This news has relevance because it can be a good quasi play on the paints industry. If Asian Paints doesn’t perform, Grasim might (or maybe both will do well). Serving multiple players and new deep-pocketed entrants in the space, bodes well for Mold-Tek.

Posts tagged Value Pickr

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

Hi Dhruv,

Had looked into this as well. In one of the con calls, management mentions that when contracts do come for renewal, government can ask for lower pricing given negligible requirement for additional reinvestment. For example, in Assam teleradiology, Krsnaa quoted lower prices with the rationale that initial investment was already recovered. Not only renewals, this can happen for initial period as well. Take Punjab for example. The payment cycle for this radiology contract is 15 days (essentially cash). In exchange for this, government can ask Krsnaa to lower their pricing. That’s the reason for drop in radiology realizations in FY23.

For pathology, this risk is even higher. Pathology contracts are of shorter duration. Generally three years and then they might extend it for another two years or so. In addition, the competition in pathology also tends to be high. I suspect that this situation can force Krsnaa to quote lower pricing for new contracts or during renewals.

The company often highlights 3-5% price escalation in the existing contracts. While that may protect the realisations during the tenure of contracts, things can change on renewals. That’s just one of the difficulties in dealing with the governments.

Investing Basics – Feel free to ask the most basic questions (06-01-2024)

If it is allowed, I think, there will be more liquidity, and there will be more volatility, although I guess, there will be restrictions regarding the market cap of the companies, only large caps will be allowed, and lesser market cap companies will not be allowed, because they can be operator driven.

I think, this opportunity will help participants who want to participate in the fall of the stock, directly in the cash segment, as doing the same in the FnO segment is risky compared to the cash segment.

Just some thoughts.

Mann’s Portfolio (06-01-2024)

