Any impact post this?

Posts tagged Value Pickr

IRFC – A Zero NPA NBFC (10-12-2023)

Yes from Screener.in

HDFC Asset Management Company (10-12-2023)

This should not be a concern I guess as it’s a financial investment for LIC and not strategic

With so many projections of sensex hitting 84,000 to 1,00,000, if they were to come true, big AMCs will benefit with rise in AUM and profits

Indian Energy Exchange (IEX) (10-12-2023)

Sorry, that’s a typo from my side. To correct myself – In case of a MCO in place, all transactions occur on MCO while the role of IEX will be primarily not of price discovery but just collection of buy/sell bids.

I can comment on your a) and b) questions, may not be the answer. If MBED(Market Based Economic Dispatch) is implemented, in which case all power trading must happen via the power exchange. you can ignore all the reasons for moving towards exchanges like – “uncertainties on fuel supply side and pricing on one hand and push towards renewables and operations optimization”. In one fell swoop, this will move all power trading to happen via exchanges. And when this happens, there is one MCO who is the ‘sole exchange’ and several brokers like IEX, PXIL and HPX. With this surge in volumes, and way lesser uncertainty in terms of business regulations, there could be many more players who could be interested in entering the business.

About commanding higher multiples, exchanges always will command a higher multiple because there is a great room for innovation, they can come up with newer products, like derivatives for example which can add significantly to existing revenues. But here that would be the MCO and not IEX. IEX, as they say, is as of today NSE + Zerodha rolled into one but after MCO implementation it will become just like Zerodha and their success will be linked to things like how well they manage the commissions and UX(user Interface) rather than adding newer innovative products, and hence a lower multiple.

The reason I couldn’t form conviction to buy IEX is the number of uncertainties around it. Just take the MCO and MBED, you really cannot reliably build a bull or bear scenario without knowing if and when they will be implemented. Two many key variables in the equation.

Rudra portfolio (10-12-2023)

