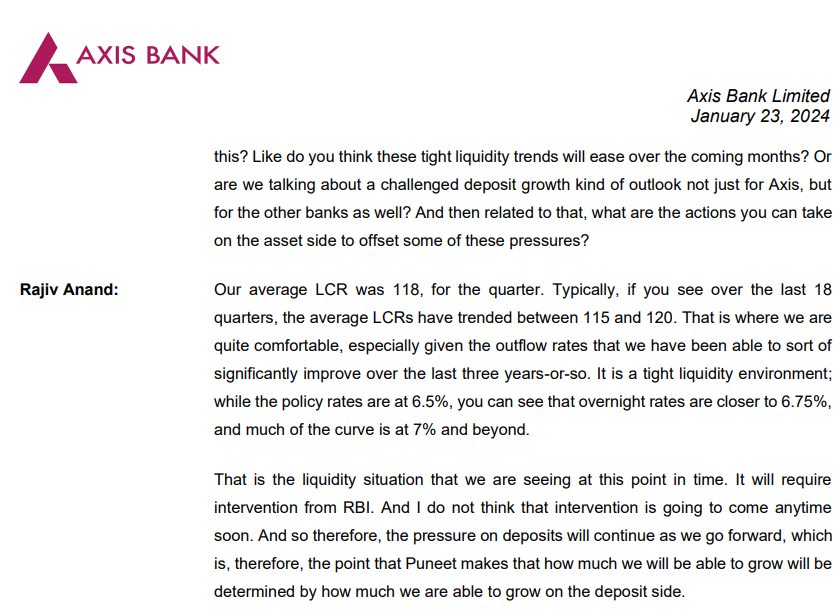

From the recent con-call – Seems like tight liquidity will continue until CY24 H2

From the recent con-call – Seems like tight liquidity will continue until CY24 H2

