Hi,

I’ve been tracking Shilchar from 1200-1400 levels and has moved all the way upto 2800 levels. Just wanted to understand what is your thought process to add the stock when it’s 6-8x up already this year. Would love to understand your reasoning.

Hi,

I’ve been tracking Shilchar from 1200-1400 levels and has moved all the way upto 2800 levels. Just wanted to understand what is your thought process to add the stock when it’s 6-8x up already this year. Would love to understand your reasoning.

(post deleted by author)

A recent idea that have come to @nirvana_laha and my notice as an ancillary play to EV batteries.

https://www.screener.in/company/HEG/consolidated/

Demand scenario of Lithium ion batteries

Conservatively Battery capacity required by 2030 is around 122 GWh – Source and Discussion with experts.

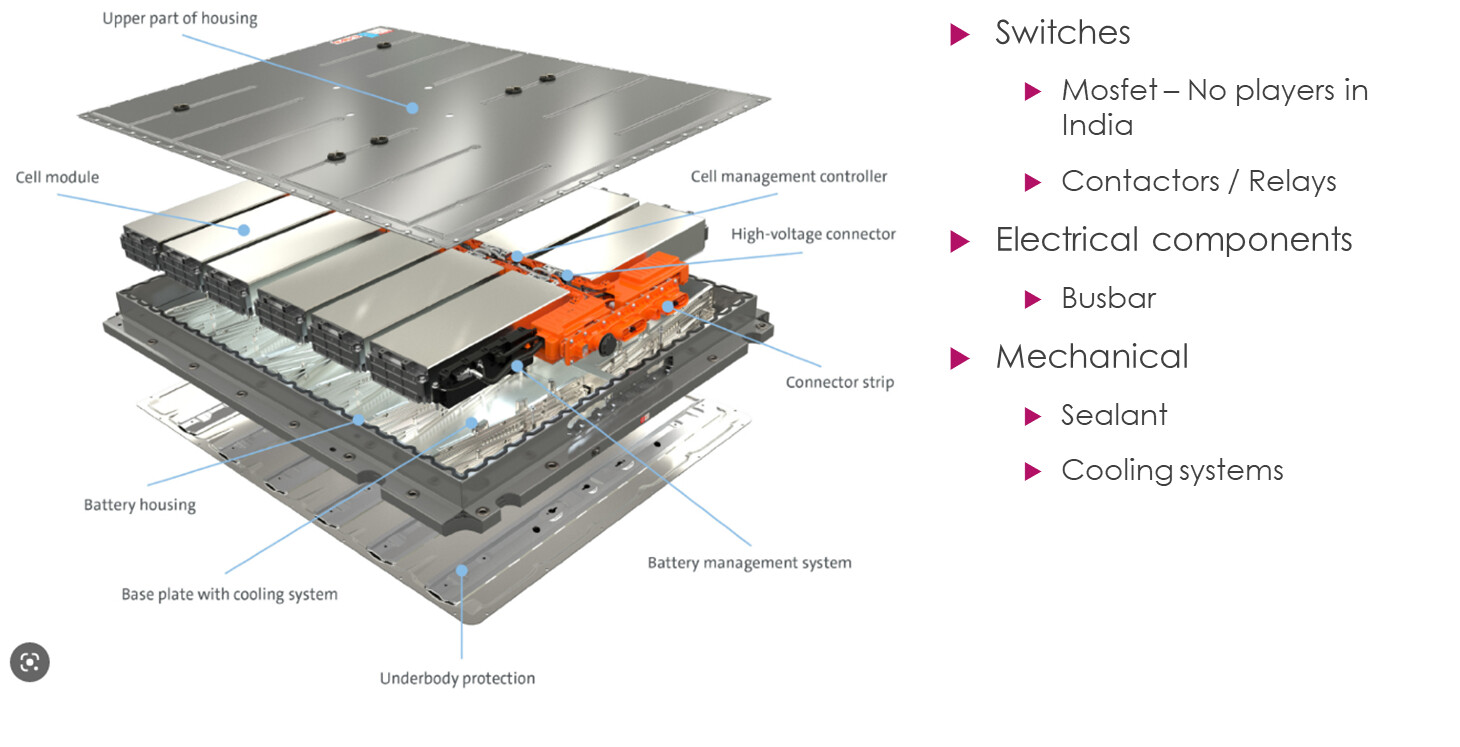

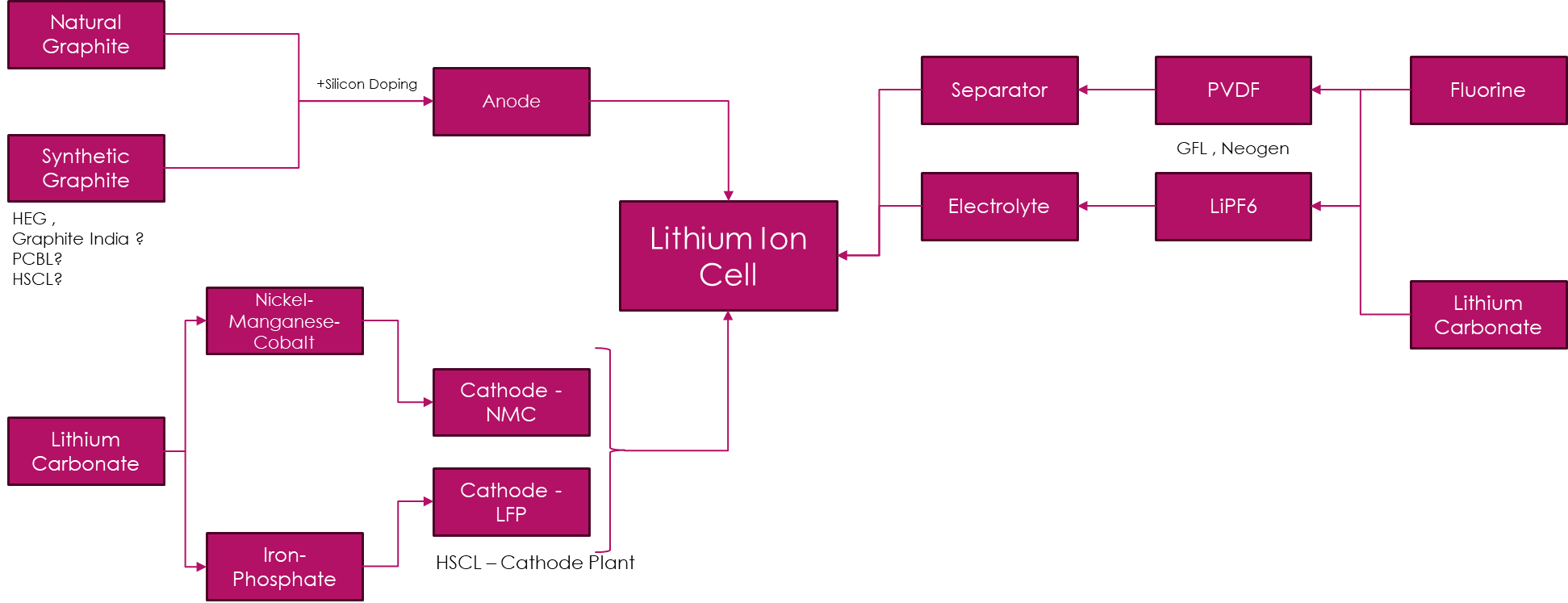

Major components of a Battery