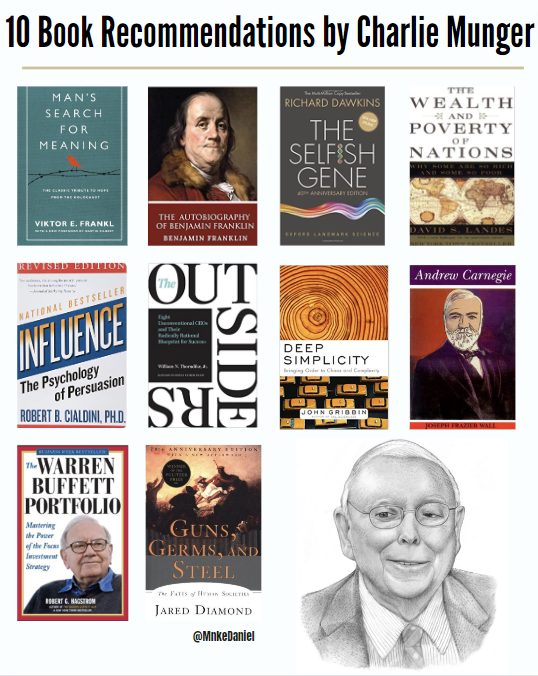

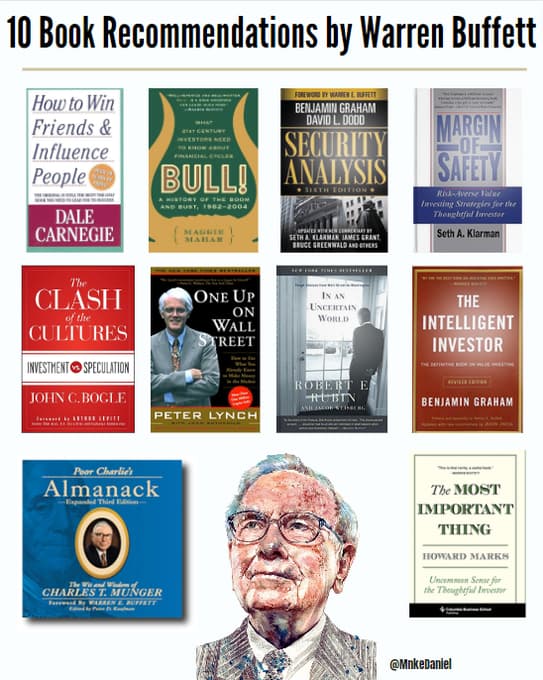

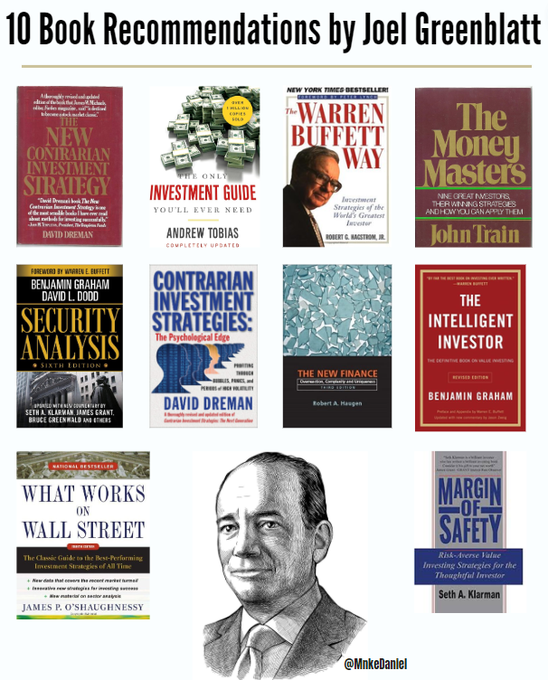

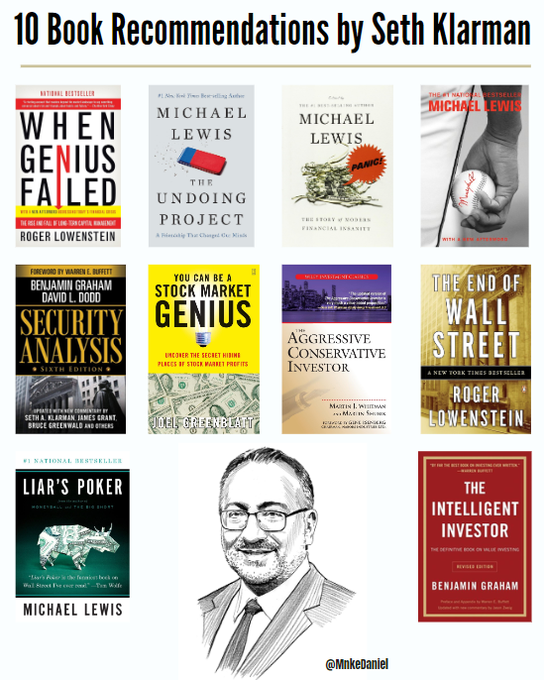

Top 10 Books to read from Famous Investors

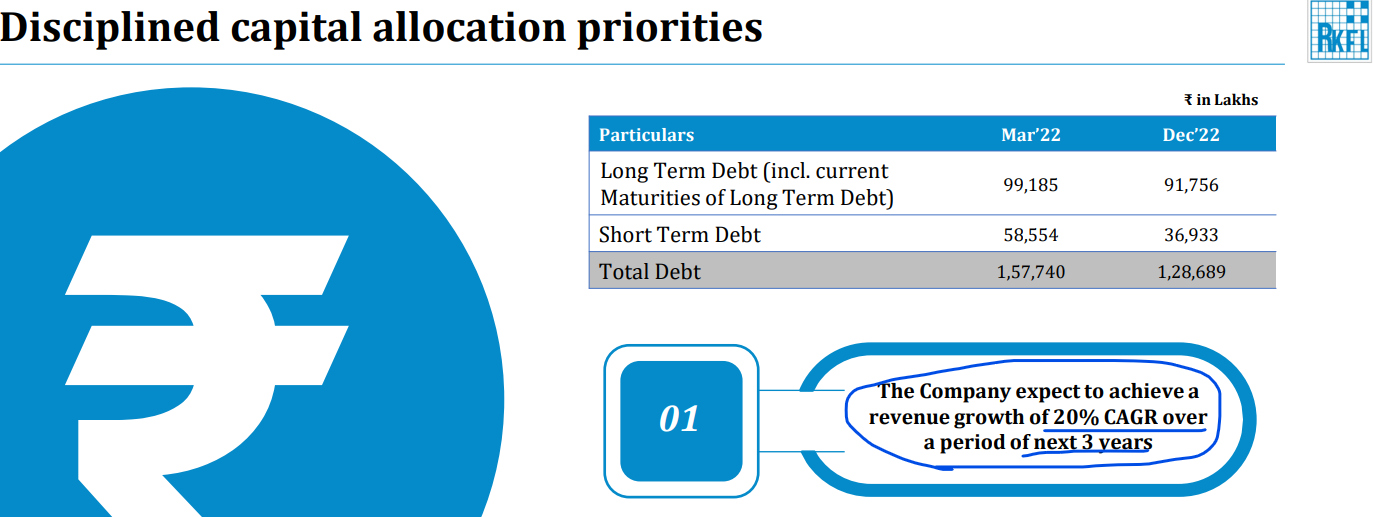

Companies with 20%+ growth guidance for next few years (10-12-2023)

Ramkrishna Forging in its investor presentation guiding for 20% growth for next 3 years. In the same presentation, they referring to their capacities being able to fetch the revenue of ~ 5,000 Cr. FY24 revenue seems to reach between 3,800-3,900 Cr.