Hey Rankamoksh,

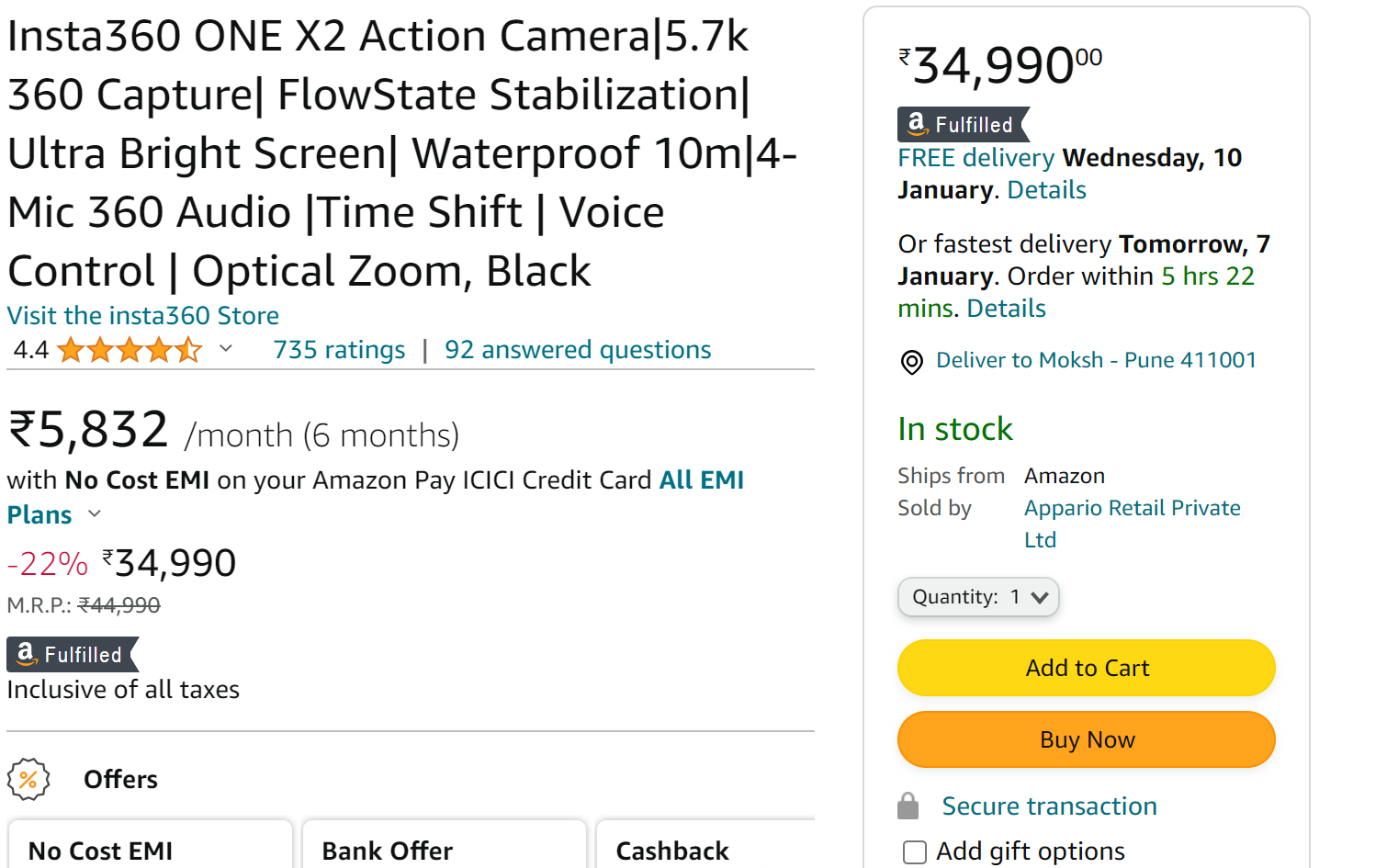

I guess insta 360x is also a enterprise business.

which is basically a trading business.

they are national distributor for Samsung Display, Insta x360, Etc…

You can’t expect the National distributor to supply each and every product themselves.

ese karenge to value chain kese chalegi?

the thing might have happened is that Creative instead of doing all themselves might have sold the same to this Company

