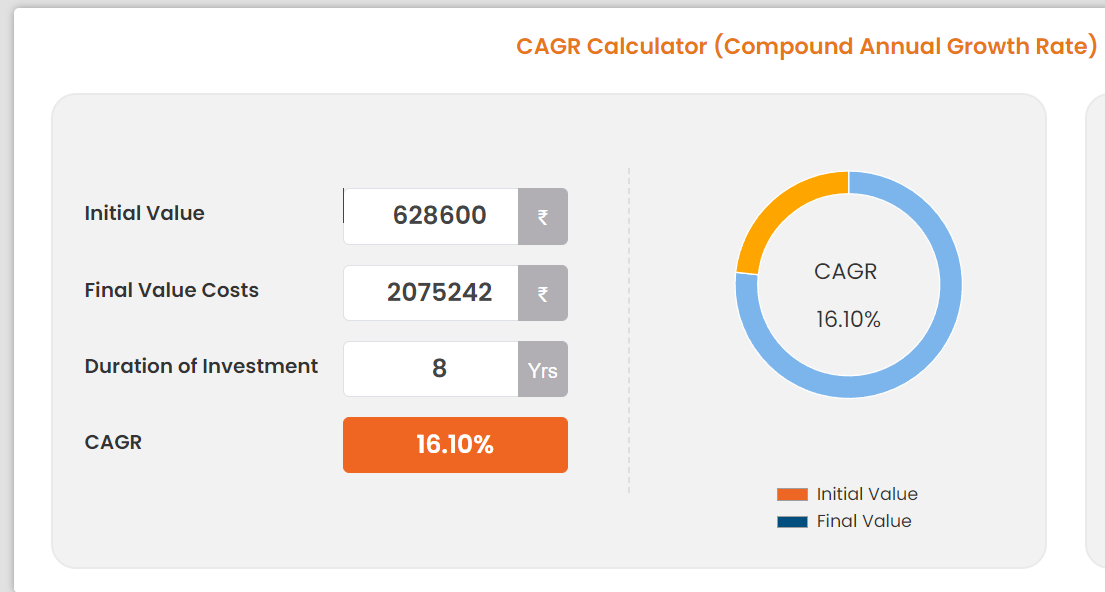

90% of large cap mutual funds doesn’t beat index in India. For a new person who just bought stocks based on tips of experts, I still see 16% as decent return.

Posts tagged Value Pickr

Help on my Portfolio (30-01-2024)

(post deleted by author)

Rain Industries – An oversold de-leveraging play (30-01-2024)

Any specific reason that shook your thesis for the company? or what made you to book that profits, curious to know as you seem to be a hardcore “Rain industries” Investor. Curious to know your thoughts going forward

Rain Industries – An oversold de-leveraging play (30-01-2024)

Seems like they are trying to caution the investors (who have high expectations after peer companies results) to keep the rational expectations that is just after recent surge in stock prices also, one more thing I feel like is there are lot more headwinds and for a prolonged period than one is expecting at this moment, this might be the reason why Pabrai has sold his stakes.

Disc: recently added between 150-160 levels

Help on my Portfolio (30-01-2024)

Great work.

16% CAGR on such a high risk portfolio is very average return (adjusted for high risk premium associated with small/microcaps). Nifty small caps index has given 18% CAGR in 8 years and many large cap mutual funds (with much lower risk premium) have also given returns in the same range.

To generate alpha of 3-5% over a representative index (in this Nifty Small Caps), the target return will be 21-23% which is quite challenging and requires active management of portfolio. If one is not up to it better to go with good small caps mutual funds.

MPS Ltd (30-01-2024)

@ap1990

MPS Q3 numbers were clearly disappointing, more so as the mgt. had needlessly upped the guidance just a qtr ago. The numbers themselves were not that bad, with operating margins getting better despite the set back in the e-learning business. I guess the mgt too has learned its lessons & will hopefully, going forward, let their numbers do the talking! I guess the the pressure of having concalls after every quarterly numbers also gets to the mgt whose enthusiasm to please shareholders can sometimes get the better of their judgement! The mgt. though has stayed committed to their vision 2027 of 1500 crs, & hope to actually achieve it before time with similar margins.

