Thanks for sharing this. As per the latest presentation, Antelopus Energy has ~20x more 2P reserves vs. Selan i.e. 54.65 vs. 2.57 mm boe.

Thanks for sharing this. As per the latest presentation, Antelopus Energy has ~20x more 2P reserves vs. Selan i.e. 54.65 vs. 2.57 mm boe.

Hey (@Investor_No_1): Valid Points.

All have a big 140Cr. population opportunity. Like Abbott, I have not followed others and am not in a position to make an opinion on the fly. Equity valuation demands a long term thinking to form a view about the prevailing prices. However, one must take action in the short term as per the change in circumstances since competition was there, is there and will be there.

I read Mudit’s view on another thread and was providing him with another perspective. Needless to say, all opinions are proven wrong sooner or later in the equity market.

Both Nestle India and Abbott are good businesses. However, mispriced valuation might make either or both of them great buys. One shall do the home work and be ready to load as and when the opportunity knocks.

1, last 5 years sales will be decent and future sales will be more than 25% .

2,Asset turnover more than 5x .

3, in current asset inventory and receivable have to decrease years on years.

4,debt interest not to be more than profit.

5, depreciation have to be increasing every year.

So basically hiding NPAs was the overall plan under the title AIF.

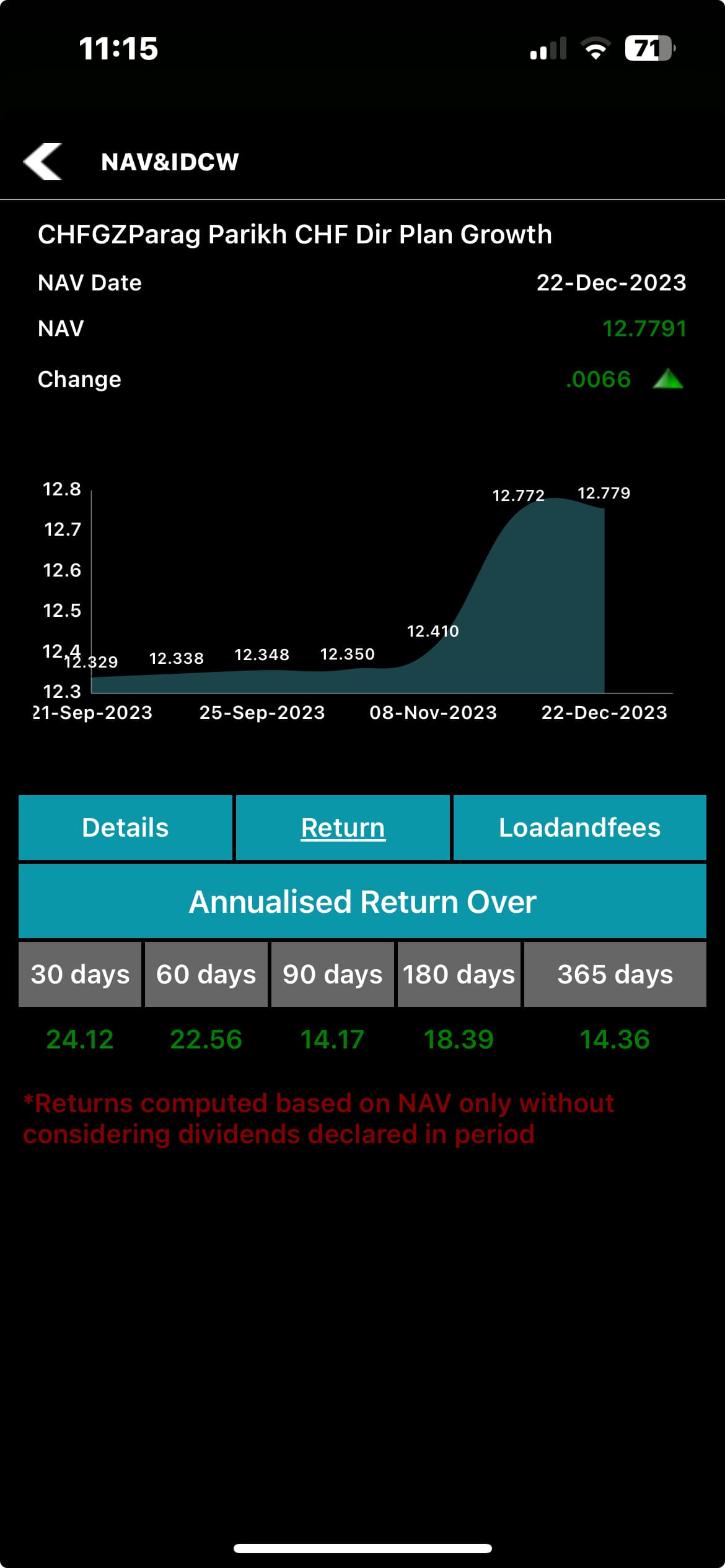

IMO investment in PPFAS Conservative Hybrid Fund (CHF) is a good option. It was launched in May 2021 and since then it has given a return of about 10%. They are investing about 75% in Govt Bonds, 10 to 25% in equity with high dividend yield and about 0 to 10% in REITs and INVITs. There are Chances of delivering 2 to 3% higher than FDs . After 3 to 4 years one can go for a SWP . Sharing the annual performance of the fund.

Disc Invested

If I convinced me to buy that company so I put my money half and in a week if company can gain 2-5% than I buy more .if it lose 10% Iook that company once again If I sure nothing it’s wrong than I invest more not I convinced than I quit.i don’t average my losses stock.

1,Business has to be a pricing power and not so much compitition.

2,most important that industry can grow above GDP growth.

3, is the industry has already participated last bull market so please avoid.(except finance)

4,if u have negative working capital and ROE more than sales (20-30%) .don’t see for cash flow statement it was garentee that company has cash flow is positive.