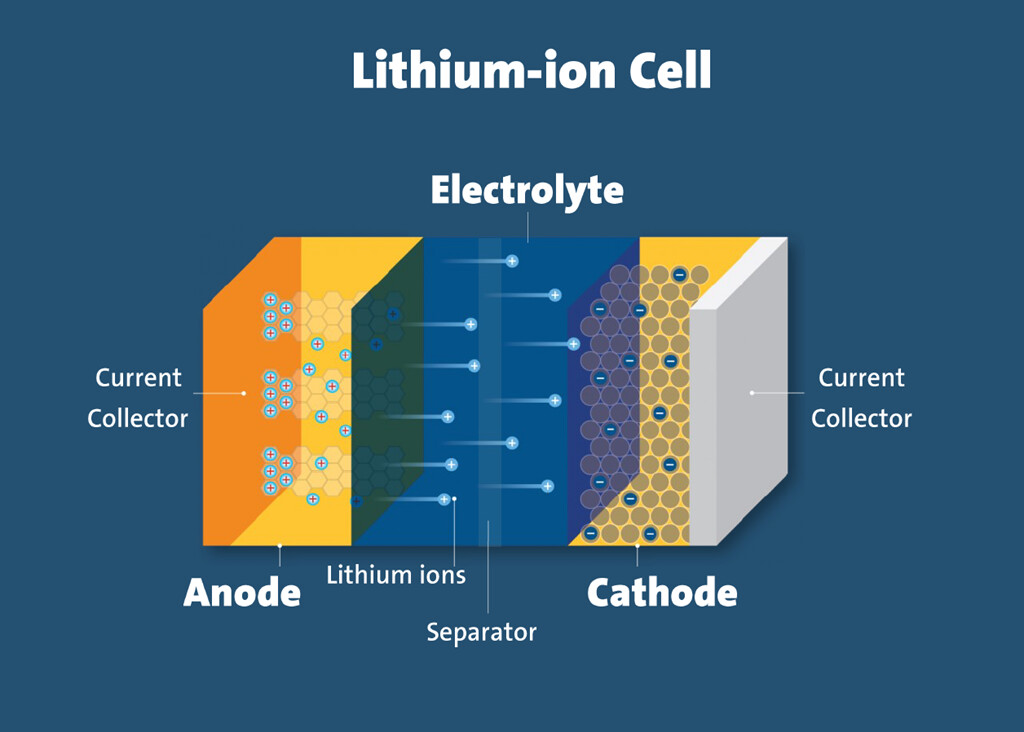

Major components of a lithium ion cell

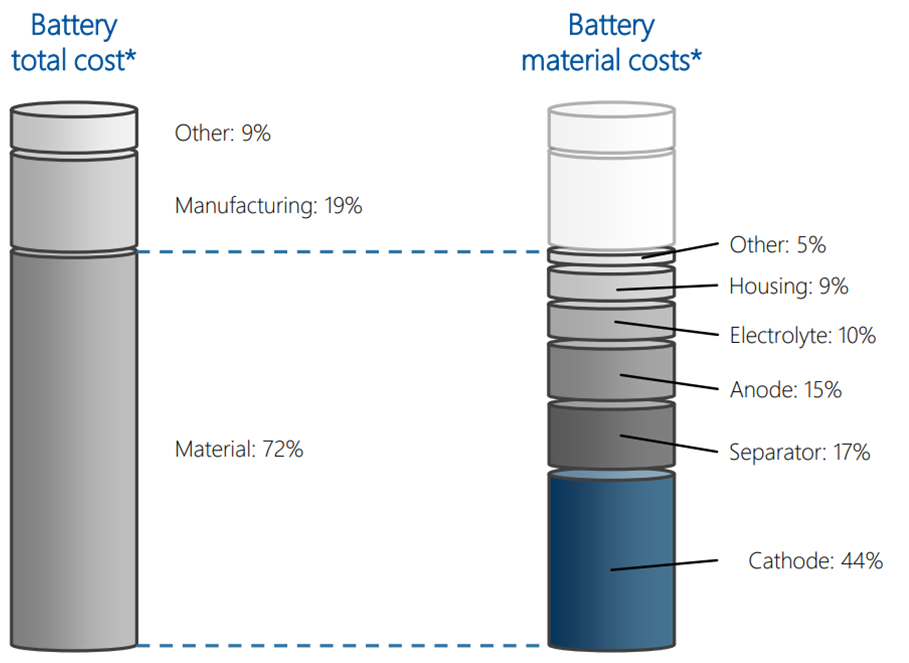

Approximate percentage of anode in a cell by cost source

the battery cell chemistry value chain

Conservatively = 122 GWh of lithium ion battery demand

1 GWh battery requires around 1000 tons of Graphite

Domestic demand by 2030 would be 1,22,000 tons at least. Globally much larger

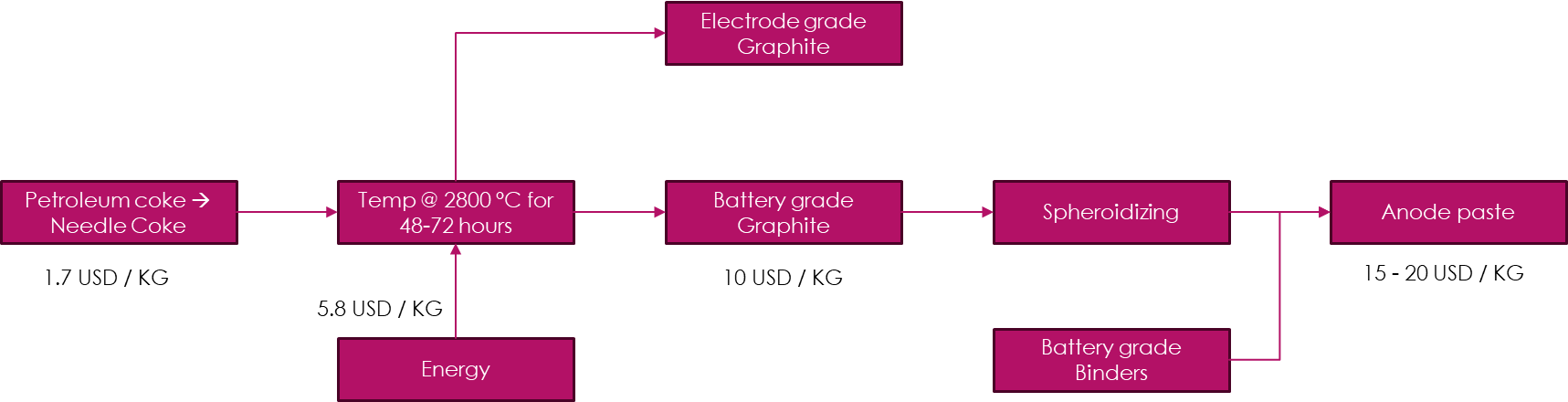