I am of the view that the mgt. is well meaning & have by & large walked the talk over the last 7-8 qtrs, which is a sufficiently long time. I also believe the the mgt. has the wherewithal & ability to grow inorganically by successfully acquiring companies & then integrating them. That is what will create shareholder value in the long run. It matters less that the vision 2027 is realised 2-3 quarters behind schedule but the journey forward should clearly show a pattern in that direction.

The Co. is generating free cash flows of about 130-150 crs annually. Has given a interim dividend of Rs. 30/-, & could easily give another similar final dividend (I think the mgt has mentioned something to this effect in the previous concall, admittedly to be taken with a pinch of salt!) That would make the stock give about a 4% dividend yield.

I feel any meaningful correction from current levels of about 1490 could present a decent buying opportunity & I will look to add.

Disc: Invested

MPS Ltd (30-01-2024)

Management has done a laudable job of integrating and driving to growth all the businesses bought in last few years. Delay and customer decisions do impact business and has to be taken as known risk. Having an aspirational growth plan is a directional plan. Revenue projections and risk is blended in Management/ Analyst projections and aspirations. Dividend yield and growth has been decent for the current valuation.

Help on my Portfolio (30-01-2024)

Putting everything on the side:

Just for random calculations

I did the current valuation of the PF on the first day and what would happen if it is left untouched.

