Hey folks,

Does anyone have either a non paywalled version or a summary/note on this article?

Hey folks,

Does anyone have either a non paywalled version or a summary/note on this article?

Summary of the key points from the Pondy Oxides and Chemicals Ltd. (PCL) Q2 FY2024-25 Earnings Conference Call:

●

Financial Highlights: PCL reported strong financial performance for Q2 FY2025, with consolidated revenue from operations increasing by 42% year-on-year and 30% quarter-on-quarter. Consolidated EBITDA increased by 75% year-on-year, with EBITDA margins at 5.2%, up from 4.2% in H1 FY24. Consolidated PAT increased by 188% year-on-year, with PAT margins exceeding 3% for the same period. The strong performance was attributed to increased production, sales, and realizations in lead, plastics, and copper.

●

Operational Highlights: Capacity utilization of lead, plastics, and copper increased substantially. Lead division sales increased by 47% year-on-year on a half-yearly basis and 49% year-on-year on a quarterly basis. The sales mix between domestic and export markets remained at 32% and 68%, respectively. The percentage of value-added products in the lead segment remained consistent at about 60%.

●

Project Updates: Construction of PCL’s new plant at Tuticorin is ongoing and is expected to be completed for trials by the end of the calendar year 2024, with production commencing from Q4 FY2025. PCL is also increasing capacities in its lead vertical from 132,000 metric tons per annum to 240,000 metric tons per annum in two phases of 36,000 metric tons each. The company’s existing equity shares have been subdivided from one equity share of INR 10 face value into two equity shares of INR 5 face value. The board approved raising funds of up to INR 250 crore through a qualified institutional placement to be utilized for long-term growth and expansion of existing and new verticals.

●

Recycling Industry Trends: The projected growth of the recycled lead market is being driven by demand from the automotive, construction, and renewable energy sectors. The demand for electric vehicles, which use lead-acid batteries for ignition and other ancillary applications, is anticipated to further propel demand for batteries.

●

Government Regulations: Amendments to the battery waste management rules highlight the government’s shift towards stricter accountability for battery producers, ensuring they take responsibility for the entire life cycle of their products. This regulation may also lead to increased consumer awareness about battery disposal, encouraging responsible consumption and recycling practices.

●

Outlook: PCL’s outlook is positive, influenced by strategic capacity expansion, enhanced operational efficiencies, a well-planned capital expenditure strategy, and effective management practices.

Q&A session summary:

●

Volume Increase: The increase in sales volume was primarily driven by the lead vertical, which is backed up by the company’s expansion plans to meet potential future demand. PCL also attributed the increase to the addition of new customers and penetration into new markets.

●

Performance of Aluminum and Plastics Segments: The aluminum segment is being revamped to focus on value-added products. The plastics segment has seen a turnaround from the previous year. While PCL has not been able to utilize its plastics capacity as anticipated, the company expects a turnaround in the third or fourth quarter of this fiscal year.

●

Working Capital Increase: The sharp increase in working capital and negative operating cash flow post-working capital were attributed to the jump in turnover. The utilization of working capital increased, though the average utilization period decreased slightly.

●

Lead EBITDA Per Ton Increase: The increase in lead EBITDA per ton was attributed to the value-added products segment.

●

Hedging Raw Material Volatility: PCL hedges its raw material price risk through forward contracts and by maintaining soft commitments from larger suppliers for a specific amount of raw materials on a monthly basis. The company also has medium-term contracts (3 to 6 months) in terms of volume and supply.

●

Capacity Utilization and Expansion: PCL expects its new capacity of 36,000 metric tons (first phase) to be fully operational by Q4 FY2026. The second phase, adding another 36,000 metric tons, is expected to be operational by Q2 FY2027. PCL is targeting a capacity utilization of 80-90% by Q1 or Q2 of calendar year 2026.

●

Carbon Certificates: While PCL is eligible for carbon credits, the process is not currently active. The company plans to begin voluntarily reporting on environmental, social, and governance (ESG) factors to enhance its value proposition.

●

New Verticals: PCL is exploring new verticals in rubber and e-waste recycling, conducting techno-commercial evaluations to assess the value chain proposition. While the company is also evaluating lithium-ion battery recycling, it is not yet commercially viable due to the early stage of the lithium-ion battery market.