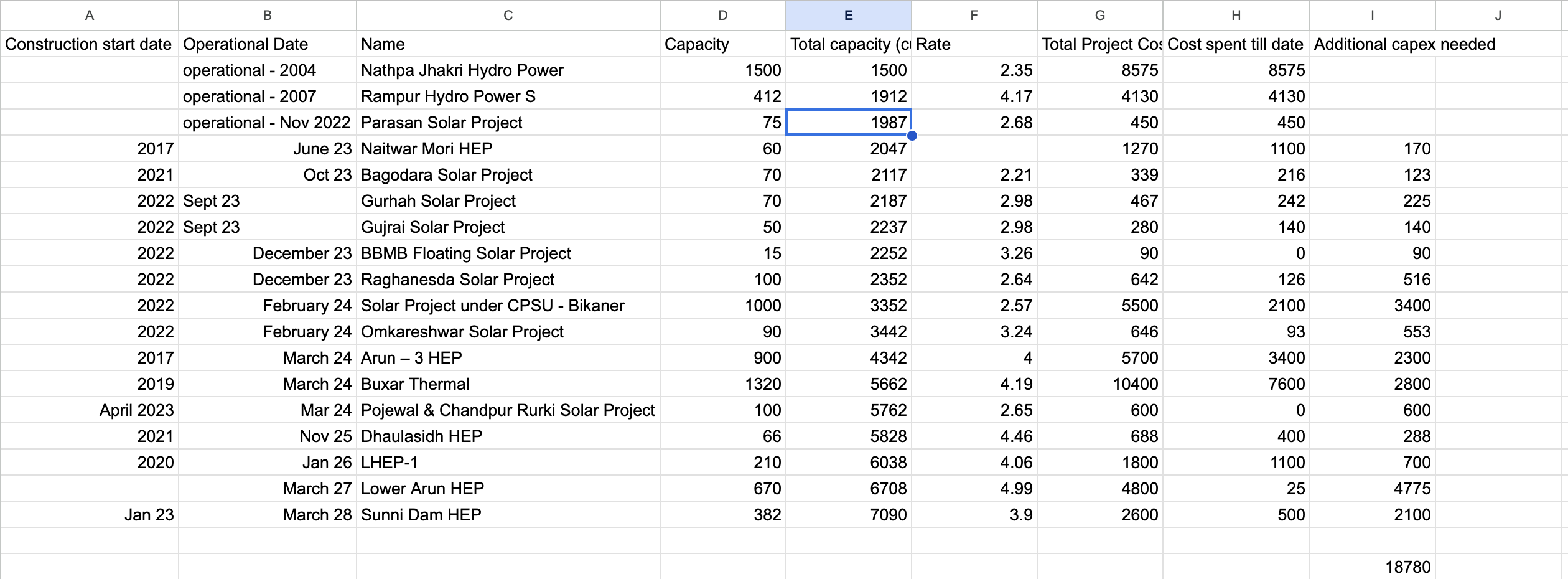

I am very bullish on SJVN, reason being:

They are mostly into renewables now… one of their major Thermal plant is Buxar. Apart from this, I dont think they have any major Thermal.

When I researched on SJVN in June 2023, they had installed capacity of about 2000 MW and had visible pipeline of 7000 MW capacity (image attached for my analysis until June 2023). At that point of time, they had vision to 20x their installed capacity by 2030 or so.

In last 6-8 months, they have got orders of atleast 4000 – 5000 MW, so now projections are at 12000 MW operational capacity by 2026-27.

They aim to increase their installed Capacity to 25 MW by 2030. Which will be more than 12x of their current capacity

SJVN has been designated as Renewal Energy Implementation Agency by Government of India. Through REIA SJVN collects the demand from the states / discoms and then for the renewal

energy, they invite bids from the developers. These developers build RE project, then the

PPOs are signed between these developers and the discoms of the states. And the SJVN will

get INR0.07 paisa per unit for this energy which we would be supplied to these discoms. There are 4 REIA in India at the moment.

All this growth will certainly bring in risks along:

What I am expected – With 12x capacity, revenues are expected to be 10-12x and Net Profits may increase 6-7x due to interest outgo in initial years + REIA opportunity would also bring in 2-2.5K profits over 4-6 years. REIA is a new thing for SJVN, not sure how it will play out.

My average buying price is 66, I am expecting a min of 6x from my invested price by 2030

FEP-ENM or Cefepime/Enmetazobactam to be sold under brand name Exblifep has good efficacy in certain class-A beta-lactamases but overall its performance is comparable to Piperacillin/tazobactam (sold as Zosyn and gone off-patent in ’23) which again is comparable to meropenems. These are not effective in MBL-producing strains is what the studies say.

WCK 5222 or FEP-ZID has efficacy against all classes of ESBL and carbapenamase producers (see FEP-ENM column and compare against FEP-ZID 1:1 column to get an idea). Bold text with or without greater-than signs mean those variants are resistant to the drug in that particular column.

Exblifep will be competing against a generic Zosyn and meropenem and odds of it being priced higher than these are slim since efficacy is equivalent. WCK 5222 is more comparable to CAZ/AVI (Avycaz) or ATM/AVI and is showing in studies that it is even better than those as its mode of operation is completely novel (BLE) compared to anything that currently exists.

If anything the royalty that Orchid can make can give us a good idea of what to expect with WCK 5222 (it has to be few times better than FEP-ENM)

Median PE for 3 or 5 years?

Superb numbers from bluestar

24% YOY quarterly revenue growth

45% YOY Ebitda growth

UCP segment growth – 35% YOY

I think AC as a category is an outlier among other consumer durables and home appliances segment in terms of growth and with now industry coming out of 2-3 years of low growth led by delayed summer/high competitve intensity, AC as a category should be an outlier among other segments

Good insights, thanks. ICRA CRISIL & CARE all ratings are needed. Anyways there is no way this PSU can get less than AA rating.