| Row Labels | Cost Value | CMP value | Profit | % |

|---|---|---|---|---|

| Alpa Lab (66) | 6600 | 10100 | 3500 | 53.03% |

| Anantraj (36) | 3600 | 47300 | 43700 | 1213.89% |

| Arrow Textiles (89) | 8900 | 900 | -8000 | -89.89% |

| Ashiana (150) | 15000 | 31200 | 16200 | 108.00% |

| Ashok leyland (95) | 9500 | 17300 | 7800 | 82.11% |

| Astra microwave (130) | 13000 | 55100 | 42100 | 323.85% |

| Axiscades (250) | 25000 | 80000 | 55000 | 220.00% |

| Balaji Amines (133) | 13300 | 229900 | 216600 | 1628.57% |

| Camlin Fine sciences (95) | 9500 | 12700 | 3200 | 33.68% |

| Cox & Kings (215) | 21500 | 175 | -21325 | -99.19% |

| DLF (98) | 9800 | 78700 | 68900 | 703.06% |

| Elgi equipments (125) | 12500 | 121400 | 108900 | 871.20% |

| FCEL (23) | 2300 | 120 | -2180 | -94.78% |

| Fortis Healthcare (166) | 16600 | 42000 | 25400 | 153.01% |

| Future Retail (162) | 16200 | 315 | -15885 | -98.06% |

| Gabriel India (92) | 9200 | 37000 | 27800 | 302.17% |

| Granules INdia (144) | 14400 | 40900 | 26500 | 184.03% |

| Greaves Cotton (124) | 12400 | 16200 | 3800 | 30.65% |

| Greenply Ind (182) | 18200 | 24600 | 6400 | 35.16% |

| Gufic Bio (Avg 90) | 9000 | 35600 | 26600 | 295.56% |

| HSIL (270) | 27000 | 76200 | 49200 | 182.22% |

| India cements (84) | 8400 | 26000 | 17600 | 209.52% |

| Indiabulls wholesale (15) | 1500 | 1220 | -280 | -18.67% |

| Indian Hotels (105) | 10500 | 49300 | 38800 | 369.52% |

| Jagsonpal Pharma (Avg 85) | 8500 | 37400 | 28900 | 340.00% |

| Jain Irrigation (65) | 6500 | 6530 | 30 | 0.46% |

| Jamna Auto (145) | 14500 | 11700 | -2800 | -19.31% |

| Jindal steel (60) | 6000 | 74600 | 68600 | 1143.33% |

| Jyoti structure (16) | 1600 | 3280 | 1680 | 105.00% |

| Kanoria chemical (70) | 7000 | 13300 | 6300 | 90.00% |

| KPIT Tech (140) | 14000 | 145700 | 131700 | 940.71% |

| KRBL Ltd (215) | 21500 | 36100 | 14600 | 67.91% |

| Kwality (113) | 11300 | 220 | -11080 | -98.05% |

| Marksans Pharma (Avg 90) | 9000 | 14700 | 5700 | 63.33% |

| Maxwell Industries (57) | 5700 | 4600 | -1100 | -19.30% |

| Nectar Lifesciences (55) | 5500 | 3440 | -2060 | -37.45% |

| NIIT (87) | 8700 | 12500 | 3800 | 43.68% |

| Onmobile Global (127) | 12700 | 11300 | -1400 | -11.02% |

| Pipavav Defense (72) | 7200 | 17000 | 9800 | 136.11% |

| RS Software (68) | 6800 | 7200 | 400 | 5.88% |

| Ruchira papers (59) | 5900 | 17050 | 11150 | 188.98% |

| Skipper Ltd (160) | 16000 | 23600 | 7600 | 47.50% |

| Snowman Logistics (90) | 9000 | 6920 | -2080 | -23.11% |

| Sudarshan chemical (95) | 9500 | 52400 | 42900 | 451.58% |

| Syncom Healthcare (16) | 1600 | 420 | -1180 | -73.75% |

| Talbros Auto (104) | 10400 | 27100 | 16700 | 160.58% |

| Talwalker (240) | 24000 | 100 | -23900 | -99.58% |

| Tanla Solutions (41) | 4100 | 100000 | 95900 | 2339.02% |

| Tara Jewels (60) | 6000 | 50 | -5950 | -99.17% |

| Tata Global beverage (142) | 14200 | 112300 | 98100 | 690.85% |

| Tata Motors DVR (257) | 25700 | 85900 | 60200 | 234.24% |

| TCI (240) | 24000 | 84000 | 60000 | 250.00% |

| Trigyn Tech (89) | 8900 | 15800 | 6900 | 77.53% |

| Ujaas energy (26) | 2600 | 225 | -2375 | -91.35% |

| V2 Retail (60) | 6000 | 35400 | 29400 | 490.00% |

| Zen Technologies (88) | 8800 | 80000 | 71200 | 809.09% |

| Zicom Electronics (115) | 11500 | 177 | -11323 | -98.46% |

| Grand Total | 6,28,600.00 | 20,75,242.00 | 14,46,642.00 | 230.14% |

There might be some errors but it is majorly correct.

Days 2916.

Not here to prove any thesis.

Since this thread was inactive for long, just did a calculation.

Pharma || Hospitals || Diagnostics : Industry perspective (30-01-2024)

Cipla Q3 FY 24 –

Concall highlights –

Sales @ 6604 cr, up 14 pc

EBITDA @ 1748, up 24 pc (margins @ 26 vs 24 pc)

PAT @ 1068 vs 808 cr

R&D spends @ 6.1 pc of sales, up 10 pc YoY

Region wise performance –

India sales @ 2859 cr, up 12 pc, fuelled by chronic therapies and big brands ( 44 pc of total sales )

North America sales @ $ 230 million, up 18 pc ( 29 pc of total sales )

South Africa sales @ ZAR 1355 million, up 15 pc

( 1 ZAR = Rs 4.4 )

Other international Mkt sales @ $ 90 million ( 11 pc of total sales )

API and others represent 4 pc of sales

Company’s cash holdings @ 7200 cr ( I hope they r used to acquire speciality, branded portfolios )

Forecort Inhaler – became the No 1 Indian brand in Q3

Filed gSymbicort and one more product in US mkts

Awaiting approval for one peptide product launch

Therapy wise rank of Cipla India –

Respiratory – 01

Urology – 02

Cardiac – 07

Overall rank in India – 03

Rank in chronic therapies – 02

Company has 10 brands in top 100, 06 brands in top 50 and 03 brands in top 25 in IPM. Company has 20 brands with sales > 100 cr/yr

