Hey Rohit.

Any source for this. Thanks ![]()

Posts tagged Value Pickr

Burger King ~ Whopper of an Opportunity (03-02-2024)

Neuland Laboratories Limited – Transformation towards niche APIs? (03-02-2024)

Management may provide some clarity on revenue potential of KARXT drug in concal. Karxt drug is just a feather in the cap and since it is claimed to be a block buster drug, there will be lot of recognition for Neuland in Big pharma and Company may get lot of new deals. Over a period of 2 to 3 years we may see significant increase in number project molecules in which Neuland will be working. As discussed earlier in this forum, the nature of business is lumpy, however ever year the base will increase as evident from last several years.

Disclosure : Invested and adding in SIP.

Deepak Fertilizers and Petrochemicals (03-02-2024)

Management itself admitted that high margins in previous year were an aberration. Its a pure commodity play and accordinlgy valuations will also adjust accordinlgy.

EPS will be in the range of Rs 5 per quarter (i.e annualised EPS of Rs 20 ) for next 6 to 8 quarters. Now it is upto individuals what PE they can give for a commodity player.

Even if we give a PE of 15 to 20, there is a long head room for correction in valuation.

Further there is an over hang of 2 major CAPEX undertaken by the Company of around Rs 4000 to Es 4500 Cr (TAN & Nitric Acid)

Fertiliser business is making losses, overall margins are squeezing, Ammonia Capex of Rs 4500 Cr is making losses and Gas for Ammonia plant has been contracted at a higher price.

Disclosure: Exited position and now tracking for knowledge purpose.

Strides Pharma Science (03-02-2024)

Detailed investor presentation by the company. Provides more specifics around. Strides and OneSoruce revenue and EBITA targets in next 3-5 years. Overall market opportunities.