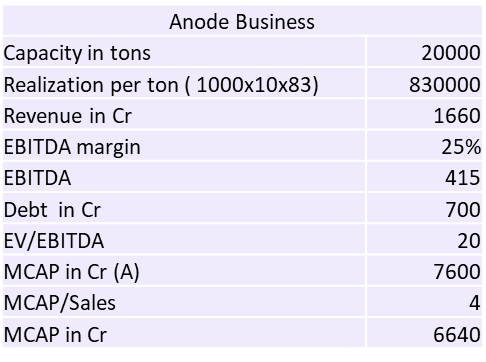

~40-50% of the cost is energy for anode production. HEG is the first company to invest in Capex under subsidiary TACC for 20000 tons by FY27.

HEG’s power cost is 5.5 rupees / Unit vs G.I ~ 8 rupees / unit, the management has claimed that they are the cheapest in the country and competitive with China

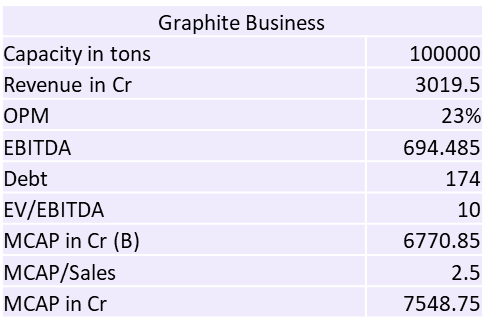

This is the cost structure, HEG’s new subsidy TACC will supply Battery grade Graphite

