But then, the market may go down in the bull market also. There is no delimitation between the bull market and a bear market.

Wouldn’t a fall when you buy in a so-called bull market affect you?

Isn’t ‘buy cheap’ the mantra?

But then, the market may go down in the bull market also. There is no delimitation between the bull market and a bear market.

Wouldn’t a fall when you buy in a so-called bull market affect you?

Isn’t ‘buy cheap’ the mantra?

Last three Quarters `Preformatted the EBIDTA for Ambika is down vs their historic 20 %. Working capital interest cost has increased 3 times vs last Dec though they have so much money in FDs. Promoters are not finding use of the cash, they are not expanding or buying. It is good though 1large portion of electricity is now with the wind.

Hope this compression in EBIDTA is due to the high-cost inventory of cotton that they carry not because of loss of margins for good.

Disc: Invested since 2017 here

Q3FY24:

• 97cr new awards for the quarter. Order Book at Rs. 1200 Crores.

• International: Deep International DMCC has supplied a modular compression station for a client in Egypt to counter well head pressure reduction and maintain well head gas production. The project was executed on a Build/ Own/ Operate basis with the partner in Egypt.

Middle East Fast Track Compressor Overhaul – The Company has supplied quantity four gas compressor packages for a debottlenecking project in Gulf for a client.

Deep Onshore Drilling Service Private Limited, a subsidiary company of Deep Industries, entered into a JV with Euro Gas Systems to enhance the company’s technical expertise and know how to further support gas field services.

• Beluga International DMCC100% Dolphin owned subsidiary incorporated in Dubai The charter hiring of Dolphin’s Barge would be done under this entity

• Kuwait Oil Company (One of the largest Oil Producer in the world) exclusively shortlists qualified enterprises, with Deep, being one of the selected few. Moreover, the favourable day rates in the Gulf region should potentially enhance our margin expansion.

• The industry exhibits relatively subdued competition, largely attributable to its significant capital-intensive nature, operational efficiencies and extreme discipline in leverage.

• a history of never exceeding a D/E ratio of more than 1, signifying sound financial management and a low-risk profile.

CONCALL NOTES:

• Bidding pipeline of around INR500 crores plus with increasing trend.

• Demand environment is particularly looking very exciting, as fresh large capex plans have been announced by not only the PSUs, but also large private players. Further, the current demand scenario is so strong, the services business like us are operating at nearly full capacity, which is facilitating benign pricing environment in medium to long term. Strong demand environment, coupled with benign pricing outlook is ensuring profitable and durable growth in coming years

• In oil and gas, Vedanta Group Company has announced $700 million investment to enhance drilling infrastructure at its 100 exploratory wells in the country. We remain optimistic about the robust bidding pipeline for Deep, which is expected to remain strong in foreseeable future.

• DOLPHIN OFFSHORE: On a full year basis, expect almost INR90 crores to INR100 crores top line from Dolphin. Dolphin, we are looking operating margin of more than 50%.

We have already started giving some expressions to our clients. We are working on bidding some of the tenders in offshore space. So I think it will still take us a quarter more to get – because there was a lot of things to be done to revive the company, get the documentation done and all. So I think in next quarter, we should be in a position to bid for these tenders. And we can – we are sure that we will have a huge amount of outcome coming in because as it is, there is a huge demand in the industry and there is a lot of vacuum for the services provider in this segment.

• 20-25% sales growth for next FY. So, we are anticipating minimum 25% growth year-on-year in Deep Industries itself. So, the way our bidding pipeline is increasing and the conversion which we are expecting out of this bidding pipeline can definitely help us in growing 25% CAGR.

• Steady state operating margin should be in the range of 42% to 45% EBITDA

• Euro Gas (EPC JV) tender is already bidded and it is under evaluation and we are expecting the tender to convert soon.

• KUWAIT OIL: So, in Kuwait Oil, we got qualified for various capacities of rigs. The tender is already published by Kuwait Oil Company. And I believe it is due in March or April. So, the size is huge, but our company in India intending to bid some of the rigs in that region. So that will depend on the market intel that we are working on. So having said that, getting qualification in KOC in itself is a big task. So, once we have got qualified now, that stands another chance that we would be allowed to bid for those tenders. Outcome, of course, depends on the tenders once they are submitted. But the opportunity is big. In terms, I believe they would be asking more than 25 to 30 rigs, although we are not going to bid for all of them, maybe a few of them. But that will depend as the dates progress near.

