Posts tagged Value Pickr

Koustubh’s Portfolio (15-01-2024)

Thanks for your question. Will share detailed analysis once research is complete soon.

Koustubh’s Portfolio (15-01-2024)

Made a few additions, updated some information and fixed some typos. Here’s the updated research list:

| Sno. | Stock Name | Sector | Price (INR) | Market Cap (in Cr, INR) | P/E Ratio |

|---|---|---|---|---|---|

| 1 | Ami Organics | Speciality Chemicals | 1150 | 4244 | 55 |

| 2 | International Combustion | Capital Goods | 1423 | 340 | 19.3 |

| 3 | Shree Pacetronix | Healthcare/Manufacturing | 220 | 79 | 19.1 |

| 4 | Control Print | Industrial Printing | 1030 | 1650 | 28.5 |

| 5 | SKP Bearing Industries | Ball Bearings/Rollers | 262 | 436 | 32.9 |

| 6 | Galaxy Bearings | Ball Bearings/Rollers | 1544 | 491 | 27.1 |

| 7 | Aurangabad Distillery | Alcohol | 298 | 244 | 12 |

| 8 | Shivalik Bimetal Controls | Shunts Manufacturer | 584 | 3361 | 43.6 |

| 9 | AAA Technologies | Information Cyber Security and Auditing | 103 | 132 | 41 |

| 10 | Walpar Nutritions | Pharmaceuticals | 104 | 49 | 35.5 |

| 11 | Avro India | Plastic Products | 128 | 129 | 31.6 |

| 12 | Clean Science & Technology | Speciality Chemicals | 1523 | 16178 | 58.7 |

Narayana Hrudayalaya Ltd (15-01-2024)

Yes agree Insurance is not easy. Lets see how they go after this business.BUt if they suceed it will be game changer

Narayana Hrudayalaya Ltd (15-01-2024)

Narayana philospohy is to charge less for outcomes. EBIDTA should be not seen in isolation with captial that has gone into to produce same EBIBTA. They dont invest in buying some hsopitals so they pay rent for example have less EBIDTA but high ROCE. ROCE is king of any business not EBIDTA. High ROCE with high reinvestment means high growth.

Semiconductor world – CPU/GPU Wars (15-01-2024)

I did not give any kind of forward value in my earlier post ![]() Let me do that now.

Let me do that now.

As per Lisa Su, by 2027 we are looking at 400B$ AI GPU investment. But this seems a little too big w.r.t. other predictions – The Tidal Wave Of Rising GPU TAM Raises All Boats).

If AMD does 4B$ of AI GPU sales this year. Say the growth is 25% (Being very conservative) for GPU AI. We will let other biz to grow at 10%.

We are looking at Forward PE for each year at current price (with all other markets holding stable since nothing match 2023 doom and we can expect Embedded to revive by 2025).

Forward PE AT 148$/share

2024 – PE37 – @ 4B$ AI GPU sales + 22B$ Others @ 25% Operating margin

2025 – PE32 – @ 5B$ AI GPU sales + 24.2B$ Others @ 25% Operating margin

2026 – PE28.3 – @ 6.25B$ AI GPU sales + 26.6B$ Others @ 25% Operating margin

2027 – PE25 – @ 7.8B$ AI GPU sales + 29.2B$ Others @ 25% Operating margin

Year 2027 predictions on forward PE

-

Say instead of growing 25%, AMD grows to capture 10% of AI GPU market of 100B$ by 2027. This 100B$ market prediction is at i@ How Long Before AI Servers Take Over The Market?

By 2027 – PE24@148$ per share – @ 10B$ AI GPU sales + 29.2B$ Others @ 25% Operating margin -

Lisa Su says 400B$ AI GPU market

By 2027 – PE13@148$/share – @ 40B$ AI GPU sales + 29.2B$ Others @ 25% Operating margin -

If you go by what is being predicted for NVDA AI Market share of 300B$ and AMD getting 10% of it – NVIDIA predicted to generate $300 billion in AI revenues by 2027 with a 75% market share

By 2027 – PE16@148$/share – @ 30B$ AI GPU sales + 29.2B$ Others @ 25% Operating margin

On average looking at 150-200$ price range till 2027 @ 2025PE without including

- AMD gaining DC market share from intel

- AMD going beyond 10% AI GPU market share – One leaker says 30% of NVDA shipments in 2025.

- GAAP financials – which includes amortisation of xilinx acquisition costs. This should get better with time. Though I do not know precisely how this ramps down.

- What else am I missing?

@harsh.beria93 @kondal_investor Can you please share your valuable inputs on these calculations. Unsure what I might be missing.

Narayana Hrudayalaya Ltd (15-01-2024)

To improve Free Cash flow/(number of beds), they are focussing on ALOS. ARPOB is not a redundant metric. If length of patients staying in the hospital decreases, they can cater to more patients within same infrastructure. Increase volume of medical services for same infrastructure. Increase Overall revenue with reduced requirement for capex.

This will lead to increase in ARPOB, but, that is the resultant KPI, output of the process. And, increase in ARPOB can also be achieved by increasing Prices of medical procedures, deviating from efficiency in business operations. And their purpose of providing affordable medical facilities.

Rather, they are focussing on increasing quality of Input.

And ARPOB cannot be replicated across the whole infrastructure. But, learnings for reducing ALOS can be scaled across the whole infrastructure.

Sorry, I haven’t studied Apollo, so cannot comment on them.

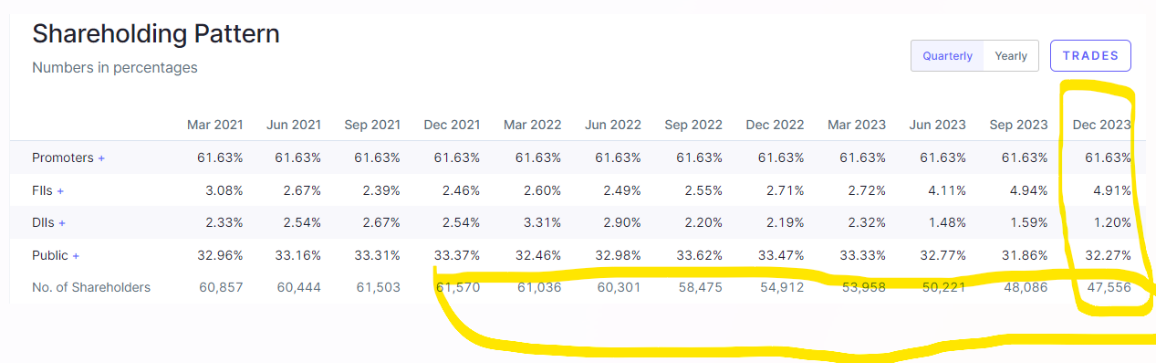

Hazoor Multi Projects Limited (15-01-2024)

Spent 1 day studying the company, key materials studied :

-

All tweets related to the company/promoters on handle @Mumbai_400071. Thanks @Ascendant for sharing the source.

-

Changes in shareholders since Mar. 2019, plus Bulk deals of last few months.

-

ARs since 2018

-

Digital footprints of KMPs & directors

Concluded: It’s a shell company.

Key points : Changes in SHP is telling a lot, sudden change of CFO along offload of shares by Mellora Infra should not be ignored as a coincidence.

Disc. : Exited today at day’s high, made whooping 173% in 2 months. Thanks @chikspat for planting the seed, by starting the thread.

Is China investible? (15-01-2024)

Yeah! Liquidity is super bad but if you’re investing for a big revival then it won’t matter much.