https://e360.yale.edu/digest/wall-street-begins-trading-water-futures-as-a-commodity?s=08

Posts tagged Value Pickr

Varun beverages fast growth duopoly business (22-01-2024)

I have not done any extensive analysis as of now, but one thing I am sure about is, PE expansion for this stock will soon touch its high. Net profit for 2022-23 is approximately 33% higher than last year, but the stock has more than doubled. Such outperformance cannot continue for long. There will either be time correction, which means the stock will consolidate for sometime to match its long term valuation average, which is around 56x EPS, or we can see a price correction which gives us a target price of 962-990 per share.

Disc- Invested

Varun beverages fast growth duopoly business (22-01-2024)

I have not done any extensive analysis as of now, but one thing I am sure about is, PE expansion for this stock will soon touch its high. Net profit for 2022-23 is approximately 33% higher than last year, but the stock has more than doubled. Such outperformance cannot continue for long. There will either be time correction, which means the stock will consolidate for sometime to match its long term valuation average, which is around 56x EPS, or we can see a price correction which gives us a target price of 962-990 per share.

Disc- Invested

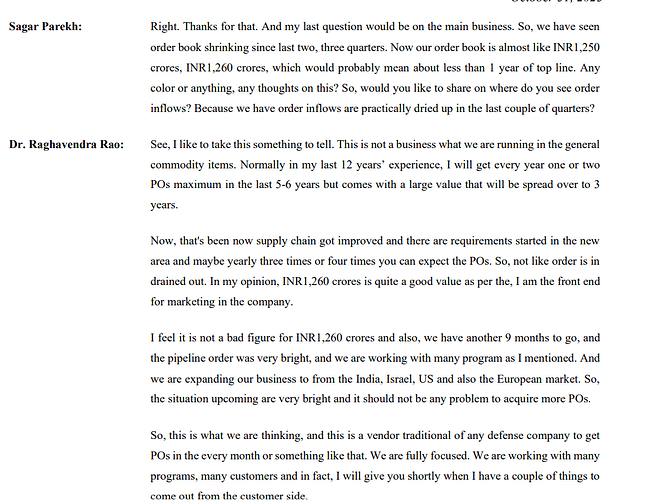

DCX Systems Ltd (22-01-2024)

Nice write up. The few points from my side:

- Still OPM is between 6-7 % due to EMS nature of business. It appears a volume play as of now. In Last Con-Call there was discussion on margin expansion-

Company hopes that once backward integration happens ( Manufacturing PCB by Subsidiary Renal Advanced System) there would be improvement in margin. But, company is not quantifying it.

- Employee cost is very low. Approx. 1% of Sales. In May 29, 2023 Con call the issue was raised by investor as below:

As per management company uses hig value products, so employee requirement is low. But, after going through different con-calls it appears that they are not in highly technical field. They are basically in integration and in assemly and now they have started making high value PCBs which they were integrating.

- There is shrinkage in order book of the company. After Q4 Fy 23 it was Rs 1700 Cr. After Q2 FY 24 it is Rs1260 Cr. Although management is quite confident and some they are expecting orders in some more programs.

Over all it appears a decent play and value migration may also happen, as company delivers result, enters in JVs and acquire technologies.

Disclosure: Not invested

Disclaimer : I may be wrong in my analysis, I am neitehr SEBI registered analyst nor subject expert. Please do your own due dliligence.

IPO Review – Discussion until listing (22-01-2024)

Returns depends upon the amount one has to keep in cash to get the allocation. Retail portion is based on lottery and is not scalable. There is very low chance of allocation as people are applying from multiple accounts also. Once a while one can get lucky but no strategy can be made out of it due lack of scale.

The hni quota is based on the proportion to the amount applied for. So people are applying in higher quantities to get confirmed allocation. One strategy used is to apply in higher quantities and keep rotating with higher quantities to scale.

Another problem is that IPOs work best in bull market. One can easily use the money kept for IPO in secondary market and get better returns.

Strategy of buying on listing date and holding for long term can be used on poor listing with undervaluation. In most cases there is nothing left for investors after listing gain.

IDFC First Bank Limited (22-01-2024)

(post deleted by author)

The harsh portfolio! (22-01-2024)

Hi @harsh.beria93 , would this be a good time to re-evaluate ICICI/IDFC over HDFC Bank?