• 2 NEW RIGS: Selan rig is already under mobilization and maybe a week from now, the operations will start. Regarding the rig that we had ordered for Bokaro is already ready. We had already done a third-party inspection. It’s lying in China. So, in all probability, we expect that the rigs would get shipped in March and we would be in a position to start the operations probably in April or May.

Q3 and Q4 put together, the quantum of capex would be around INR100 crores.

• Q4 to be better than Q3.

I dont think comparison with Apple is fair. Apple is an aspirational brand across the globe. Forget the US, there is no competitor across the globe that offers Apple like experience with owning Smartphones – atleast in the minds of people.

Coming to HDFC Bank

The positives –

The Constraints –

All in all for those seeking consistency with comparatively lower volatility in business performance, HDFC Bank could be the go to bank. For those seeking a higher return albeit with higher risk, other banks offer great value.

Disclaimer – Recent entry in HDFC Bank futures below 1500 and writing calls against it to generate consistent income. Holding multiple other banks as well with a higher weightage in the overall holding.

Problem with leveraging in down market is that if the market goes down further or doesn’t go up quickly, the value of shares pledged can go down and you will get a margin call. You will have to pledge more shares or the bank will sell them at rock bottom price. This will give a double whammy and can take you out of the game. It is very common in FNO traders.

Cross posting from another thread:-

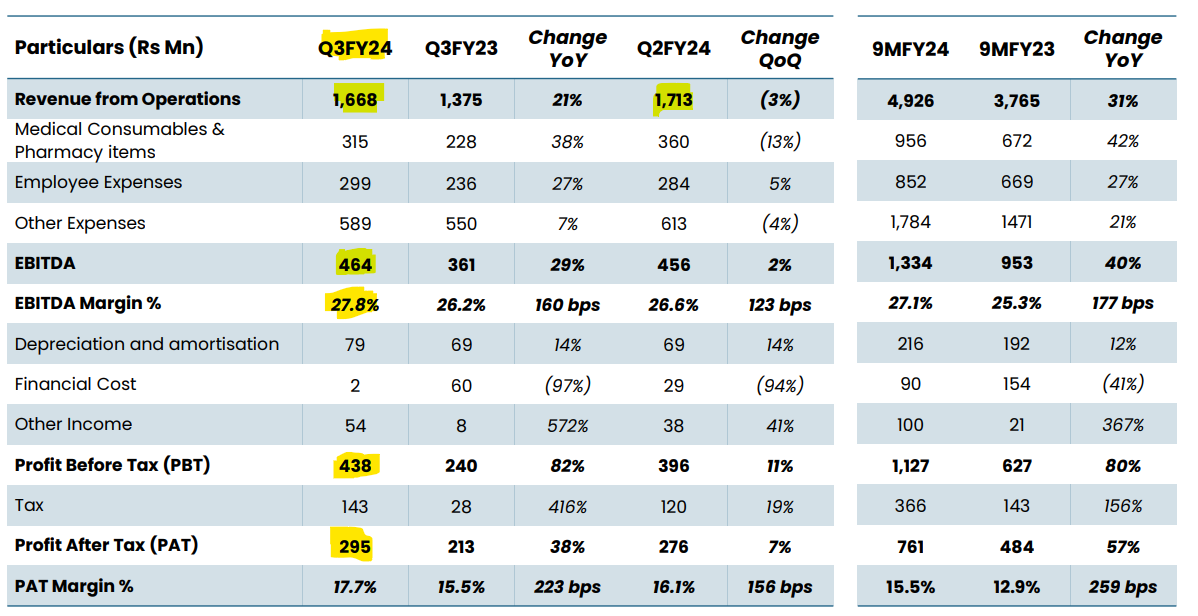

Yatharth Hospitals posted its results yesterday:-

Can someone help explain to me if Q3 has any sort of seasonality? I don’t see a reason for QoQ degrowth otherwise.

Anyways, posting few of my observations:-

To build on this further, the Noida extension occupancy is currently at 45% and the company is undergoing a brownfield expansion to add 250 beds to take total hospital capacity at 700.