Cipla’s popular Indian OTC brands – Omnigel, Nicotex, Cofsils, Cipladine, Prolyte ORS solution

Acquired Actor Pharma in RSA for $ 49 million in Q3. Integration process is on

Q4 is a seasonally weak Qtr – both in India, US

Company’s Goa plant is scheduled for a re-inspection by USFDA in Q1 FY 24. It was last inspected in Aug 22 and was given a warning letter. Similar is the case with their Pithampur plant which was also given OAI status in Feb 23. OAIs at these 2 plants are hampering the new product launches in US

One Peptide product should get launched by Q1 FY 25. Cipla should be the first company to launch it. Mkt size for the product is descent ( they did not quantify )

Company is hopeful for an approval for the launch of Advair in US by end of FY 25. Current price of the generic Inhaler is around $ 30 / inhaler

Cipla has about 20 pc mkt share for lanreotide 505(b)(2) product in US. Hope to keep gaining incremental Mkt share in the coming Qtrs

Going fwd ( 3-5 yrs ), Respiratory and Peptide assets shall continue to be company’s two largest segments in the US mkt

Cash on books to be used for bolt-on acquisitions. Can go for larger assets in India, relatively smaller assets in Intl Mkts

Disc : holding, biased, not SEBI registered

Ranvir’s Portfolio (30-01-2024)

Cipla Q3 FY 24 –

Concall highlights –

Sales @ 6604 cr, up 14 pc

EBITDA @ 1748, up 24 pc (margins @ 26 vs 24 pc)

PAT @ 1068 vs 808 cr

R&D spends @ 6.1 pc of sales, up 10 pc YoY

Region wise performance –

India sales @ 2859 cr, up 12 pc, fuelled by chronic therapies and big brands ( 44 pc of total sales )

North America sales @ $ 230 million, up 18 pc ( 29 pc of total sales )

South Africa sales @ ZAR 1355 million, up 15 pc

( 1 ZAR = Rs 4.4 )

Other international Mkt sales @ $ 90 million ( 11 pc of total sales )

API and others represent 4 pc of sales

Company’s cash holdings @ 7200 cr ( I hope they r used to acquire speciality, branded portfolios )

Forecort Inhaler – became the No 1 Indian brand in Q3

Filed gSymbicort and one more product in US mkts

Awaiting approval for one peptide product launch

Therapy wise rank of Cipla India –

Respiratory – 01

Urology – 02

Cardiac – 07

Overall rank in India – 03

Rank in chronic therapies – 02

Company has 10 brands in top 100, 06 brands in top 50 and 03 brands in top 25 in IPM. Company has 20 brands with sales > 100 cr/yr

Cipla’s popular Indian OTC brands – Omnigel, Nicotex, Cofsils, Cipladine, Prolyte ORS solution

Acquired Actor Pharma in RSA for $ 49 million in Q3. Integration process is on

Q4 is a seasonally weak Qtr – both in India, US

Company’s Goa plant is scheduled for a re-inspection by USFDA in Q1 FY 24. It was last inspected in Aug 22 and was given a warning letter. Similar is the case with their Pithampur plant which was also given OAI status in Feb 23. OAIs at these 2 plants are hampering the new product launches in US

One Peptide product should get launched by Q1 FY 25. Cipla should be the first company to launch it. Mkt size for the product is descent ( they did not quantify )

Company is hopeful for an approval for the launch of Advair in US by end of FY 25. Current price of the generic Inhaler is around $ 30 / inhaler

Cipla has about 20 pc mkt share for lanreotide 505(b)(2) product in US. Hope to keep gaining incremental Mkt share in the coming Qtrs

Going fwd ( 3-5 yrs ), Respiratory and Peptide assets shall continue to be company’s two largest segments in the US mkt

Cash on books to be used for bolt-on acquisitions. Can go for larger assets in India, relatively smaller assets in Intl Mkts

Disc : holding, biased, not SEBI registered