Results have mostly disappointed since some time.

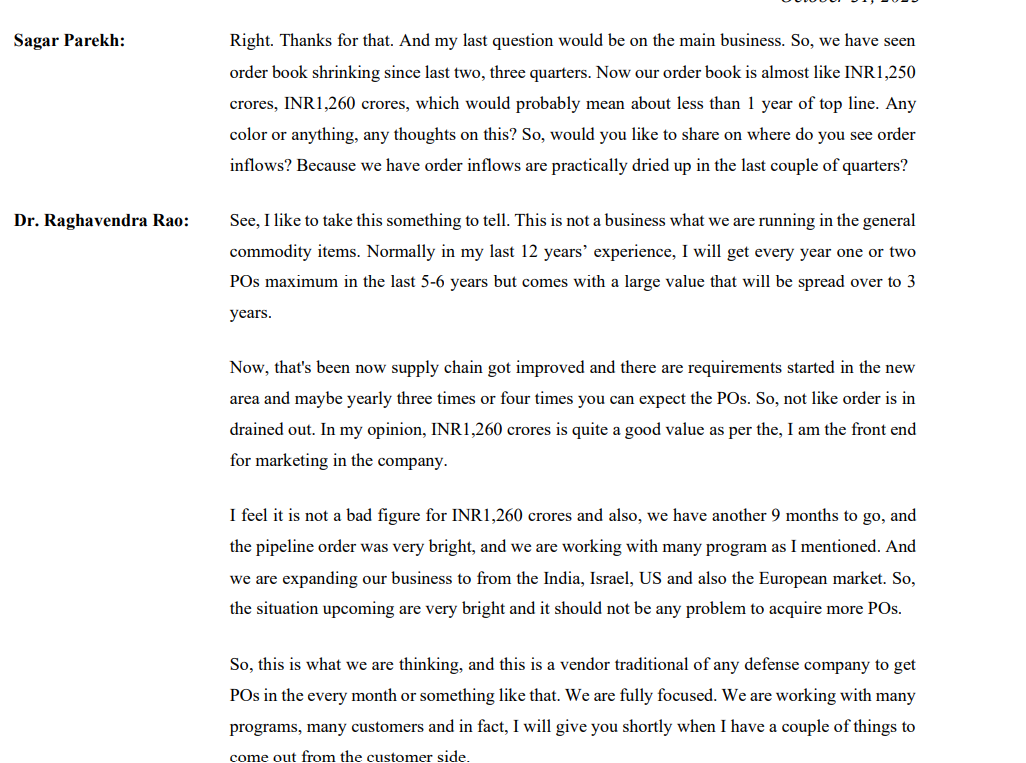

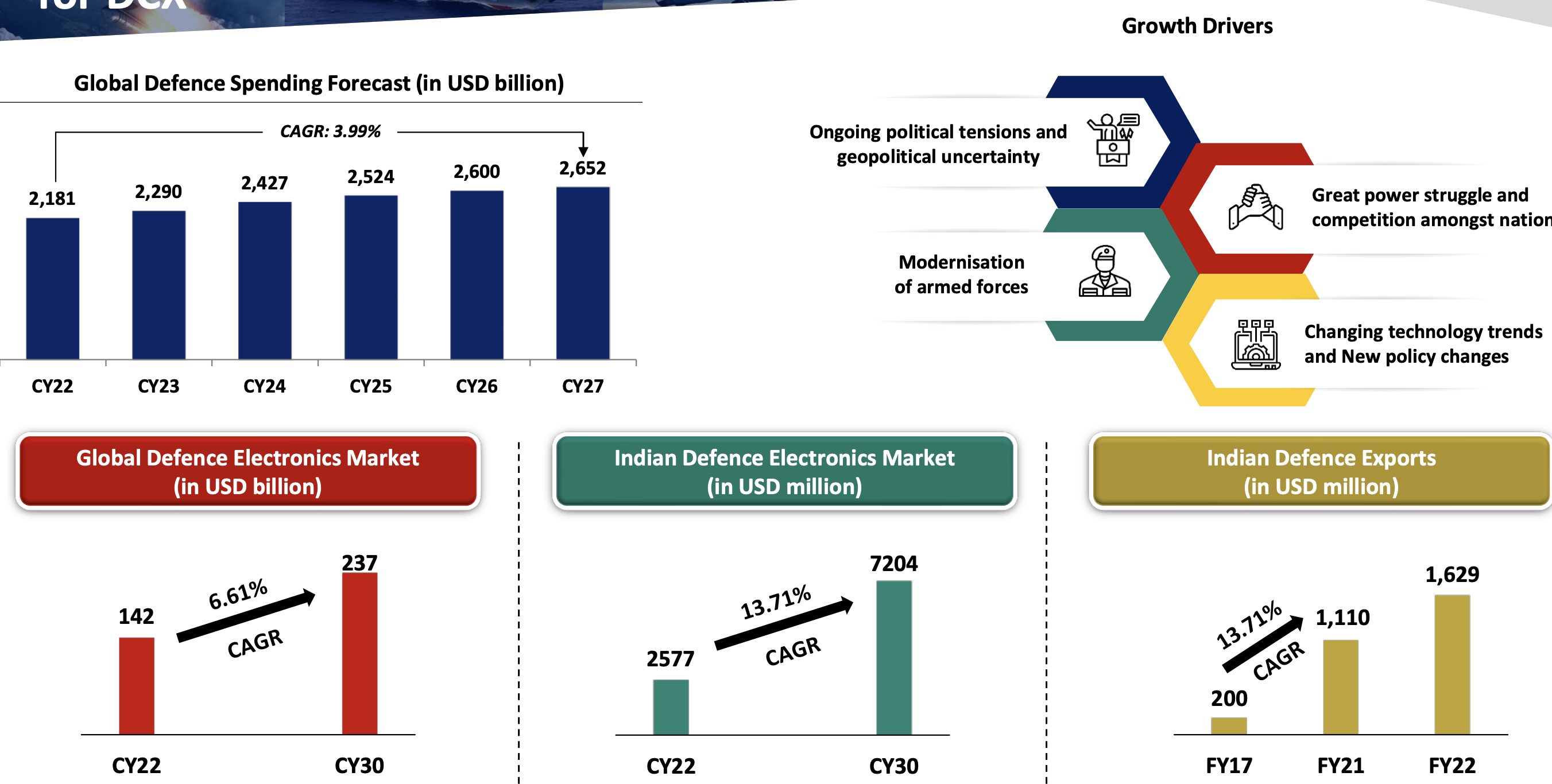

