you need not worry if you are investing bottoms up

Posts tagged Value Pickr

Bull therapy 101-thread for technical analysis with the fundamentals (15-12-2023)

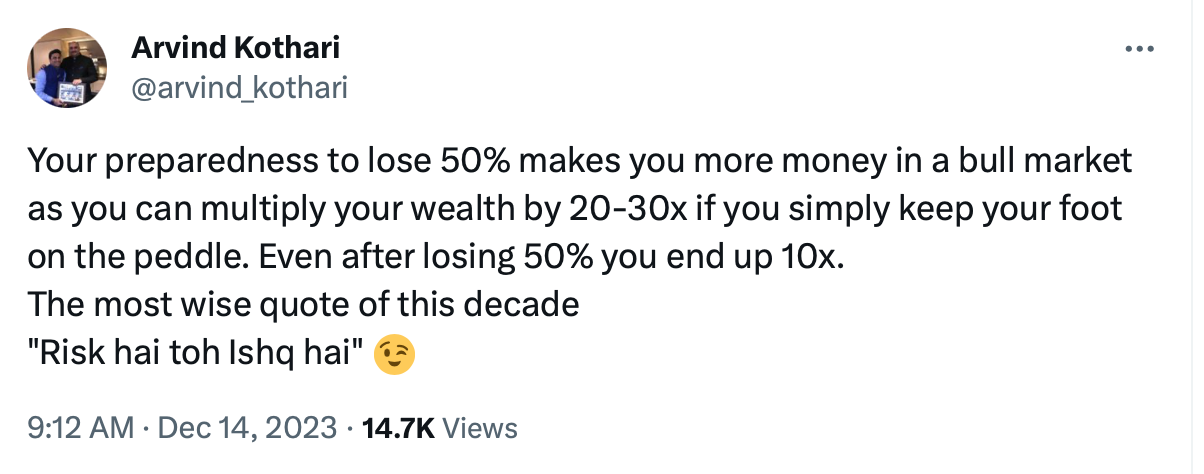

So, the bull run continues and I am keeping this quote from Arvind Kothari in mind.

So, be prepared to lose some money from your basket which has been increasing since April. This will make sure that you will enjoy this bull market and not exit early.

But the market looks stretched here. I will be alert and focused and I will make sure not to lose much from here if there is any correction in the market. Also should not run after every breakout in some kachra stocks.

The regret will always be there, I missed this stock, I missed that stock. I exited early, and so forth.

The SmallCap Index is up more than 11% in just one month after my last note.

In the last 2 weeks, large caps also showed similar strength to mid and small caps may be due to the return of FIIs or state election results.

Disc: Update on last month’s trades

Still holding my position moving slowly if this crosses 300 then further upside possible.

Also, there are a few new orders received by the company. and promotors were also buying from the market.

Closed my position with little profit as it was not moving as expected.

Simple clean move. Booked 50% today on this trade and trailing the remaining position.

I used to book full positions either in or out completely but I have missed many up moves so don’t want to miss either or give back all my gains to the market so trailing with a 50% position. Will book remaining position even with early signs of weakness.

The power sector, PSU, and mining magic playing out

Holding all the positions with Trailing stop-loss at 200. If it closes below 200 then I am planning to close it at the end of the day.

For the upcoming week my focus is on selective Pharma and chemical stocks.

Orchid Pharma came on my radar after the gap-up on 8th December and today it crossed the tight range with good volumes.

Fundamental triggers: Merger with Dhanuka Lab, promotor holding to surge to 74.45 pct vs 69.84 pct due to proposed merger of Dhanuka Lab research upgrade. The company also targets to 1400 cr turnover.

Orchid Pharma | Source: JM Financial

- The management is confident of delivering 20-25% Revenue CAGR over the next few years (excl. PLI);

- The company is also guiding for 100-150bps EBITDA improvement annually;

- The company has multiple growth levers: (1) capacity expansion; (2) new product launches in regulated markets; (3) PLI for 7ACA and downstream products; (4) NCE Enmetazobactum; and (5) Cefiderocol, which will play out in the next 4-5 years;

- The company is at a land acquisition stage in Jammu (for PLI) and expects an update by the end of this fiscal;

- The company is now debt-free. Post-takeover, the company has taken several cost initiatives to improve margins. Strategically, the company is backward-integrating and forward-integrating its operations to become an integrated player in cephalosporins.

|| Gap-up stocks are generally considered strong technically if the gap is not closed and the price consolidates with the gap ||

This happens when there is overnight something positive development or news and the market has not discounted it previously.