Imo, this is a very favorable upside trigger for the ARPOBs and for overall ROCEs.

Greater Noida hospital also registers a 10% ARPOB increase (possibly driven by transplants?). Despite lower footfalls, the overall revenue of the hospital is up by nearly 20%. This indicates the growing mix of higher specialities. Occupancy levels remain at around 70% and the company is undergoing another brownfield expansion of 200 beds.

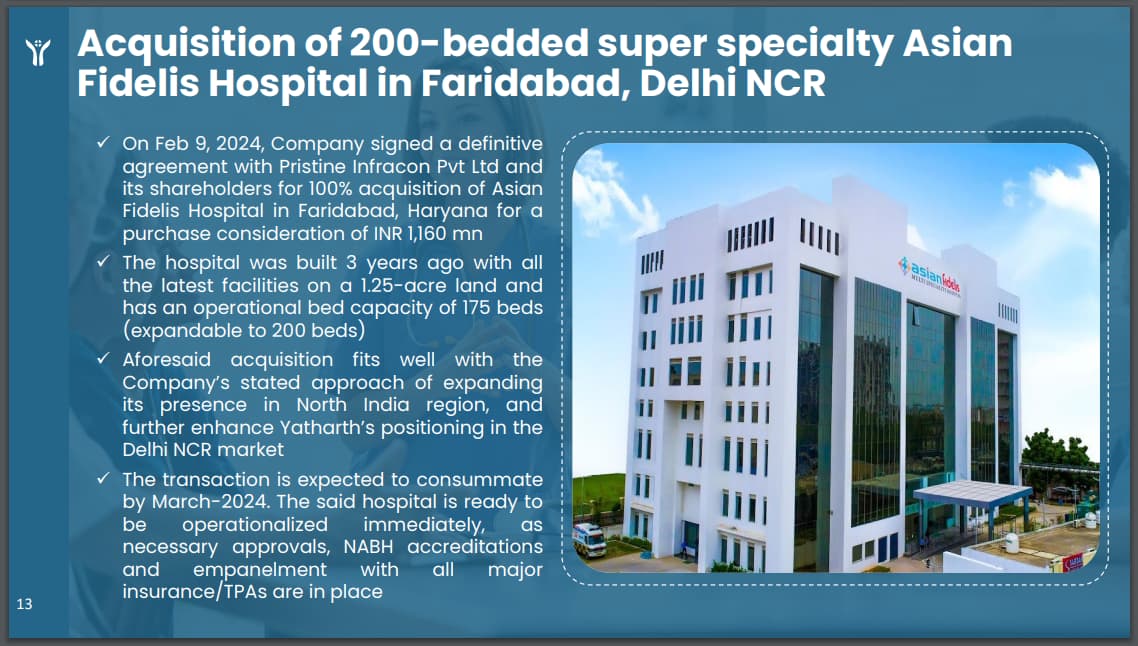

Acquisition of Asian Fidelis for 116crs cash. Sector-88 is a fairly populated area in Faridabad and with upcoming infra (connectivity from Jewar Airport in next 1-2 years), Faridabad will naturally have higher residence density. Needs to be seen how Yatharth can scale the metrics in this hospital. Prima facie, the acquisition looks fairly cheap.

Zooming out, Yatharth is adding nearly 250+200+175 = 625 beds, taking total bed capacity to >2k in next 1-2 years. This is a near 40% capacity addition.

However, the peers in NCR region trade at much higher valuation. Part of the higher valuation is justified because Apollo, Max, Medanta, Fortis all are well recognised and much older brands with greater surgical prowess.

Hard to estimate the EBITDA growth for next year, but conservatively I expect EBITDA to register 40% increase primarily due to:-

a) Contribution from Asian Fidelis (around 20crs total).

b) Higher ARPOBs across hospital (barring Noida). I expect ARPOBs to inch up by 10-15%

FY25E EBITDA: 252

Expected net cash surplus: ~ 300 crs

Basis the above, Yatharth is currently trading at ~14x FY25E EV/EBITDA.

D – Invested (from lower levels) & biased

Yatharth Hospitals posted its results yesterday:-

Can someone help explain to me if Q3 has any sort of seasonality? I don’t see a reason for QoQ degrowth otherwise.