●

Impact of Government Regulations: The company believes that government initiatives and regulations, such as the Battery Waste Management Rules and Extended Producer Responsibility (EPR), will benefit PCL by making the domestic supply chain more transparent and organized, ultimately increasing domestic raw material sourcing.

●

Value-Added Products: PCL defines value-added products as those that are customized for specific applications and offer higher margins than pure lead. The company aims to increase the percentage of value-added products in its portfolio to 70% by FY2026.

●

Raw Material Procurement Mix: PCL’s raw material procurement was previously heavily reliant on imports. However, the company is seeing an increase in domestic sourcing and expects the mix to shift towards 65-70% imports and 30% domestic by next year.

●

Sales to Indian OEMs: Sales to Indian OEMs were approximately 36-38% in the first half of FY2025.

●

R&D Facilities: PCL plans to establish a dedicated R&D center in the next financial year to explore newer verticals and more futuristic materials beyond the basic recycling of non-ferrous metals.

●

Mundra Land Acquisition: PCL intends to start work on its 123-acre land parcel in Mundra by December 2026. The land will be used for future expansions in various segments, including lead and other verticals.

●

Market Share in the Lead Market: PCL estimates its market share in the organized lead market to be around 10-12% of India’s current secondary lead production.

●

Revenue Mix by Segment: PCL aims to diversify its revenue stream, reducing the share of the lead vertical to 65-70% by FY2027 and further to 50% in the next 3-4 years, with the balance coming from other verticals like copper, aluminum, and plastics.

●

Turnaround in Aluminum and Plastics Segment: PCL is working on turning around its aluminum segment by focusing on more profitable products but did not provide a definite timeline. The company expects a turnaround in the plastics segment in the next couple of quarters.

●

Competition from In-house Recycling: While in-house recycling is becoming more prominent in India, PCL does not view it as a threat to its business and believes companies will continue to outsource recycling.

●

Expansion into Steel Recycling: PCL has no plans to enter steel recycling, maintaining its focus on non-ferrous metals.

Overall, the latest quarter results show a mixed picture. While topline growth remains strong, driven by acquisitions and international business performance, profitability has weakened due to margin contraction in the India business.

Related article on anti drone systems being developed world wide.

(post deleted by author)

Hi, My father found physical share certificate of SBBJ bank shares (now SBI Bank), anyone please guide me what is the process for converting physical share into demat account.?

Thanks in advance.

