Hi Hitesh, what’s your view on Gujarat Fluorochemicals?

Posts tagged Value Pickr

Sundaram Clayton (14-12-2023)

Not necessary to have some business of its own, it can show the dividends, sales of subsidiaries as w.r.t it’s holding… I guess. there are these two kinds 1) just act as hold co examples maharastra scooters, bajaj Holdings, Ujjivan Financials the other examples likes of Kama Holdings, Hercular Hoists etc.

Cineline India – Picture abhi baaki hai (14-12-2023)

Was able to speak to a gentleman who works in Multiscreen exhibition.

per him, “fully fitout and tied up” means its mostly plug and play excluding equipment , some movable furniture for food and beverage. he mentioned Rs2.5cr is an estimated total capital needed per screen including everything (quote “starting from 4 bare walled structure”), so the commentary from the management that its model is based on “fully fitout and tied up” and spend Rs2.5 cr per screen on top of it not consistent with competitors. He thought, “from here bringing up another 150 screens in another 1,5 years in a profitable manner, seems like stretched “

He being from the industry doubted if they have 160 screens already operating, he suggested to do a bit of research to confirm screens they have disclosed as operating, also suggestion was to speak to the owners of the properties if the rents were paid as agreed and on time.

The general caution was , when there is a large player, (PVR_INOX), distributors will have pressure from large player not to release on screens of smaller player. He said it can be big risk.

Glenmark Life Sciences (14-12-2023)

Very difficult to predict the future.

But you need to categorize these businesses like pure play CDMO, branded / unbranded generics etc.

And the below approximate criteria (shared by Aditya Khemka on one of the Twitter spaces.) you can use to value them.

Hope this helps

dr.vikas

Rural Elect Corp (14-12-2023)

After having taken investment positions in PSU pack two-3 years back & tracking the performance of these stocks thereafter , my take as follows, though there are conflicting views from different analyst on PSU stocks.

The PSU stocks especially railway , defence, renewables, (REC- PFC is a part of renewables) have undergone re-rating substantially and may further continue to do so wherever there is a scope if the govt policy such as heavy capex in infra project, railway , defence capex and Atma Nirbhar Bharat scheme continues . The other reasons for re-rating may be as follows as per my views

Have you heard of any PSU

(1) where CFO of a PSU resigning or any auditors resigning ?

(2) Any manipulation of balance sheet ?

(3) Diverting fund by promoter to other unrelated areas or related party transaction ?

(4) Promoter share pledging ?

(5) with worries such as USFDA compliance such as in pharma ?

(6) Not paying a substantial dividend consistently every year – though the amount may vary – The Govt holds majority stake and they need money in terms of dividend from PSU

(7)facing Income tax raid or GST raid ?

(8) Promoter entity Caught with insider trading

(9) working capital issue or fund raising issue from domestic/international market- All agencies are ready to lend to the Govt with most convenient rates?

(10) Not getting enough order from its customers ? Well, in most cases, the Govt is the customer and so the order book is healthy as of date is full for next 4-8 years.

If any of the above happens to a listed pvt stock which keep happening every now and then , the market becomes nervous and the stock price crashes.

The risks i could see in PSU stocks:

(1) If the govt changes its current policy as mentioned in 2nd para of this post

(2) The Govt is a majority share holder of most of the PSU’s. At times, They may take decisions which may not be in interest of minority share holders,

(3) OFS is frequent and normally they sell at a discount of 8-10% every time. Good thing is that they first give a hint in social media and after few days or a month or so, they declare OFS But then after having faced 2-3 OFS , i have found that the stocks have bounced back.It could be seen as a blessings in disguise as many institutional investors are on-boarded and the minority share holders gradually become majority and they can counter any decision by govt if it is not favourable to the shareholders.

Discl: Remain fully invested in a pack of Railway , Defence , renewables since last two years.

It is not a buy or sell recommendation in PSU stocks . Please apply due diligence before investing

Hazoor Multi Projects Limited (14-12-2023)

It’s just I don’t know how will we execute stoploss based order if the stock hits lower circuit.