Also it is good to see contrasting viewpoints from @akash_das and @Anubhav_Garg based on the same fact, this is why I started this thread on VP.

Don’t think of inflation, time or returns, focus on your profession and then on gaining knowledge. A lot of things impact investing, not just time. Capital, risk, returns, market cycles, liquidity, even luck.

If you want to participate, and want to see your investment grow with time, start with a debt fund, not to redeem soon, but invest until you reach a point where you are confident enough to go forward into equity. If there is a chance of withdrawal too, go with a RD. There is a bull run going on, so 12-15% return looks normal, it is not. Liquidity is a major factor in taking the prices up, if that runs out, even 8% will look wonderful, hence no compounding in itself, unless you are doing it yourself.

If you go with equity, you can go with a conservative hybrid fund, which has more debt and some equity, the NAV could fluctuate, you get used it, and you can do this for a year and check your progress and experience.

As time is on your side, you don’t have to hurry.

Skipper has allotted Rights Issue 1:10 ie one Rights Equity for every 10 shares held.

Today that REs have been credited to eligible share holders. RE issue will be at 198/-share. Hence there is a difference of Rs 42/- from todays CMP of skipper. Those who are not interested to apply for RE, have sold their share in open market and are available at Rs 42/-. (ie the difference between Offer price and CMP of skipper).

Those who want apply for Rights Issue, to apply on or before 05 Feb by paying Rs 48.25. you will be issued with Skipper BE share of face Value 0.25 (present FV of skipper share is Rs 1). You may need to pay additional Rs 144.75 as and when asked by the board to convert that share to a normal skipper share of FV of 1 (Up to three additional Calls, with terms and conditions such as the number of Calls and the timing and quantum of each Call as may be decided by the Board/ Rights Issue Committee –from time to time to be completed on or prior to March 2025).

From 05 Feb, REs allotted will expire and wont be avl for trading.

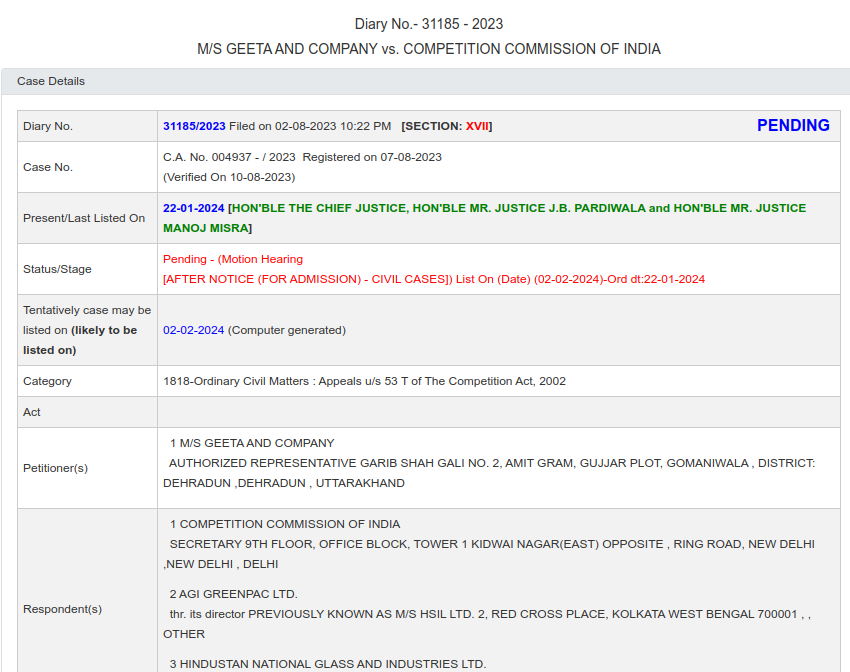

sci case status

Earnings Outlook With Varun Lohchab, Head of Institutional Research, HDFC Securities

Some discussion around battery companies.

Calls it a day in politics and will start to focus on Amara raja as per news