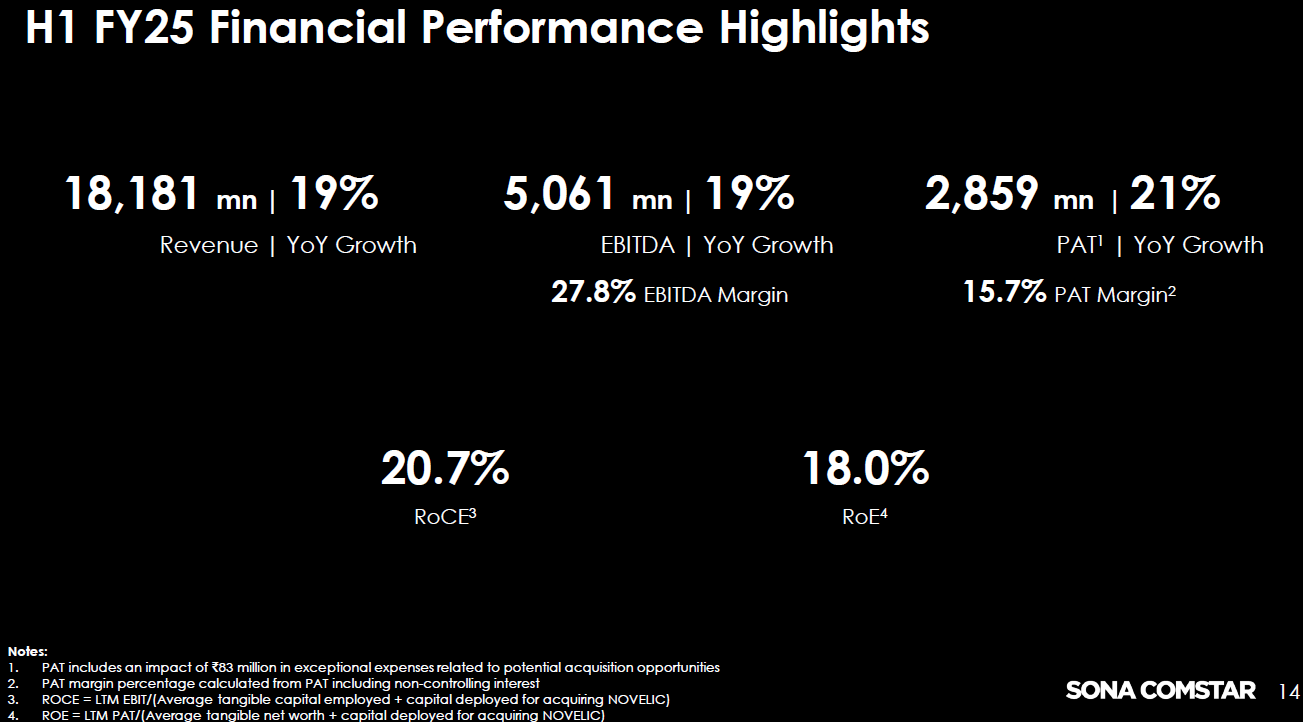

SonaCom posted fair set of numbers in Q2 FY25. Key takeaways from the numbers.

Other highlights/extracts from Inv. Presentation.

Revenue Growth: Total revenue for Q2 FY25 reached INR 9,251 million, reflecting a significant 17% year-on-year increase. This growth outpaced the overall light vehicle sales trend in Sonacom’s key markets (North America, India, and Europe), which experienced a 2% decline. This suggests that Sonacom is effectively capturing market share and expanding its presence.

BEV Revenue Surge: Notably, Sonacom’s Battery Electric Vehicle (BEV) segment witnessed remarkable growth. BEV revenue in Q2 FY25 reached INR 3,172 million, a substantial 53% increase compared to the same period last year. This highlights Sonacom’s successful strategic focus on the rapidly expanding EV market. The BEV segment now contributes a significant 36% to Sonacom’s total revenue, demonstrating its growing importance to the company’s overall performance.

Profitability: Despite various challenges like the UAW strike, Sonacom managed to maintain stable EBITDA margins. The adjusted EBITDA margin for Q2 FY25 was 28.5%, slightly higher than the 28.3% recorded in Q2 FY24. This consistent profitability underscores Sonacom’s operational efficiency and ability to manage costs effectively, even amid a dynamic market environment.

PAT Margin: Sonacom’s adjusted PAT margin for Q2 FY25 was 17.1% compared to 16.3% in Q2 FY24. This growth in PAT margin indicates the company’s ability to translate its topline growth into even stronger bottom-line performance.

New Programs and Customers: Sonacom has secured new programs across various regions in Q2 FY25, demonstrating its continued success in acquiring new business. The company added 1 new program in Europe, 1 in Asia, and 14 in India, further expanding its global reach.

Key Takeaways about Sonacom’s Railway Equipment Division (RED)

Market Leader and Pioneer: RED is the market leader in railway brake systems in India. It introduced manufacturing compressed air brake systems for railway applications for the first time in India, making it a pioneer in the industry.

Diversified Portfolio: RED possesses a diversified portfolio of products, with brake systems being the largest segment. Other products include couplers, suspension systems, electrical panels, HVAC systems, automatic plug door systems, friction and rubber products, and brake cylinders.

Historical Growth and Profitability: RED boasts an attractive financial track record characterized by high growth, profitability, and return metrics. Its revenue grew consistently from FY21 to Q1FY25, with EBIT margins ranging from 13.8% to 20.5% and ROCE exceeding 38% in recent years.

High Growth Potential: RED is poised for high growth, driven by the introduction of new products and the overall expansion of the railway sector. The division is strategically positioned to capitalize on the increasing demand for railway equipment in India and potentially other regions.

Summary

Q2 FY25 performance underscores its resilience and strategic positioning within the evolving automotive landscape. The company’s focus on high-growth segments like BEVs, coupled with its operational excellence, positions it well for continued success.

Disclaimer: Invested and Biased. Less than 7% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

Absolutely. Hopefully things should fall into place ![]() I’ve held a bias but looking at the recent thread will have relook

I’ve held a bias but looking at the recent thread will have relook ![]()