Disc – Invested

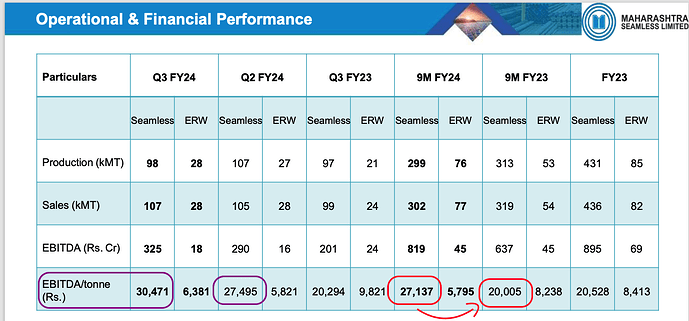

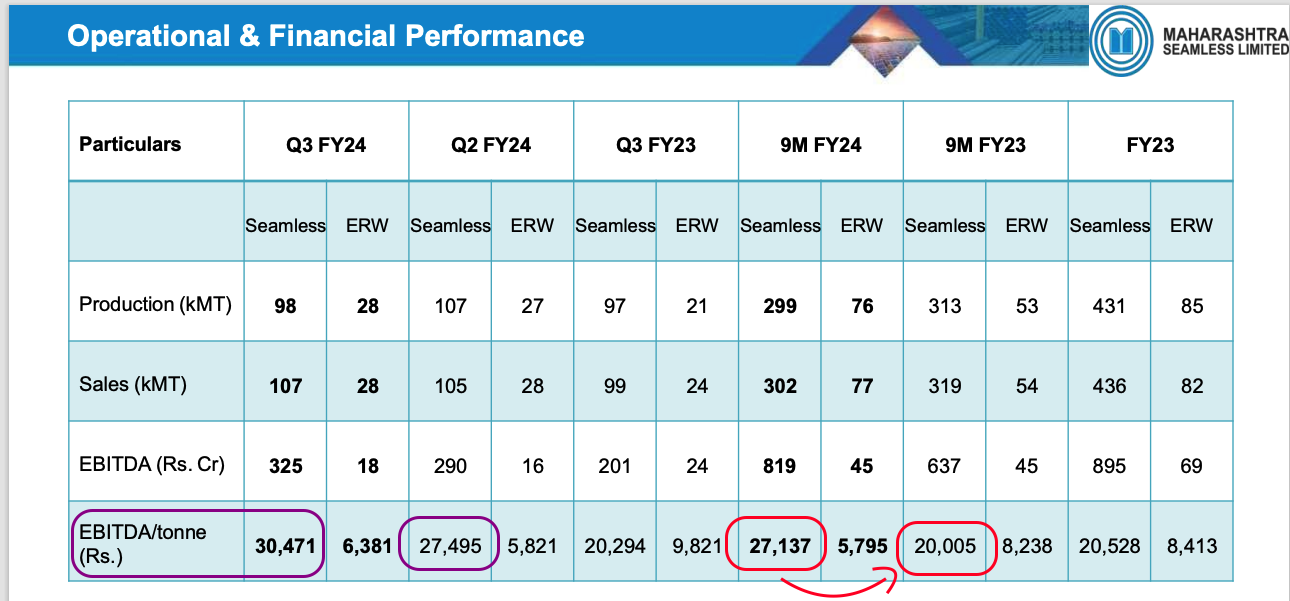

Maharashtra seamless-a value plus cyclical play (03-02-2024)

My takeaways from the conf call ( any mistakes are truly mine, as they were my running notes ):

- Highest EBITDA ( but on lower production volumes). Have been able to control costs.

- There is spending in O&G sector, and orders are getting topped up.

- Seamless pipe product down by approx 10% to 98 kMT from 107 QoQ but sales have been higher, indicating higher price for seamless pipes. Ebitda/tonne has also increases Q, Y and 9m YoY too.

- Domestic demand is high. Exports is only 10% and has not picked up over last 9 months, domestic has compensated. If we wanted to get export order, we could have gotten it by reducing the prices/margins, but we had more than enough domestic orders and hence export is lower.

- Promoter stake has increased over the past 2 years from 63 to 68, when will it improve to 75? No timeline, but would like to get to 75%

- Order book: 1563 cr.

- Orders are typically 3-4 months only

- why is there an increase in EBITDA/Tonne:

- Good domestic market. Export started declining from April of last year, and our margins started increasing from the same time. This indicates the domestic market is good and is indicative of higher margins.

- RM prices have declined. Steel price has come down. When the tender from ONGC came 3 months back and we book RM at a lower price. Not all or 100% of RM is booked, hence lower steel [RM] prices have helped in this quarter.

- FY25 the EBITDA/tonne will go back to 20,000 and will not sustain at 30,000 level. FY24 might close closer to 27,000 levels but FY25 will be lower. [ this year was more opportunistic – volatile market, higher prices for end product and RM was lower ]

- No plans for deploying cash back to shareholders. No opportunities seen yet for buying other companies, we are ‘hoping’ for an opportunity. Dividends plan will be in consideration.

- ONGC comes out with lower value and lower duration order, compared to in the past when it was a large one and for a full year out, unlike today where its for 3-4 months.

- We are one of 3 participants and are the market leader, we will get good orders.

- Exposure to oil and gas segment is 70% other area we cater too are: boiler and general engineering. Power sector uses boiler segment.

- ERW margins are going down. Two types of sectors for ERW we cater to: Oil and water. Depending on the sector, the margins fluctuate. Oil ERW has better margins than water ERW.

In my view, given that the margins are at an elevated level and the mgmt has stated that the EBITDA might not sustain at these levels of 30k and might revert to 20k levels in the next financial year, I have sold most of my holdings. Have transactions in the past 30 days.

AGI Greenpac- on the cusp of growth? (03-02-2024)

Date moved to 9 Feb. Taarik pe Taarik!

Skipper Ltd., (Power and Water) a moat in making? (03-02-2024)

Here is what the mail from ZERODHA says

Blockquote

These RE’s will be temporarily traded on the stock exchanges and will then be extinguished. You can either use the RE’s to apply for the rights shares of the company or you can sell them in the market.

So basically if you are applying then please do not execute any sale transaction. Hope that adds little more clarity.

P.E. Analytics Ltd (PROPEQUITY) – Another Data Analytics Platform for Real Estate Players (02-02-2024)

I feel their current size is very small compared to the opportunities out there. An example is their valuation services business, where conservatively the TAM is 300-500 cr. annually, and they are only at 15-20 cr. revenues. Their main competitors are individual valuers who might not give the same level of standardization and turn around times. I imagine this vertical can easily reach 80-100 cr. in next 5 years.