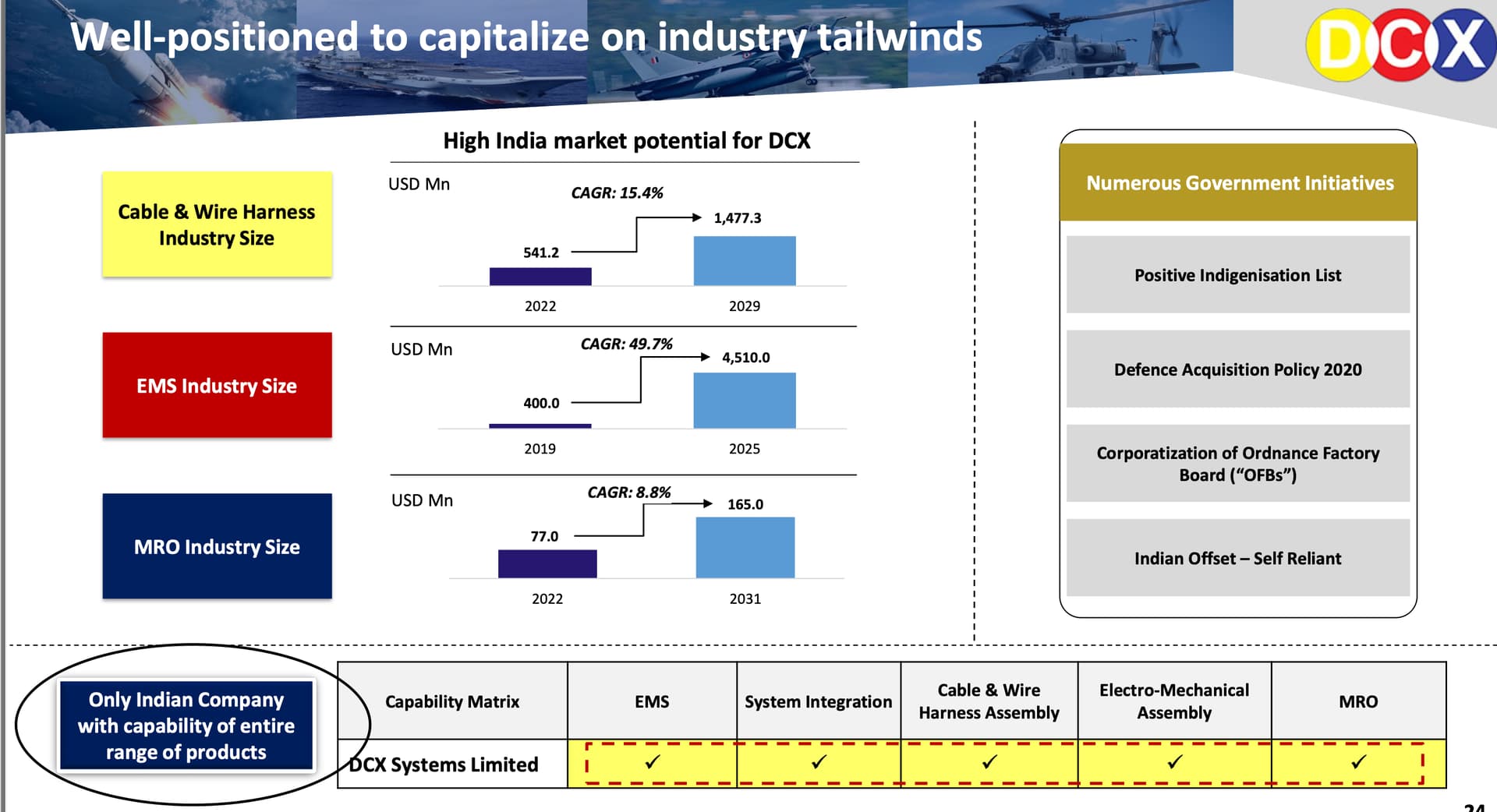

DCX Systems Ltd (22-01-2024)

DCX Systems

Seems to be a fantastic play on wiring & systems for defence and aerospace. Not as overvalued as compared to peers in this category.