One more example of a Gap up and then price consolidating in the range is Ceinsys Tech Ltd.

You can read more about it in the previous post of @phreakv6 with the upcoming triggers.

:: Just sharing my thoughts and update of last post

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (15-12-2023)

make molasses without causing sugar shortage…so how is this a cyclical uptrend?

Pondy Oxide & Chemicals (15-12-2023)

Pondy Oxides & Chemicals Ltd

ROCE:- 24%

Market Cap:- Market Cap₹ 511 Cr.

P/E :- 14.1

Stock Price:- 439 Rupees

POCL is a leading manufacturer and recycler of Lead, Aluminium, Copper Alloys, and Plastics.

History

Pondy Oxides and Chemicals Ltd Incorporated as a public limited Company in Tamil Nadu and listed on the Madras and Coimbatore Stock Exchanges (Regional) at 1995.

Then They Set up Litharge, Red Lead and Zinc Oxide production plant in Pondicherry in 1996. In 2003, They Set up new unit in Tamil Nadu for lead acid batteries.

In 2015, They Set up new SMD-II plant in Andhra Pradesh.

In 2023, The Company successfully established and commenced operations of an Aluminium Recycling/Melting facility at its factory in Sriperumbudur, Tamil Nadu.

Business:-

They manufacture Lead, Tin, Aluminium, Copper Alloys, and Plastics.

Lead:-

Lead has been one of the oldest metal known to have widespread uses commonly due of its properties like easy extraction and to work with, highly malleable, corrosion resistant and so on.

Their Products :-

Lead alloys :- Pure lead, lead calcium alloy, lead antimony alloy, lead master alloy, lead tin alloy, and other specialised value-added alloys.

In lead, about 50% to 55% is the general pure lead and 45% to 50% is the alloys.

Uses:- The largest use of lead is in the lead acid battery industry. It is also used for radiation shielding, ammunitions, roofing sheets, extruded products, solders in the electronic, plumbing and automotive industry. Some other uses like cable sheathing, pigments, glass and others also contribute to the consumption of lead.

In cable industry where lead is used as a sheathing mechanism which is also growing and also there is radiation industry, x-ray machines and nuclear power plants.

Process:-

Procurement:-

In terms of procurement, They have a mix of 75% imports and 25% domestic sourcing.

They do tie up with OEMs either battery manufacturing OEMs or car manufacturing OEMs and they collect batteries from their workshops.

For retail batteries that are being used by E rickshaw and especially in countries like India, they come from retail network.

The lead content in a Lead Battery is around 60 to 65%. It also contains some plastic, rubber etc.

Price is around around 50% – 60% of the L.M.E.(London Metal Exchange) Prices for 60%-65% of the Lead in the Battery.

Plants:-

SMD I – In Tamilnadu

SMD II – In Andhra Pradesh

SMD I has a capacity of 96,000 MTPA, in Tamilnadu.

SMD II has a capacity of 36,000 MTPA, in Andhra Pradesh.

Automobile lead acid battery recycling plant

Scrap Batteries Goes Into A First Auto Cutting Machine ( Acid Collection) – Belt Conveyor – Primary Shredder – Screw Conveyor – Secondary Crusher – Vibrating Separator ( Separates Lead And Other Materials ) – By Using Water Flow, Plastics are Separated ( As the density of the Plastic is low ) – Collection Of Lead Metal And Lead Powder – Then Melted in the Rotary Furnance

Customers:- Clientele comprises reputed players such as Amara Raja Batteries Ltd, Sebang Global Battery Company Ltd and Glencore International AG.

Their sales composition consists of 60% exports and 40% domestic proportion.

Aluminium :-

Products:-

Aluminium alloys, Aluminium and Aluminium Alloys.

Procurement:-

85% to 90% imported and the balance will be domestic.

Customers:- They are new in the business. They are getting orders from O.E.M.s.

They have plant in Tamilnadu with a Capacity of 14,750 MTPA.

Plastics:-

Products:- PPCP, Plastic-ABS, PVC, industrial and engineering plastics

Procurement:- currently 70% is procured domestically and 30% is from various other sources.

Customers:- The primary industry could be battery industry, furniture manufacturing, flooring sheets, paint manufacturers – paint boxes, and all these box packaging industry etc.

They have of capacity of 9,000 M.T.P.A.

93% Of The Revenue Comes from lead division.

And the rest 7% Comes From Plastic and Alumium Division and Copper Division.

Industry:-

The Global Recycling Industry was valued at USD 60.41 Billion by the end of 2022 and is projected to reach USD 88.01 Billion by 2030.