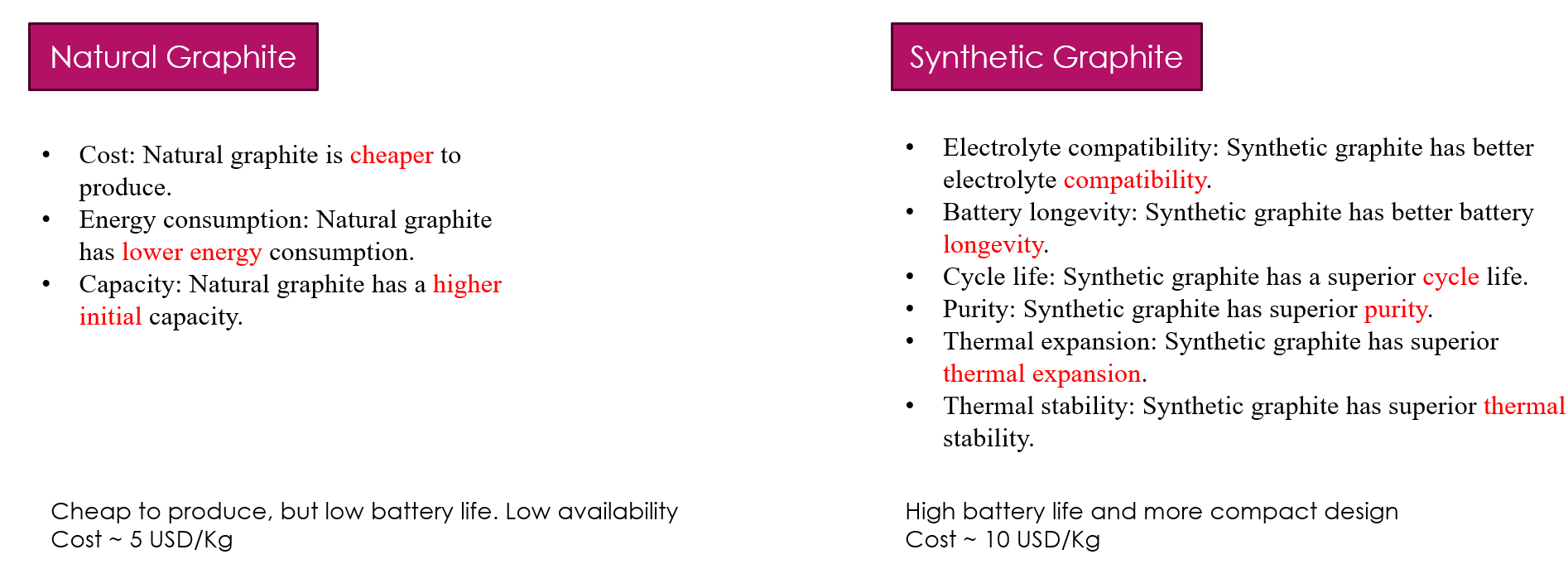

Synthetic graphite’s demand is rising as it can enhance life and fast charge applications. Most manufacturers will make synthetic graphite.

