Reco Research report

Share-India-Securities-30-12-2023-pro.pdf (270.6 KB)

Reco Research report

Share-India-Securities-30-12-2023-pro.pdf (270.6 KB)

35k spending criteria is too much. HDFC has 5k spending criteria to give lounge access in the next quarter, this is quite easy for normal spenders also.

This spend based lounge access impacts we may see in Q4 numbers directly, management cautious statement is well appreciated.

I thought impact would be minimal but it seems that there could be some big dip in footfall going forwards for few quarters

Being from this industry this announcement gives me a headache. Fabrication and packaging are very different parts of the value chain. You wouldn’t even be able to buy half a lithography machine for 500 crores lol or put up a decent economies of scale packaging or ATMP (as its called) facility.

The entire semiconductor hype in India is unfounded IMO – we are 5-10 years away from doing anything even on leading edge nodes right now. Investors should pay a close attention to the value chain, technology node and product segments RIR Power is catering to – you will find that its mostly commodity (look at their website). The only project that is worth anything is the Tata Micron ATMP JV and the proposed Foxconn STMicro JV for 40nm Fabrication. If you buy RIR power – buy it not for Semi but maybe an EMS play?

He has always wavered with his guidance and gives extremely vague answers to questions.

Wonderla is entering the high ROCE capital light phase now. Their competitive advantage keeps increasing in size. They manufacture their parks much cheaper than anyone else. At the moment is fairly priced for 12 % growth in price but undervalued for 20 % plus growth. Multiple are reasonable. It is played on a consumption theme. They can maintain single-digit footfall plus a 5 % (inflation) price increase that gives an easy 12 to 15 % cashflow increase. Plus growth will come from Bhuvaneshwar and Chennai. We are also underestimating the pricing power that Wonderla has (even management is underestimating ). The ability for people to spend is way higher.

I was buying at 200 and had no competition last year. Of course, at this price, you need to get growth assumptions right but in my view is still not expensive.

Disc: Invested from 2017 at 250 Rs, so my views can be biased.

RIR is RIR Power Electronics Ltd ? What is your rationale behind investing in this company. The have just secured proposal to ivest 500 Cr+ in Odisha.

Hi Has anyone figured out what is the expected share count post conversation of warrants of promoter and others?. Screener gives 48 CR shares so cash flow per share considering normalized tax of 25 % should be 1.53 and with 25 multiple stocks should be valued at 38.

There will also be maintenance capex any one do any maths on the same? as I guess no maintenance would have been done in the last 3 years.

One small issue with the diagram. Spheroidizing works with natural graphite, not artificial graphite, hence the image is incorrect. Battery Grade Graphite > Graphitization > Anode Paste

@Aditya_Mittal Thanks for asking this question, I was also doubtful of their margin sustaining after Q4 FY23 result.

I don’t think there will be mean reversion to 15-20% as their product mix has changed. The operating margin in case of human NCE is more than 40 percent in peers. Check Suven for the example.

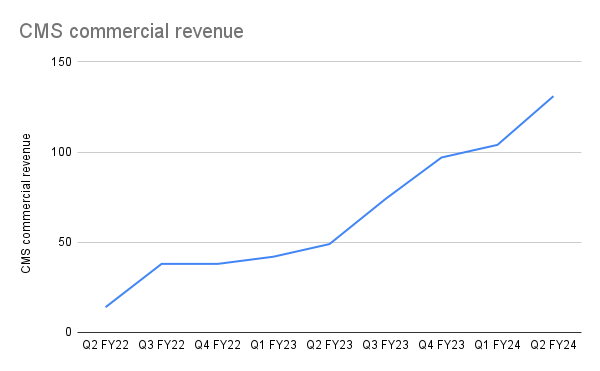

Considering 45 percent margin for the CMS business and 15 margin for their other business, the weighted average of margin comes out to be nearly 31 percent which is what they have attained.

It can obviously drop to 25 – 26 percent for some quarters going forward(as there is some economies of scale playing out) but it will definitely revert back to more than 30 percent once the share of the CMS business increases further and remain above a certain level.

Its revenue from the commercialised molecule from the CMS business is increasing QoQ for some time now. Hence product mix change is here to stay.

The volatility in the CMS business revenue is mostly due to the developmental molecule revenue which fluctuate on QoQ basis.

There can still be some quarters of the volatile earnings(which obviously is a buying opportunity) but as the share of commercialised molecule CMS business increases, the volatility in revenue will decrease going forward.

Other than this I think the KarXT optionality is not baked into the price currently.

Ex of KarXT optionality the valuation of the Neuland might seem on the higher side for some folks but with the KarXT optionality playing out, we are up for the surprise.

Disclosure: Please do your own research, I have a track record for being wrong.

The bear had escaped and is now roaming freely in the forest.

It’s beyond me how the broader market seems to have missed identifying this gem. Starting to see some bytes beginning to appear.

Holding since lower levels and plan to remain invested for as long as execution and numbers live up to the potential.

Honestly feel we are looking at a future star. FY 26-27 will see immense execution.

Also, I like the name Balu. Wild & free.