. Indus, Axis, Bhandan, ICICI (![]() ), YES, . It baffles me why is the Bank becoming a bank holding company. Do they feel other Banks can grow faster than them and hence spending money in acquiring these stakes will help them?

), YES, . It baffles me why is the Bank becoming a bank holding company. Do they feel other Banks can grow faster than them and hence spending money in acquiring these stakes will help them?

This contradicts management saying they can grow 20% BTW they feel ROE will come down for sure in the medium term which means EPS will slow down to 15 % to 16% growth.

I believe HDFC was merged to hide some big NPAs in its real estate book and protect the market cap of HDFC, as you know most of the management is compensated via stock as well. Need to dig in Deep.

HDFC bank’s advantage is its corporate book and its underwriting which only keeps it at the fair value of 2 times book.

Right now it is a good bet for 15 % to 17 % CAGR for the next 5 years which is not bad for big mutual funds and people who cannot find better opportunities.

Disc: Started tracker position HDFC bank will wait to pick up more when the upside is higher.Portfolio here

Chirag’s Portfolio (11-02-2024)

I have invested in Jubilant ingrevia considering the segments they are working on and future capacity expansion. Recently there have been lot of profit degrowth in the company. Can someone share their views on the company and thesis on revival of the chemical industry?

Globus Spirits (11-02-2024)

Why broken rice is important for alcohol companies:

Understand costing aspects:

Case 1: Revenue / Lt of Bulk alcohol: Rs 64.00

Animal feed & other products: Rs 10-12.00

Total Revenue: Rs 74 -76.00

RM cost: Broken Rice 2.2kg X 26/-: Rs 56-57.00

Gross Margin on Case 1: Rs 18-19.00

In %: ~ 24%

Case 2:

RM cost: Broken Rice 2.2kg X 20/-: Rs 44.00

On the same line, Revenue will also come down by Rs 6.00/- to 58.00/-

Now Total revenue: Rs 68-69.00

Gross Margin on this case: Rs 24-25.00

In %: ~ 35%

Hope you can understand both case scenario. Now come to full costing mechanism

Power Cost: Rs 9-10.00 per ltr

Net Margin: Case 1: Rs 9-10.00 and Case 2: Rs 13-14.00

So Net Net Rs 5-6.00 is impact on EBITDA margin, which is 7-9%.

Ambika Cotton Mills (11-02-2024)

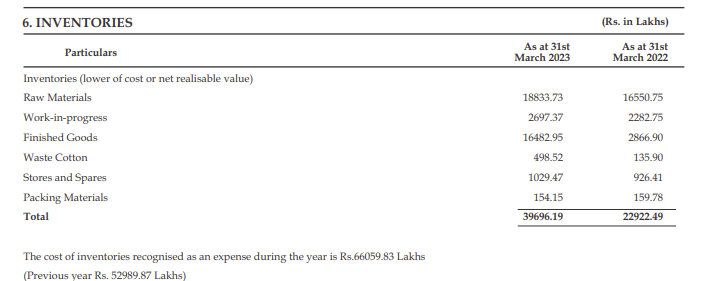

As per the last BalanceSheet published in Sept23, Cash Equivalent was 234Cr; whereas short and long term borrowings were ‘Zero’. Am not able to understand what is accounting for this Interest cost?

The inventories at 496Cr!! Almost 96Cr rise in last 3 quarters!!

More than 2 quarters of sales is tied up in inventory…

If its raw cotton inventory, why do they speculate and buy so much in advance… Does it show that they are not able to pass down the increased raw material cost and hence consider hoarding cheap raw material as their real moat…

What if the cycle does not turn soon and they are forced to liquidate at the low point of the cycle after holding for long? Why cant they hedge through commodity exchanges. Currently they are not doing the same, check point 6 below from their last annual report.

I was hoping that finished goods would be a small miniscule portion of this inventory, since that would loose value as the fashion fades in future. however the below disclosures in their last annual report (Mar23 data) are a little worrying. Raw Material had increased slightly from 165Cr to 188Cr, however Finished Goods had increased from less than 29Cr to 165Cr. (as per last annual report). Only hope can be that the FG is majorly in yarm form rather than knitted as mentioned by @sunilkumarca3101 above

But pls note that Knitted Fabrics is more than 22% of Revenue while Yarn is 64%; so inventory can be in similar ratio…

Disclosure: Holding since i consider it cheap, however now worried that it maybe cheap given this reason of growing inventory over multiple quarters…

Burger King ~ Whopper of an Opportunity (11-02-2024)

In terms of the menu, BK has mutton which is not on KFC/McD menus. BK has created a menu at the intersection of McD and KFC – Burgers, Wraps, Nuggets, and Chicken Wings including Boneless and Grilled Chicken. (Plus a little nudge into Taco Bell territory with Veg/Chicken Tacos)

The domination of non-veg items in the menu is bound to give BK a higher per-order value and they should in fact make sure they are priced higher than McD on most items to have the premium factor, other than some value offerings which they can retain to compete for the lower-order value customers.

On the question of people preferring one brand over the other, I feel like each brand will develop its loyal customers and over time price will not be such a big factor, just as McDonald’s offerings have gone far beyond the low-price value items and into McCafe + Gourmet burgers category.

While a smaller point, I also feel McDonald’s success so far could become a positive for other brands as just being located in the same food courts/malls could see other brands gain from McD’s waiting time

KSE Limited — Interesting Business (11-02-2024)

Nothing disclosed in public till now.

Sai Silks (Kalamandir) – only listed player in the organized saree market (11-02-2024)

Concall Highlights:

- Market Challenges: Ethnic wear market facing slowdown due to factors like cyclone impact and reduced purchasing power in Andhra Pradesh, Telangana and Chennai due to water clogging.

- Store Expansion: Company added 4 new stores and plans for more, indicating growth despite market challenges. In Chennai plan is to have from 2 to 20 stores. In Karnataka only have store in Bangalore. Kerala is not discovered. Andhra and Telangana can still accommodate 20 to 25 stores. 100 stores in Southern states are possible.

- Financial Performance: Last year’s revenue was 378.6 crore with a gross margin of 39.80% and a net profit after tax (PAT) of 31.3 crore (8.28% margin).

- Customer Base: Approximately 50% of customers are repeat buyers, highlighting brand loyalty and value proposition.

- Gross Margins: Gross margins vary from 25% to over 60%, averaging 40%, reflecting a diverse product mix and pricing strategy.

- Sales Growth Target: Targeting 3-4% like-to-like sales growth, indicating a focus on improving operational performance.

- Geographic Expansion: Focus on expanding in Tamil Nadu, with plans to increase stores from 2 to 20, tapping into the lucrative silk sarees market. Additionally, potential for significant store additions in Kerala, Telangana, and Andhra Pradesh.

- Market Dynamics: Chennai market commands a 15% premium over Hyderabad, indicating potential for higher margins.

- Competition: Transitioning from unorganized to organized competition in Tamil Nadu, with 30% currently organized, suggesting opportunities for market share gains.

- Market Size: Total addressable market (TAM) estimated at 50,000 crores for Tamil Nadu, indicating significant growth potential.

- Marketing Strategy: Planning to increase marketing spend by 3-4%, suggesting a focus on brand awareness and customer acquisition.

- Same Store Growth: Slightly negative on a blended basis, indicating the need for improved performance in existing stores.

Store expansion and revenue growth to be seen in numbers. Total Address Market is huge.

Disclosure: Invested