Anyways, posting few of my observations:-

To build on this further, the Noida extension occupancy is currently at 45% and the company is undergoing a brownfield expansion to add 250 beds to take total hospital capacity at 700.

I fully expect the hospital to reach around 40k ARPOBs by end of next year, which puts it not too behind the bigger hospitals.

Imo, this is a very favorable news for Yatharth from a brand and capability point of view.

Greater Noida hospital also registers a 10% ARPOB increase (possibly driven by transplants?). Despite lower footfalls, the overall revenue of the hospital is up by nearly 20%. This indicates the growing mix of higher specialities. Occupancy levels remain at around 70% and the company is undergoing another brownfield expansion of 200 beds.

Acquisition of Asian Fidelis for 116crs cash. Sector-88 is a fairly populated area in Faridabad and with upcoming infra (connectivity from Jewar Airport in next 1-2 years), Faridabad will naturally have higher residence density. Needs to be seen how Yatharth can scale the metrics in this hospital. Prima facie, the acquisition looks fairly cheap.

Zooming out, Yatharth is adding nearly 250+200+175 = 625 beds, taking total bed capacity to >2k in next 1-2 years. This is a near 40% capacity addition.

However, the peers in NCR region trade at much higher valuation. Part of the higher valuation is justified because Apollo, Max, Medanta, Fortis all are well recognised and much older brands with greater surgical prowess.

Hard to estimate the EBITDA growth for next year, but conservatively I expect EBITDA to register 40% increase primarily due to:-

a) Contribution from Asian Fidelis (around 20crs total).

b) Higher ARPOBs across hospital (barring Noida). I expect ARPOBs to inch up by 10-15%

FY25E EBITDA: 252

Expected net cash surplus: ~ 300 crs

Basis the above, Yatharth is currently trading at ~14x FY25E EV/EBITDA.

D – Invested (from lower levels) & biased

I am not so experienced in the ways of the market, and definitely not in leveraging.

“But if the market falls, valuations go down, there will be a lot of opportunities valuation-wise, “

I think it is not necessary that while the valuations go down,when the market falls the intrinsic value of a stock also goes down. My entire purchase philosophy is based on the Ben Graham’s loony Mr Market concept.

Forgive me if I appear to be talking down, but just to put my theory on record, the whimsical Mr Market may offer you a stock worth ₹100 to you in ₹50, and in a bearish mood, you may get that for ₹30. Real money in the recent history was made in 2020, when in the corona wave even the mighty collapsed. My Bajaj Finance which was at ₹4000+ just before the panic, collapsed to ₹2000. And taken in by ‘experts’ at a channel, I sold them off. That was indeed the time to buy more.

In fact, I had bought IDFC First Bank for about ₹20 then. But didn’t hold it due to lack of confidence. But my bets on TCS, Tata Consumer etc paid off because not only I was getting them cheap, they would continue to be in demand from the consumers.

In fact, I entered the PSUs and Titagarh/Texmaco because of the momentum, but became wary when their valuations touched sky-high. I have got out of the major momentum stocks recently, read the PSU, and Railway, and Power stocks in general, because I was not confident about their high valuations.

Remember, the very raison de tre of the PSU craze was the market ingnoring them?

I have reinvested the money I got from selling these, but imagine SJVN which I sold for ₹146, going down to ₹100? Impossible? But then it went from ₹40 to ₹146?

RVNL was also ₹60 or so a year back. Now, it is ₹280. If I get it for even ₹200, I am assured when buying it on leveraged money.

There are you know many stocks which make knowlegeable people anxious. IRFC’s flight from ₹28 to ₹160, while great for the investors, defies logic.

I agree with you that when a stock goes down from ₹100 to ₹60, you worry it will never regain the heights. And of course, the bear-market may last for two years.

So, it is which you approach the market, momentum or value investor.

Keep us abreast of how it goes.

Invest in stock derivatives instead of the stock, works only if it has derivatives.

Quarter on Quarter should have been better if the current price is to be justified. At growth rate of 10% annual EPS will be at best 12 implying a price of 120 to 150.

They had invested 50cr in the new plant and the current plants are itself 60% utilised. the story seems to be have been lost… huge opportunity lost.

even egypt and hungary projects not taking off. USA performance has been mediocre for many years.

Concall is a waste of time… for both investors and the management !!