The Indian waste management market size is estimated at USD 32.09 Billion in 2023, and is expected to reach USD 35.87 Billion by 2028, registering a CAGR of 2.25% during the forecast period (FY 2023-28).

Lead

The lead market is projected to register a CAGR around 7% during the forecast period. The following graph shows the global lead acid battery market from the year 2022 till 2032 (value in USD Billion).

The global recycled lead market size is projected to hit around USD 20.4 billion by 2030 with a registered growth rate of 3.5% over 2020-2026 (Source: Precedence Research and GM Insights).

Indian Lead Market Outlook

Aluminium

The global aluminum market size was estimated around USD 179 Billion at end of the year 2022 and is expected to hit around USD 278 Billion by 2030, growing at a compound annual growth rate (CAGR) of 5.61% from 2022 to 2030.

Indian Aluminium Market Outlook

Total aluminium (primary and secondary) demand in India in fiscal 2022 is estimated at 3.9 million tonnes, logging a CAGR of 4-5% over fiscals 2015 to fiscal 2022.

Demand for secondary aluminium revived by 21-22% on-year and the industry increased at a CAGR of 10% to 1.66 million tonnes in fiscal 2022.

Thus, total secondary aluminium demand is expected to increase at a CAGR of 6-7% to reach 2.2-2.3 million tonnes by fiscal 2027, from current demand of 1.66 million tonnes in fiscal 2022.

The demand for secondary aluminium in India zoomed at a CAGR of 9-11% from fiscal 2015 and 2022, while primary aluminium demand registered a CAGR of 1-2% only.

The global market for copper estimated at USD170.9 Billion in the year 2022, is projected to reach a revised size of USD 242.8 Billion by 2027, registering a CAGR of 6.2% over the analysis period FY 2022-27.

India’s copper imports, are anticipated to grow 3.4% yearly to reach USD 6.9 Billion by 2026. In India, copper is an essential metal that has been widely used in various industries for centuries due its superior properties such as electrical conductivity, thermal conductivity, ductility, malleability, corrosion resistance and toughness among others.

the use of copper in India is to see an annual growth rate of 8% or more enabled by rising demand from traditional sectors such electrical applications, building and construction and white goods such as air-conditioners, refrigerators and washing machines and also from growing official focus on decarbonising the economy. Growing demand of copper will also be seen say for a creation of 1 mw of solar cell capacity, there will be requirement of 6 tonnes of copper.

Plastic

The global Plastic Recycling market size was valued at USD 44,290 million in 2022 and is forecast to a readjusted size of USD 65,050 million by 2029 with a CAGR of 5.6% during 2022-2029.

Indian Market For Recycled Plastics is anticipated to increase at a compound annual growth rate (CAGR) of 11.30% from FY 2023 to FY 2028, reaching 18.50 million tonnes (Source: Market Research and IMARC).

Management:-

Mr. Anil Kumar Bansal, B.Sc., holds the position of Executive Chairman and Whole-time Promoter Director. He has more than 25 years of experience in this industry.

Mr. Ashish Bansal holds an MBA degree and joined POCL in 2009. Elevated to the position of Managing Director in 2015.

Peers:-

Gravita India Ltd

Market Cap :- ₹ 7,179 Cr.

O.P.M :- 9%

FY 23 Revenue:- 2,801 Crores

R.O.C.E. :- 31.6%

Nile Ltd

Market Cap :- ₹ 268 Cr.

OPM :- 5%

FY 23 Revenue :- 806 Cr.

ROCE :- 15.0 %

Growth :-

- Capacity Expansion

They are operating at about 70%, 75% and They are targeting to double their capacities in the next two years.

Harsha Exito Engineering Private Ltd land is where the company is looking at adding the new verticals and also the current expansion on the lead capacity will be done at this specific site and which is ongoing at the moment.

- They have a target to achieve USD 1 Billion revenue before this decade.

- Battery Waste Management Rules 2022

The Government of India has recently introduced new rules on Extended Producer Responsibility (EPR) through Battery Waste Management Rules (2022) for battery waste management. These rules apply to battery manufacturers and importers, and are designed to ensure that they take responsibility for the collection, recycling, and disposal of their products.

- Unorganized To Organized

For Lead,

Only 30% – 35% Market is organized.

For Plastic,

10% would be in the organized sector and more than 90% would be in the unorganized sector.