Another way I have been looking at their business setup, is that their main customers are financial institutions and they are looking to build multiple service lines to increase their product offerings (e.g. valuation services, project construction monitoring, project prices, etc.). This is simply customer mining and a relatively low hanging fruit.

They have also been talking about building a B2C line of business, the details of which was hazy in the past. In this presentation, they have clearly highlighted their plans of going into asset light model of development management, and building a social media reach to generate potential leads.

So there are lots of opportunities and it will boil down to their execution skill. Samir is a veteran in this industry and has all the relevant contacts. Maybe @Deenar_Toraskar , @Chins or @nirvana_laha can add more as they have done significant amount of work on this industry. My notes from their presentation is below.

02.02.2024 presentation

-

Annual subscription fee is based on the vertical & #cities subscribed by a client. Fees is higher for Tier 1 cities vs Tier 2 cities

-

Construction finance reporting: 21 reports were processed in a single month in FY24 vs 5/month in FY23 (see image below)

-

-

Developer Management: In JV with Forbes Global properties (2 models shown below)

-

-

PropMonitor: Monitors under construction projects for banks and gives reports to them for release of construction finance payments

-

PropBuild: New B2B construction portal

-

Will double valuation business revenues in FY24 (8.7 cr. in FY24)

-

Clients increased to 205 (vs 190 in Q2FY24) in website subscription business. Retention ratio is 85%

-

Cash grows to 71 cr. in FY24Q3 (vs 65 cr. in FY24Q2)

-

SamirJasuja-PropEquity: Youtube channel for lead generation for projects (aims to reach 1mn+ followers)

Disclosure: Invested (position size here, no transactions in last-30 days)

Amara Raja Energy & Mobility Limited: Powering Ahead (02-02-2024)

Amara came out with decent results with sales and EPS growing by 15%. It seems that their new energy business benefitted from lower lithium cell prices. This also brings into question future of lithium battery business, at a scale of 7-9 GWh, they expect to make 10-11% EBITDA margin at current cell prices of $80/GWh. They even went on to say that given the Chinese overcapacity, EV penetration has to reach 50% for the business to be lucrative. And market is most excited about this division! Concall notes below

FY24Q3

-

Lead acid battery : 13% YOY growth

-

4-W volumes : OEM: 2%, after-market: 11%

-

2-W volumes : OEM: 30%, after-market: 15%

-

Industrial volumes : growth of 6-7% (telecom: 8-9%, UPS: __%)

-

Home inverter volumes : no growth (only doing trading currently)

-

Exports : 24% YOY growth (4-W AGM batteries: 25% volume growth). Revenues are recognized after delivery. Catering to large retail chains

-

RM pricing : 200/kg (have not taken any price hike)

-

Trading revenue of 7%

-

50% of volume is from after market

-

-

New energy business :

-

148 cr. (vs 150 cr. in Q2 and 68 cr. in Q3FY23). 80% battery packs of 2-W and 3-W (Mahindra and Piaggio are main customers with 2-W being small)

-

Successfully powered an E-Bike using in-house NMC based 2170 cylindrical cells

-

Have started supplying battery pack for telecom (BSNL) and for industrial applications

-

Small cell towers have seen adoption of lithium packs

-

-

Tubular battery plant will be ready in March 2025

-

Plastic component acquisition from Mangal Industries is now complete, effective date will be 01.02.2024

-

Lithium cell : currently estimate 10-11% EBITDA margin (at current lithium prices) with 10-11% ROE at 7-9 GWh scale (@$80-90/GWh)

-

Given the Chinese overcapacity, EV penetration will have to reach 50% for business to be lucrative

-

FY24 capex: 250 cr. (lead) + 250-300 cr. (lead recycling + new energy). Recycling plant will commence in Q1FY25

-

FY25 capex: 600 cr. (mostly around new energy)

Disclosure: Invested (position size here, no transactions in last-30 days)

UPL Ltd – global agrochemical company (02-02-2024)

I think we can wait. As per management presentation expecting recovery from Q2FY25