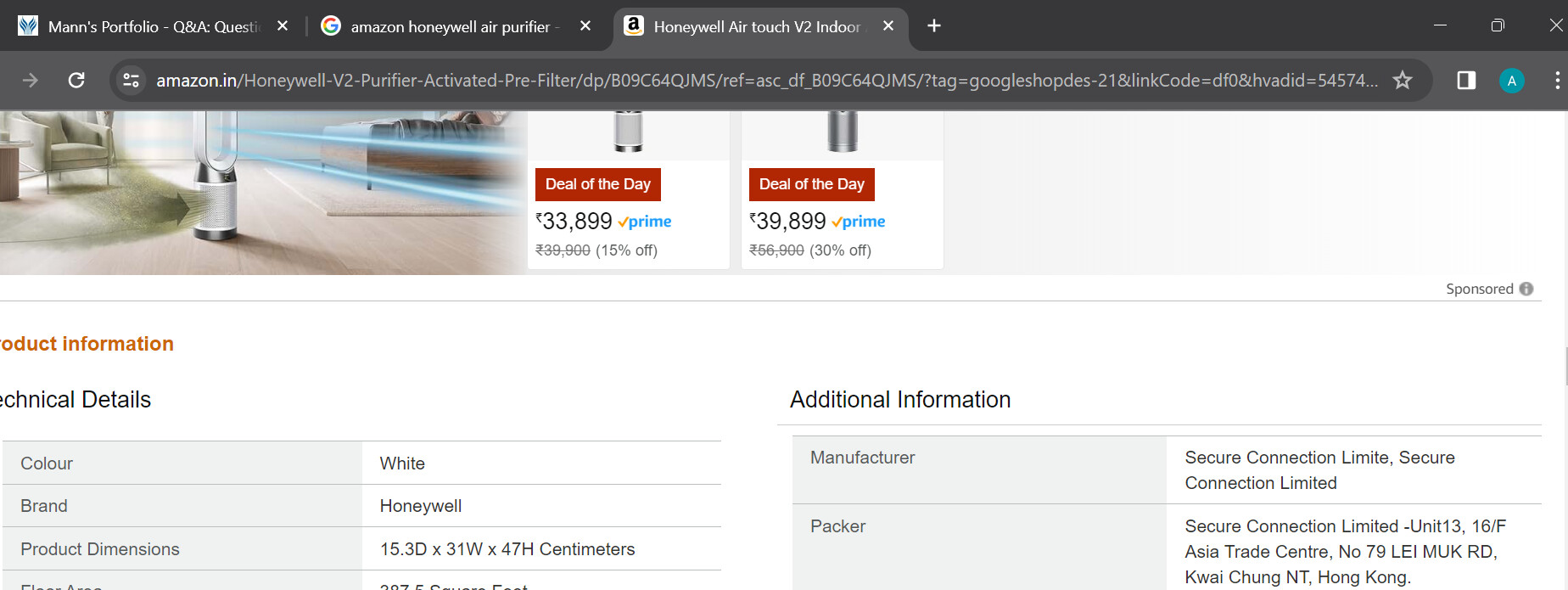

the brand Business – “Exclusivity is in Honeywell business” see the picture below

For that matter any honeywell SKU are through Secure connection only (Creative’s subsidiary)

Now, They haven’t signed “Contract Manufacturing” Deal, They have signed Brand licensing deal, meaning that All brand patents are owned by Creative. the products are made by “Honeywell and Creative Approved Factory”

hence the factory is Contract Manufacturer

Contract Manufacturing is low margin business and hence they don’t intent to enter the same

Instead they are having compete asset light model of business.

Hence for your point there is exclusivity but sab we can’t see siting at the end of value chain

Yes they are infact recently visited Reliance digital and inquired about honeywell’s Air purifier which they stated they had to order it from some entity since it’s out of stock which in turned turned out to be this one

Yes they’ve indicated Once the Honeywell business reaches say 220-230 crores of revenue they’ll sign another brand

Reviews are from service perspective they are distributors and not the service provider if your camera goes bad

it’s Insta’s Responsibility to fix it and not Creative hence most of the reviews might go for toss

I prefer to look at amazon comment or Flipkart’s comment on product rather than this google since i have experienced that some comments may be bought out

Also Couldn’t understand what is wrong with 2-3% margins i mean this is free cash without any investment in Fixed assets. This is cash cow business

Just go through Transcript and you’ll get it

For me SOTP is more than CMP

Ckart has inter generated more than 400 crores of Revenue and Any startup can be valued at 2-3x At sales minimum

Brand licening business can be worth easily 1500 crores if they achieve the target of 500 crores in next 2 years from Honeywell and New brands are cherry on Top

And Traditional cash cow business can be valued at 15-20 PE at max generating around 40 Crores of NP 2 Years down the line

And Hence SOTP is Far more than 500-600 Cr MCAP that i Entered

Arvind Fashion : Value Unlock or Trap (06-01-2024)