Upcoming trigger

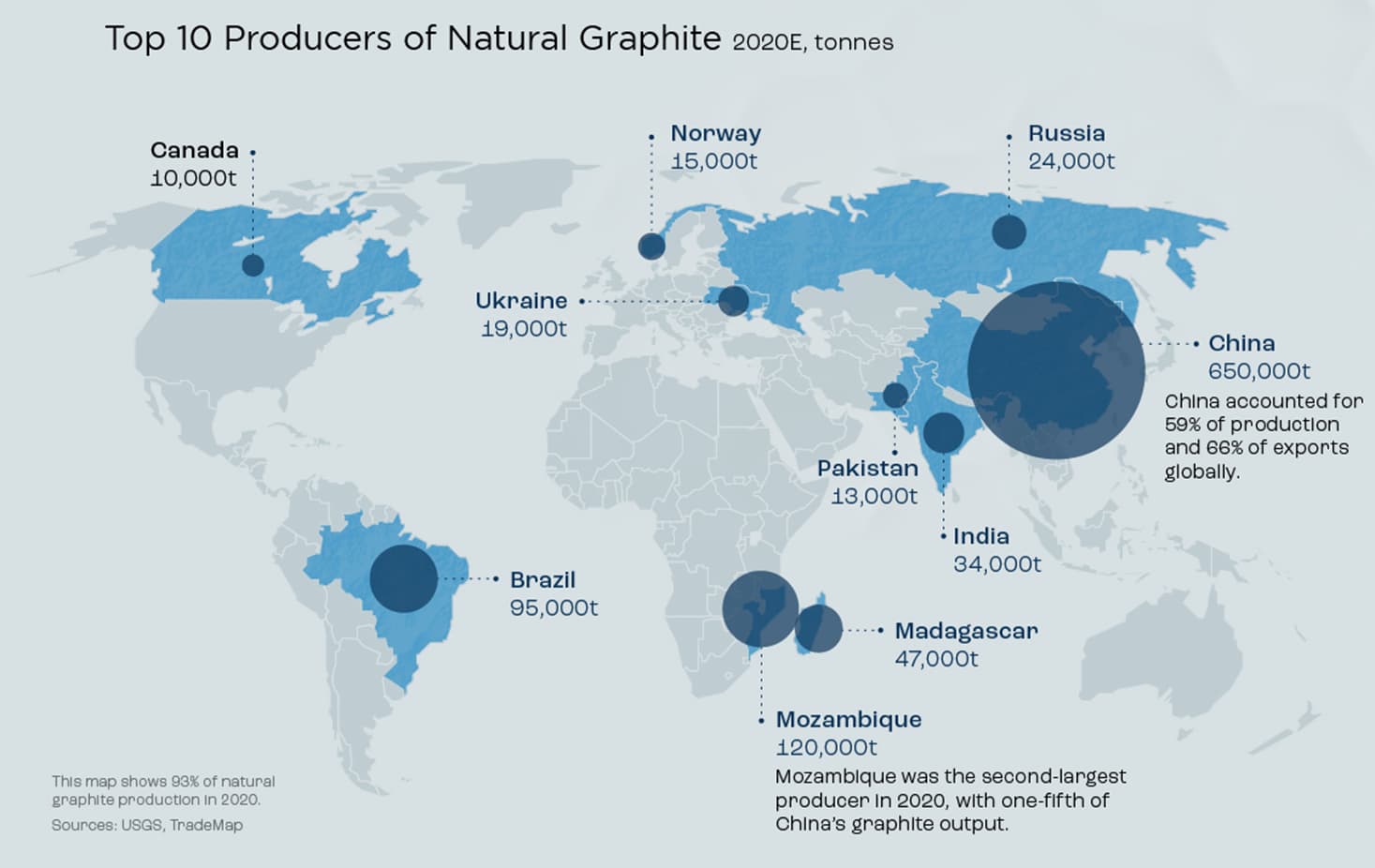

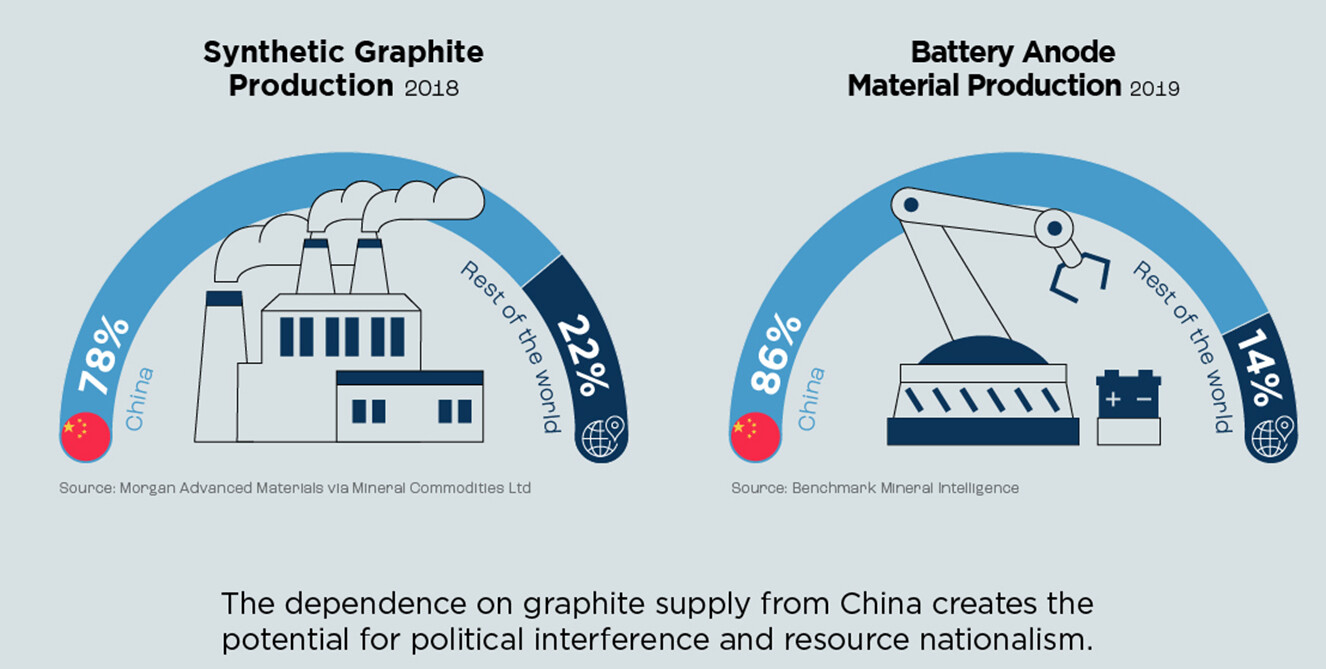

Chinese ban on Graphite export

China is a dominant graphite producer / refiner. The export curb would mean higher cost of Anode powder for rest of the world

Anode powder cost might rise to $14-15 for the rest of the world. Graphite will become a very strategic mineral.

Valuation by FY27

Note:

PEERS

Himadri Specialty Chemicals – Supplies to OLA on behalf of their JV partner, LFP play

PCBL – Not clear if they will venture into anode powder production, but management has indicated that they are definitely on the lookout for EV plays

Graphite India – Invested in some startups focused on silicon anode ( moonshot IMO)

Epsilon – Focus on US markets.

Disc: Invested and Biased. I am not a valuation expert.

Force Motors Rating outlook revised to Positive; Ratings Reaffirmed

FM Rating Rationale.pdf (479.5 KB)

Key Points:

Vikas, Any research around All-E tech? I know this was covered recently in IAS2020 but I didn’t subscribe to it.

I spent some time studying it but at surface I couldn’t find any moat that any run of the mill IT companies doesn’t have. My back of the envelope assessment of IT service companies goes like this. Calculate revenue per employee and see how they fair in comparison.

For All-E tech, 2023 revenue is 88 Cr for 331 employees (as per AR). This comes to 26 lakhs per employee. This is no different than others. In fact it is less than lot many mid size IT companies.

So why?

Any idea what are these guys upto by doing all these corporate actions?