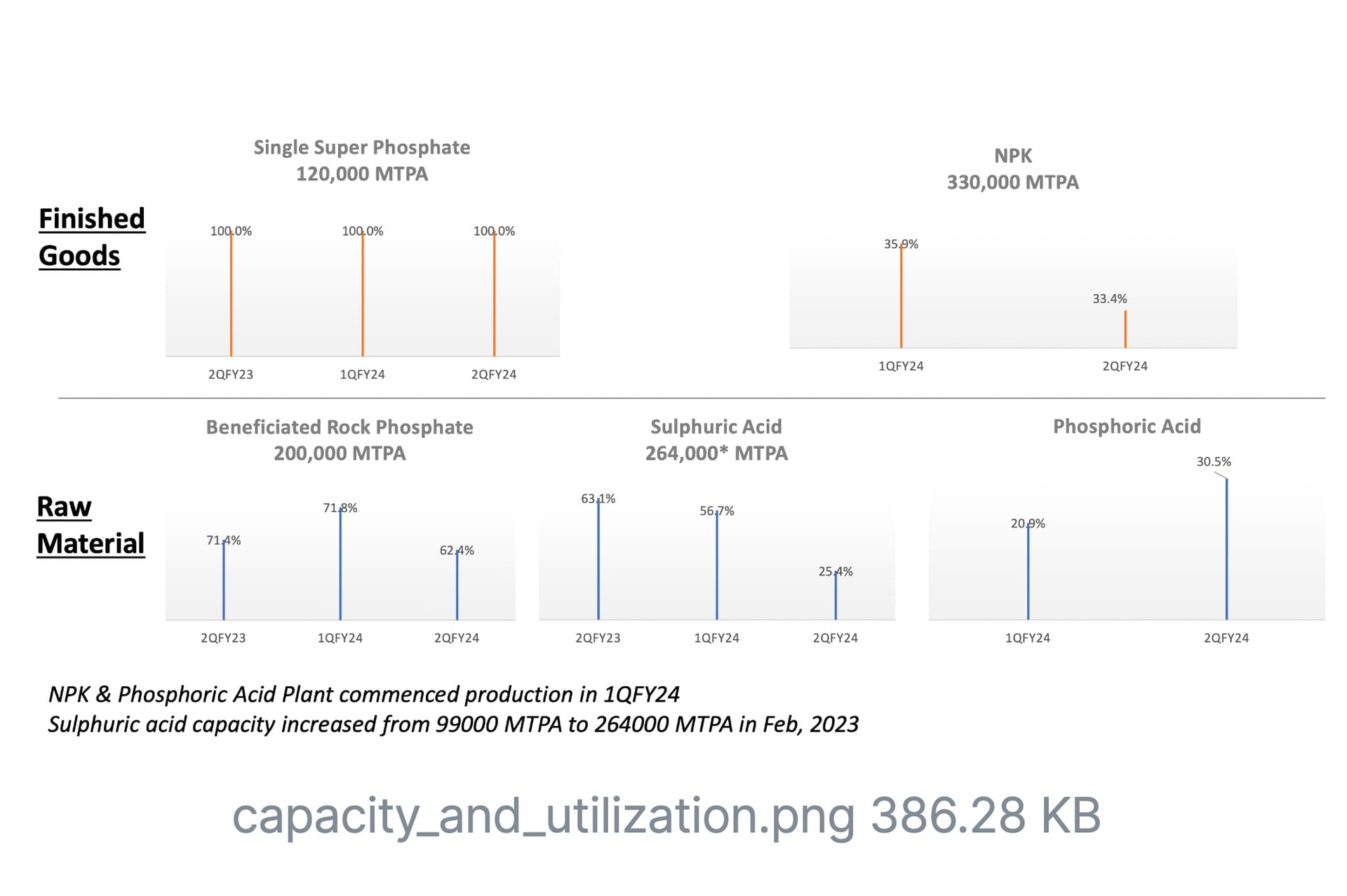

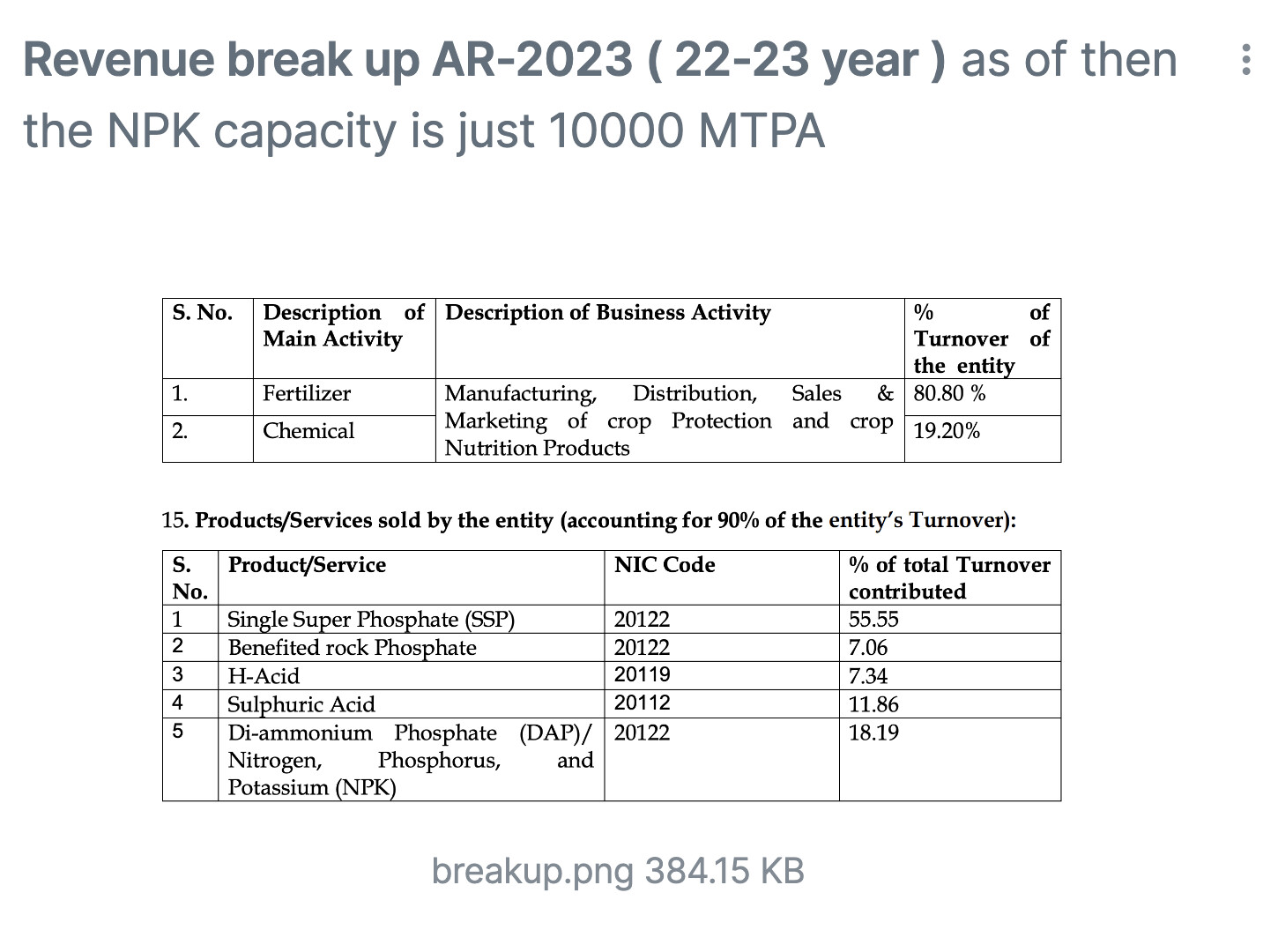

Krishana Phoschem ltd – Agro – Based Multibagger? (14-12-2023)

Recent analysis

Fundamental analysis

Last year revenue break up

.

.

Revenue Growth factors

.

The NPK/DPT utilisation levels far from full (33% ) if increased to 80% the profit will increase 100 CR annually which is a minimum rough estimate

Cost production : 18000 / ton

Selling price : 25000 / ton

(Rs. 25,000/ton – Rs. 18,000/ton) * 300,000 MT * (80% utilization) = Rs. 168 crore

.

Last quarter profit at ( 19 crores )

.

Macro economic factors

1.Russia resumes fertilizer trade with United States, ends discounts prices ( discount wast 80$ per MT ) to India ( Which will reduce imports to india, Currently Krishana does’t have any export business )

2.Union Cabinet approves NPK fertiliser subsidy for 2023-24 rabi season ( There won’t be any drop in demand and price reduction at least until the 2024 election, Currently NPK is sold at 1350 MRP per 50KG which is fixed price)