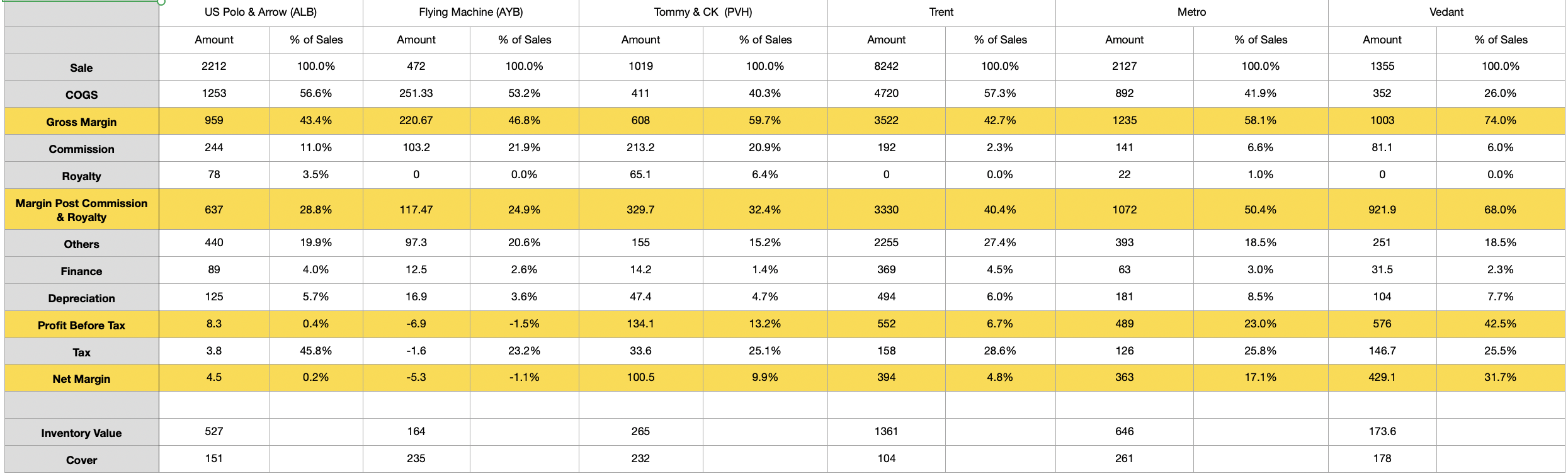

Was looking at the P&L of 3 key subsidiaries of Arvind Fashion and Comparing the same with other retail fashion players for FY22-23. Though not like for like comparison ( Trent has non fashion business also, though very small. Metro also has multiple brands which might have different dynamics individually), it gives an idea regarding the key metrics to look at.

The key call-outs were :

-

Margin post commission & Royalty is the key monitorable as the the difference between this and Profit before tax is more or less constant for each brand/ retailer (except PVH where it seems very low and Trent where it is high). Min 35% seems critical for a ~7-8% PBT margin

-

Apart from Margin, Inventory is another key monitorable, as excess inventory would lead to higher markdown in future. Flying Machine, PVH and Metro all seem to be sitting on pretty high Stock Cover (> 230 days).

-

Gross Margin for Vedant is in another orbit all together. But, unless they crack the Women Ethnic Wear market, scalability might be a challenge.

Disc : Invested.

Mann’s Portfolio (06-01-2024)

I was studying creative newtech, degarding their distribution business since it is just a trading business it has around 2-3% margins, the brands portfolio which they have are very premium and very good ratings on amazon, the sellers of these brands listed on amazon is not creative newtech so is it that they have no exclusivity with these brands or they sell to a firm which eventually sells D2C online and also are they supplying to any retailers such as croma, reliance retail etc. Also their head office in Mumbai has very bad google ratings, since they have signed an exclusive contract manufacturing deal with Honeywell they are able to command 15-20% EBITDA margins do they have any plans or are they doing contract manufacturing for any other brands?

Selecting a broker (06-01-2024)

Hi, Is anyone able to apply IPO for minors? If yes, which service provider?

Note: I used to do it through the bank website of Axis bank earlier (the demat account was with Axis Securities). However, couple of months back Axis Bank has restricted minor logins to their website and the same needs to go through the guardian logins. The bank has not updated their portal enough to be able to access the minors demat account and apply ipo through this guardian login!!

Investing Basics – Feel free to ask the most basic questions (06-01-2024)

(post deleted by author)

Solar Industries Ltd (06-01-2024)

If Solar Industries will be rallied between 2-6%, then I might get included in MSCI standard Index.

MSCI will make the official announcement on February 13, with adjustments set to take place on February 29.

Campus Activewear – betting on the India Consumption Theme (06-01-2024)

Attained concall, recalling from that memory,

o2o is online to offline. Many retailer purchases campus products from U and A. This 2 company consolidated (Some layoff also happened) their businesses and exit platform business of o2o.