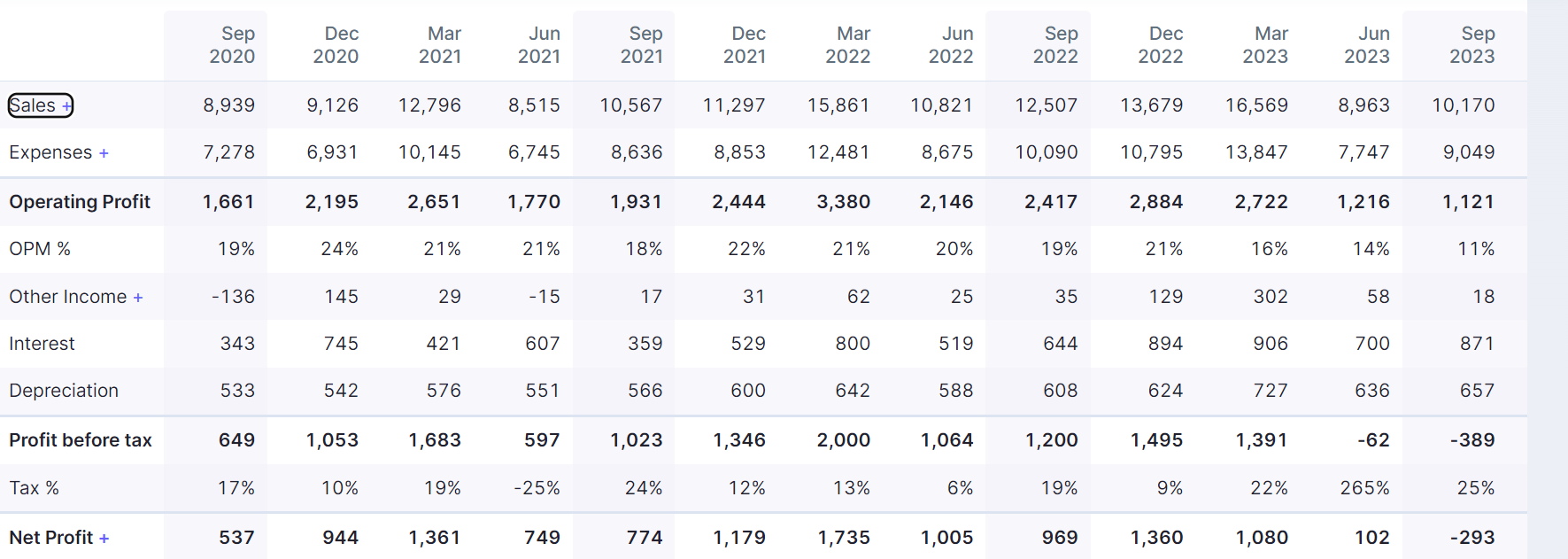

EBITDA this year will probably be the lowest for them in the last five years.

I am unsure where this company is headed and whether the thesis continues to hold.

(post deleted by author)

Update:

25% of folio churned, with 2 full exits and 8 fresh additions.

Trying to change the theme, it’s been good years recently but have to stop pretending to be a serious investor ![]() size now offers comfort to take risk more. Missed so many sectors, pipes, cables, rail, defence, EMS, PSU so on. A more diverse bet would likely pick up some of these early which can be pyramid on up or milked occasionally but position kept (since sell triggers often an up swing

size now offers comfort to take risk more. Missed so many sectors, pipes, cables, rail, defence, EMS, PSU so on. A more diverse bet would likely pick up some of these early which can be pyramid on up or milked occasionally but position kept (since sell triggers often an up swing ![]() ). Maybe results overall wouldn’t be much different, this diversity bug bites me every other year, and then I slowly consolidate the winners.

). Maybe results overall wouldn’t be much different, this diversity bug bites me every other year, and then I slowly consolidate the winners.

Some small caps reach a point of inflexion where even though their exponential profit graph flattens but real long term strength appears. For not so agile investor, it can be a point of entry. Indian manufacturing exports are booming, with true domestic value addition like auto.

Added Sharda motors, it’s supplying mainly emissions control systems with one of largest market share in India and now started exports to US, bit slowly, decent value buy, tie-up with kinetic for some BMS etc.

Added Satin credit since interested in micro finance nbfc and ujjivan seems to be moving away from the sector 🤷🏽♂

Added E2E which is selling cloud infra, GPU focus with growth likely due to AI.

Added Ceinsys which is doing geospatial studies and recently took over auto design company based in US. Maybe just superficially cheap.

Also added Shilchar which is making transformers with exports growing, new capacity under construction, 1 more year wait required with max capacity reached. Transformers shortage globally, scaling production may take 5 years approx.

Added All E tech which is just Microsoft solutions provider but apparently it’s in a sweet spot to grow.

Added Beta drugs oncology drugs maker, with exports to developing countries mainly, doing well in India also, addition of dermatology products recently.

Added Roto pumps which is making non centrifugal pumps, major exports, growing faster due to China+1 and Europe+1 theme. Looks like they are expanding capacity.

Fully exited Redtape and Best Agro.

I don’t understand much about fashion brands ![]()

Reduced Kilpest and Ujjivan financial by half.

Also reduced from Gujarat Themis, Shivalik bimetal, KPI green, RBL, Tinna in that order. Kilpest doesn’t seem to have the strength to grow that fast and my position was about 10% of folio, bit large, with 350 average buy. Gujarat Themis is showing slow progress in capacity addition, one year more for sales to start. Shivalik bimetal capacity rampup will take time depending on global macros, electronics sales, ev growth story, 30% cagr for few years is mostly priced in. Rest booked had grown 3x and needed diversity IMO. Best agro was loss booking for saving taxes. ![]() Also total holdings are 19 now, bit large but then I don’t study that well to make concentrated bets! My effort is to follow GARP strategy

Also total holdings are 19 now, bit large but then I don’t study that well to make concentrated bets! My effort is to follow GARP strategy ![]()

All new positions are roughly equal size, each about 4% of folio