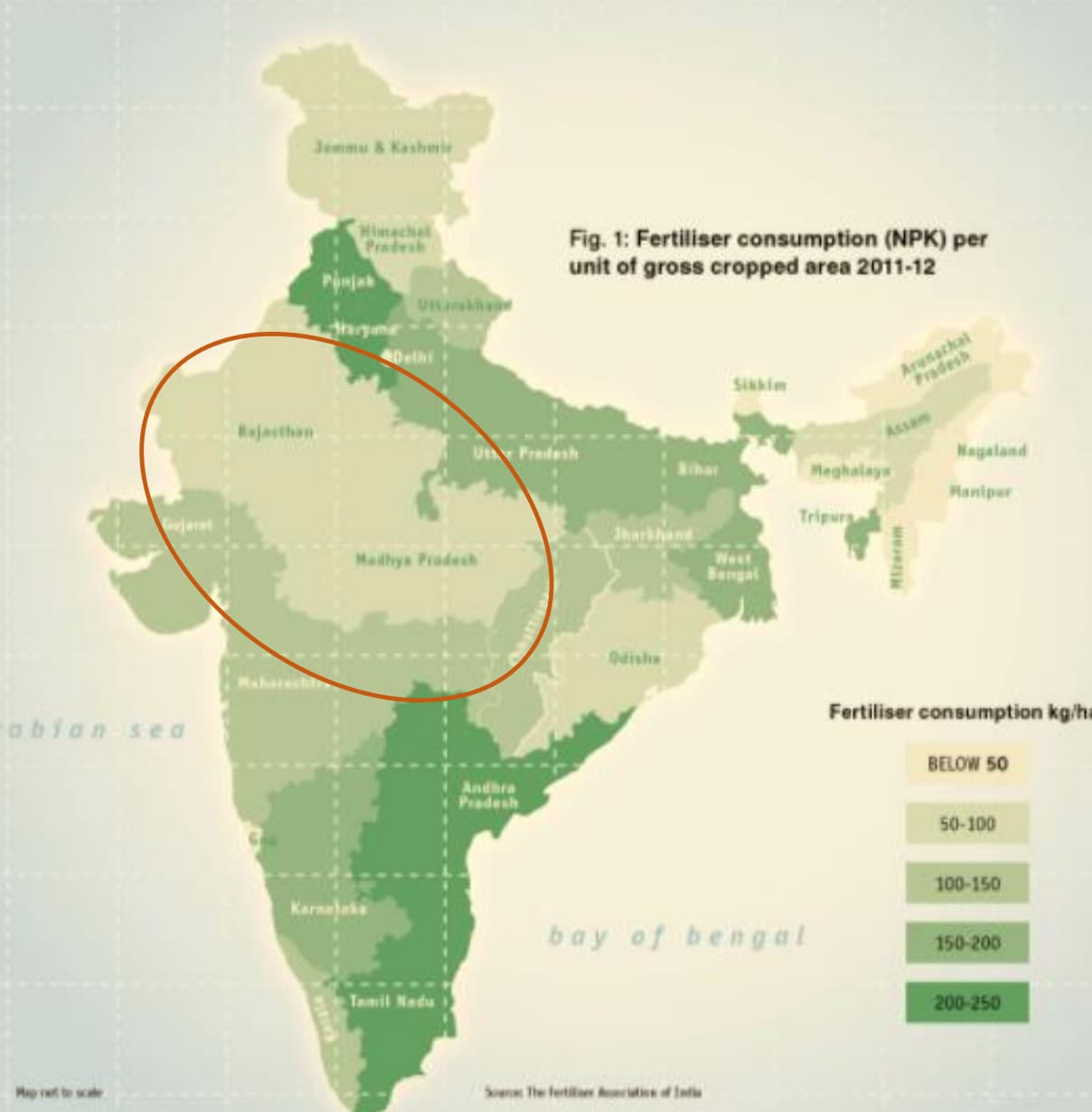

3. Fertilizer consumption in their major operating regions is very low ( as of 2022 ) there is room for growth there

.

Non-determinable Positive factors

Lot of insider trade activities by promoters ( Buying from market )

OSTWAL PHOSCHEM ( INDIA) LIMITED => Increased ownership From 64% to 65.43%

.

Nirmala Realinfrastructure Pvt Ltd bought 0.5% ( 5 crores )** at average price around 225 between past 5 months ( Owned by son of ostwal group). They have sold their significant amout of shares madhya bharat agro company,

RAJENDRA PRASAD OSTWAL => director of Nirmala Realinfrastructure Pvt Ltd ( Increased From 200 shares to 8900 shares)

.

NITU JAIN => ( mentioned as ostwal Group director in linkedin, but not sure ) ( increased from 5000 – 18000 => 30 lacks )

EKTA JAIN => Increased from (60000 to 66000 )

Pankaj Ostwal => son of ostwal group ( increased from 5000 shares to 8500 ) avg price 230

Ashok Kumar Parakh => from ( Increased from 5000 – 9000 shares ) at 225 price

Possible Negative factors

1.Adverse impact of any regulatory/policy change ( reduction in subsidy will lead to lower demand ). ( Reduction in MRP price of fertilisers, fixed at 1350 for NPK )

2.Raw materials are imported from JORDON for Rock Phosphate with long term agreement ( Any geo political factors will affect import )

.

Technical analysis

Trading at higher than 5Y Median of 25 PE, Currently trading at 33 PE ( Based on recent quarter EPS trading at 18 PE )

On balance volume is steadily growing

.

Disclosure : Not invested,

Kitex Garments Limited (14-12-2023)

i think Kitex should now show some good numbers as Powell announced rate cuts in US in coming year and may rally from here…

Rajesh Exports: Time to examine this story seriously? (14-12-2023)

I remember reading a Covid time financial dispute with Canara bank? Felt it was a genuine disagreement due to an unexpected extraneous factor and the company had deposited a large amount till adjudication.

I have a small stake in my high risk portfolio (was a mistake and i ignored the obvious red flags on corp governance.) But staying out as my bet was on Valcambi, which has signed a JV with a Middle east conglomerate. The deal ia controversial but may bump up turnover by 10%.

Burger King ~ Whopper of an Opportunity (14-12-2023)

(post deleted by author)