I see a doubler in 3 years and legacy book reflection in presentation is a combination of good and bad loans(mostly provided).

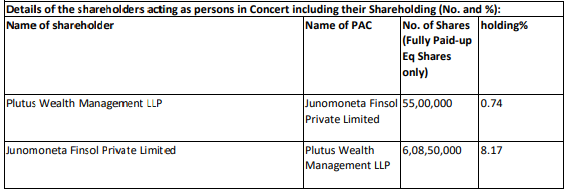

Smart accumulation already in progress as Plutus has increased holding along with PAC.

Gagan is maintaining silence in media and I feel he will make numbers talk.

I am optimistic and invested for long term as market cap of 0.54 book value has more than proviosioned ofr any doubts and things can only improve from here

Posts tagged Value Pickr

Indiabulls Housing – A compounder from here? (19-10-2024)

JNK India ltd – Oil and Gas sector proxy? (19-10-2024)

I could be wrong but below are two observations from DRHP which led me to be away from this company.

Risk 1 – We derive a significant portion of our revenue from operations from orders which are contracted to us by Contracting Customers. We have received projects from Contracting Customers such as Tata Projects Limited, and JNK Global, one of our Corporate Promoters. However, we receive majority of our projects from JNK Global. We work with JNK Global as one of our Contracting Customers and thereby cater to various End User Customers including Indian Oil Corporation Limited in India.

My view: Above tells me that company can have a intermediary influenced by promoter or the Korea partner group where the profits could be stored – with no annual report out yet – check for related party transaction in future. Almost 50% of the orders are from JNK Global.

Risk 2 – We are an asset light Company wherein we outsource our fabrication process to third-party fabricators for most of our projects which presents numerous risks.

My View: How can manufacturing company be asset light ![]() ,Reason could be that promoter Arvind Kamath has many businesses under brand name Mascot and Porvair so work might be going der for processing and hence needs deeper review.

,Reason could be that promoter Arvind Kamath has many businesses under brand name Mascot and Porvair so work might be going der for processing and hence needs deeper review.

Tejas Networks – Product based IT business in a favored sector? (19-10-2024)

Investor presentation, post the results yday

Indostar Capital Finance Limited (19-10-2024)

b6eff5f1-55c0-4873-afa2-64a4a9b1daee.pdf (1.6 MB)

Results are as per management guidance and growth in vehicle finance business is heartening. Post housing finance exit, book value will be more than 300 and current price likely to get re rated in 2-3 years.

QIP proceeds and recent rating change to AA- will help in growth capital and reducing interest rates will support return ratios.

Brookfield parentage ensures governance and Madhu soodan consistent holding gives more confidence in the building story.

I see it as a doubler in 3years. Am I missing anything?

Best Agrolife – Think Big, Think Best! (19-10-2024)

we need to compare these results to Sep 2023 … nothing outstanding IMO… Monsoon quarter is always the same…

Best Agrolife – Think Big, Think Best! (19-10-2024)

The results are outstanding

Excess Capital Value Preservation: Discuss different ways to avoid value destruction by inflation and notify new opportunities (19-10-2024)

Hi

If we can post some updates here, it will be great. Seema to be a valuable thread

Samhi Hotels – Turnaround with Tailwinds (19-10-2024)

No Major Changes in shareholding pattern except GTI Capital Alpha Block deal on 28 June, suggesting a strong hold I guess.

Invested and Biased!

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (19-10-2024)

Due to huge excess capacity and negative margin, Grain based ethanol industry will face a huge crunch… many of the companies will default… capacities will shut down and then balance will be restored. even then the returns will be very moderate…

the companies realising this and folding up earlier will be better placed as the more they delay the interest accumulation on defaulted loans can be extremely high… and what is the point in holding… at the end the industry is going to be low margin for a very long time…

unless Govt. allows import of GM maize… which is vurtually impossible in our country… even for ethanol production.

If others can share their views… it can give a clearer picture on how this industry will evolve.

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (19-10-2024)

Please refer to this post by me – exactly the same things covered in this mint artilce.