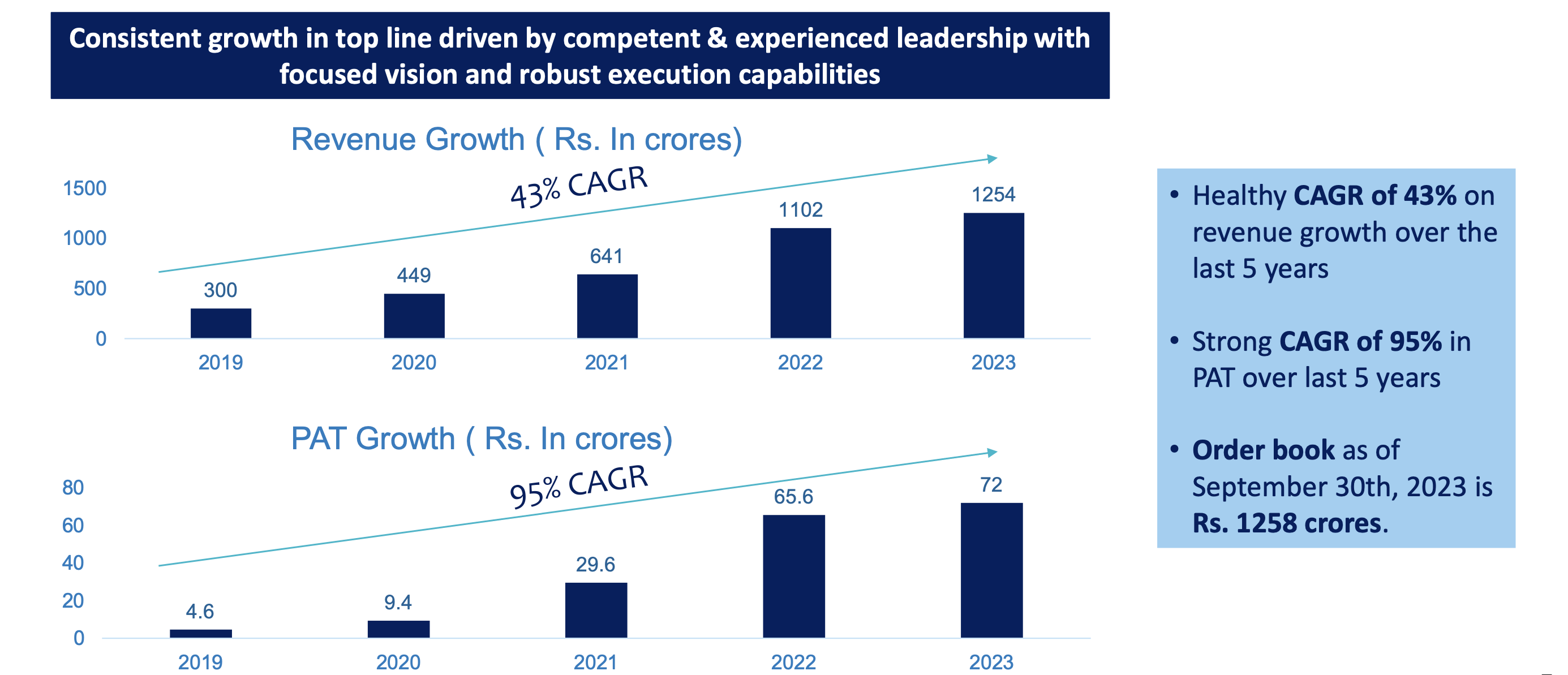

DCX has a unique business model providing end-to-end solutions of cable & wire harnesses, electronic sub-systems, high-end System Integration and PCB Assembly for Defence & Aerospace Industry.

Key Points

-

DCX is a preferred and largest Indian Offset Partner to leading Israeli Defence Company, IAI, for its offset obligations.

-

Core competency in electronics manufacturing with focus on backward integration in PCBA’s through 100% subsidiary, Raneal Advanced Systems – both for captive consumption and other markets

-

Diverse mix of domestic and international customers across Israel, US, Korea and India

-

Strategically located Manufacturing facility in SEZ in Bengaluru, spread over 30,000 sq. ft.

-

New 40,000 sq. ft. facility in Bengaluru dedicated for EMS manufacturing

-

Healthy CAGR of 43% on revenue growth over the last 5 years

-

CAGR of 95% in PAT over last 5 years

-

Order book as of September 30th, 2023 is Rs. 1258 crores.

USPs

Over a decade of supplying to one of Israel’s top defence companies. Very strong relationship that has now made DCX from a supplier into a partner, through the recent JV with ELTA

IOP / Non-IOP partner for Israel / US OEMs to supply wide range of products for Aerospace & Defence

Domain expertise in developing & manufacturing aerospace & defence electronics products on Build to Print Model

Equipment for testing etc. supplied by OEMs, thus facilitating asset light business, despite capital intensive product portfolio

Among preferred Indian Offset Partners for defence & aerospace industry across geographies

Backward Integration into EMS to manufacture PCBA’s for defence & civilian sectors

–

–

Industry Overview

–

ELTA has developed the tech for optical & radar based anti-collision systems for railways. ELTA has partnered with DCX Systems via a JV. DCX owns 51% while ELTA owns 49%. ELTA will supply the tech, DCX will do the manufacturing. The product will be manufactured by DCX and then sold to the JV company, which will then in turn sell it to the Indian government for railways, and also globally to international clients. The global market for this system is $7billion USD. The tech lies with ELTA, manufacturing with DCX, sales with the JV.

–

Found the company and management to be forward thinking and very knowledgable on the domain. Strategic partnerships, backward integrations, end-to-end in-house control, are all very appealing.

Position taken.

*Disclaimer: I invest on management depth, market leadership, sector growth & demand. My holding periods are long, and I’m alright with drawdowns, as long as corporate & business hygiene is intact. NOT an expert, just a dreamer

My portfolio updates and investment journey (22-01-2024)

Sir, what is ur criteria to select a stocks and how to decide valuation of any stock.

I’m selected stock zen technology, RVNL, Fedral bank,CDSL, plectra green but buy very small quantity due to fear.

Sir how to overcome with this fear pls guide.