- Aluminium And Plastic Division

These Plants are working on 30% Capacity only. As they are new in this segment, so it will take atleast one year to improve the capacity utilization. For Aluminium,market should be somewhere around 7 to 8 lakhs per annum

- Margin Expansion

Lead Segment Margin Is 5% – 6%. But, In Aluminium And Plastic Segment, Margin Can Go Up To Nearly 8% – 9%.

- Exploring diverse business domains within the POCL Group, including e-waste, lithium-ion recycling, rubber, oil, glass, paper, and value-added products.

- FY ’25 our targeted top line is around INR1,800 crores to INR2,000 crores, and in FY ’26, in excess of INR2,700 crores.

- We are definitely concentrating on value-added products.

- Inorganic Opportunities.

Risks:-

- Volatility in Commodity Prices. Aluminium prices are not the basis of the LME, So it cannot be hedged in the exchanges.

- Limited energy density compared to lithium-ion batteries – Environmental concerns related to lead content and recycling – Relatively shorter lifespan compared to some alternative battery technologies.

- Low Volume Growth On The Lead Segment. This segment has generated 93% Of their revenue.

- Their O.E.M. customers are trying to go backward integration in terms of getting compliant with the battery management handling rules.

- Slowdown in demand as the demand from China is very low.

- Difficulty in procuring batteries at cheaper prices.

Follow Me On X / Twitter :- investordas

No Reco

Praveen’s Portfolio (15-12-2023)

Hi sreeram

Thanks for your question

I made a list of the stock I’m interested in and I track them with a google sheet

| Company | CMP | Industry | Today’s FY | Target Year | Target Metric | Profit/Ebidta/Sales/Book value in Target year | Target Multiple | Exp Market Cap | CAGR |

|---|---|---|---|---|---|---|---|---|---|

| FLUOROCHEM | 3231 | Chemicals | 2023.7 | 2025 | P/E | 1300 | 35 | 45500 | 21.1% |

| ANGELONE | 3253 | NBFC | 2023.7 | 2027 | P/E | 2500 | 25 | 62500 | 28.5% |

| TANLA | 1091 | IT Services | 2023.7 | 2025 | P/E | 650 | 25 | 16250 | 8.1% |

| DEEPAKFERT | 658 | Chemicals | 2023.7 | 2026 | EV/EBIDTA | 2900 | 8 | 23200 | 38.9% |

So bassed on this kind of list I see where I can get most return in CAGR terms and invest accordingly. So, wherever I allocate more where the odds are in my favor. In addition to this I follow a few more things

- Reduce the weightage where drawdowns could be bigger

- Keep allocation to each sector less than 20% (Chemical and Agrochem is still less than 20%)

- Exit gradually where the risk reward is diminished or keep stoploss. (exited Angelone and MCX partially because of this reason)

- Follow what my mind says in addition to the numbers in the sheet

IT and ER&D:

- I pay lot of attention to valuations and PEG. So, I didn’t find many good bets in IT cos here. All the big IT cos are trading at >25x PE for grwoth of 10-20% and same for ER&D. So, didn’t invest much in IT cos

- Cigniti tech is an IT co which is still available at 17x P/E and I’ve invested here a few months ago

- Mold Tech Technologies is in Engineering services work and supports customers mostly in NA. So, you can say I have some weightage to this ER&D co

From both these cos I expect >20% CAGR revenue and profit growth and found the valuations attractive at my buying price and even at current price

Auto Anc:

Mayur Uniquoters is the only Auto Anc in my PF

Chemical cos:

As I’ve mentioned already I pay attention to the price I pay. IMO chemical cos are at good valuation and the drawdown would be very small from here. In fact after very bad results in recent quarterls the stock prices didn’t fall much. I expect the cycle to return to normal atleast in next 3 years and with the earning improvement and valuation rerating I expect to double the money in next 2-3 years. Shortly better Risk reward

Hope this clarifies.

Praveen

Disc: Invested and biased

IRM Energy – A new kid on the (listed CGD) block (15-12-2023)

There may be some truth to what you are saying. Glassdoor rating for Cadila Pharma is low 3.1 but same for IRM Energy is 4 (caveat only 9 reviews) and 3.4 for Adani Gas.

So work culture at IRM energy seems to be positive and CEO is a professional coming from engineering background having worked at Kalptaru Power and KEC.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (15-12-2023)

Rico Auto also is claiming to be supplier of electronic fuse to BEL.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (15-12-2023)

HBL is the only supplier to BEL for electronic fuze.

Skipper Ltd., (Power and Water) a moat in making? (15-12-2023)

reiterated where? in an interview? if yes can you please provide link