5, u have to see that ROE is more than topline growth.

A lot of people on bank accounts creation are missing the point discussing number of kids, operative accounts and such. What matters is, the infrastructure for scaling up is in place for fast transmission of money. Are banks intermediaries and gate keepers of these transactions? Yes!

Digitisation of banking services has helped banks to be more prudent in their lending. They can see you financially, if your PMJDY accounts are not active, net zero etc. The question more appropriate to ask is, is HDFC leveraging this to become bigger, better and faster.

I really don’t think so. Note that I’m continuing to accumulate this stock.

@phreakv6, As always a great summary from your end. You have largely focused on the potential of WCK 5222. If we look at the recent news articles, they attribute the price rise to the completion of the Phase 3 study of WCK 4873 (Nafithromycin).

In Phase 3 study, three-day treatment with Nafithromycin resulted in clinical cure for 96.7 per cent of patients as against clinical cure rate of 94.5 per cent in Moxifloxacin arm.

The study also establishes that Nafithromycin represents the first ever macrolide in 30 years which has successfully completed clinical development for the indication of community-acquired bacterial pneumonia. The currently available macrolide antibiotics Azithromycin and Clarithromycin were approved in 1988 and 1991 respectively. Since then no new macrolide antibiotics have been approved despite pneumonia causing about 2.5 million deaths annually worldwide as per WHO.

Do you have any idea how WCK 5222 and WCK 4873 are different? Both seem to be targeting a similar segment of bacterial infections.

Also, if the company gets approval for WCK 4873, does it mean they can target the Azithromycin market? which is valued at 6.9 Billion $

What I see before entry

1, like last 5 or 3 years average profit growth is 40% and stock CAGR is 80%(if profit growth and stock CAGR is equal than I deepdrive into)it’s overvalued I can’t buy cause it’s future earning are already discounted.

2, is stock name are famous than the company if it was true I ignored.

3, is the business is B2B or commodity and trading 30+ PE than I caution.(if the company is small cap u can ignore PE some time)

4,than I read the business if business can sustain over 10 years than I see the balance sheet if it’s not sustainable I ignored.

5,go to screener and see number ofshare holder for last 5 years double it’s ok if 5x or 10x it was indicates that juice is out.