Atirek portfolio (10-12-2023)

Neuland Reasons for buying

I looked at Neuland after Q4FY23 result but after current result only I got the conviction to buy as I was already having Syngene and I did not knew difference between two. Also the profit looked non repeatable. Syngene is in big pharma and Neuland is in biotech.

Also Niveshaay seems to have it in its portfolio. I don’t know when they added it.

ROCE and ROE improving

Syngene told about problems in biotech company being headwinds due to funding issue still neuland was able to double their phase 2 molecule counts

Industry structure

Pharma growing at 6 percent but CNS area growing faster at 8

Directly buying biotech company might seem risky but cms company helps by diversification

Crams growth in double digit

Biotech company seems to be coming with new drugs more commonly than big pharma

Rerating possible?

Yes, as it current Pe is less than 25

Growth

Many molecule in registration stage(takes 1-2 years to get commercialised)

Capex – Have announced the capex of 120 cr

Unutilised capacity of 3rd plant at 30%+.

Margin expansion

Yes, it is being seen in the last quarter Q2FY24

Debt

Debt is negligible

Negatives

-

Its revenue consists of developmental revenue and commercial revenue. Developmental revenue might be one time revenue. Need to check about sustainability of revenue.

-

Why is the reduction of the commercial molecules from Q2FY23 to Q2FY24 when we have never lost a customer?(Need to check)

-

How frequent is the situation where after going commercial with the molecule, the biotech firms with which we work change the suppliers due to any reasons like being acquired by big pharma, licensing deals with big pharma, due to constraint in capacity, etc. ? (Need to check)

-

Management selling 10 percent of the company in a company with low promoter ownership.

Tailwinds

-

Considering three months of revenue growth, it seems they might be getting recurring revenue. Also its cms manufactoring business has been growing month on month for few years now. In few years, things will become sustainable. (medium)

-

Mostly 5-6 molecules is contributing with new molecule contributing more and 1-2 molecule more is to be commercialised.(short)

-

Most of its molecules are in cns theraupaurtitic area which is supposed to grow by 8 percent cagr.(long)

-

No patent expiring till 2030(long)

MOAT

Not lost a client since inception in cms(q2 fy2024)

Shifting client is cumbersome in custom synthesis

Trust factor with innovator

Many patents granted for Neuland(more than 50 when compared to 100 for SRF)

Optionalities

KarXT comes with no side effects of currently mental diseases medicine( like schizophrenic, bipolar) like hand shaking, weight gain, muscles rigidity. It is revolutionary and the profits from commercial manufacturing of this medicine can make it bigger than any custom manufacturing companies.

Why pharma companies come to India as per Neuland?

-

Complex process

-

Source of material is in India

-

Cost of material

Screening criteria

Through unseen value.

GMM Pfaudler: A safe way to play the Pharma/Chemical cycle (10-12-2023)

Here is a summary based on the transcript of their Q2 FY24 earnings conference call:

- FY25 Guidance: The company is confident of achieving its FY25 guidance of revenue CAGR of 14% and EBITDA CAGR of 24% over FY22-FY25E.

- Market Leadership: The company intends to maintain its leadership position and increased profitability in its core glasslined equipment (GLE) business, which has a global market share of 40% to 50%.

- Diversification: The company is expanding its non-GLE and systems business by cross-selling opportunities and exploring new application areas in segments such as oil and gas, minerals and mining, lithium, etc.

- Innovation and M&A: The company remains focused on innovation and M&A to drive growth. It recently acquired MixPro, a mixing company based in Canada, to strengthen its global presence and product portfolio in the mixing business, which has a market size of $3 billion.

- Order Visibility: The company has an order backlog of INR 1,705 crores, which translates to about 6 months of order visibility in India and about 7 to 8 months in the international business. It also has a strong opportunity pipeline across all business platforms and expects some large projects to materialize in the coming quarters.

Sheela Foam – An exciting branded play (10-12-2023)

Here are some key takeaways from the Q2 FY24 earnings concall transcript of Sheela Foam mattresses:

- Revenue growth: The company reported a 22% year-on-year growth in revenue, driven by strong demand for mattresses and other comfort products. The company also gained market share in both organized and unorganized segments.

- Margin expansion: The company improved its EBITDA margin by 240 basis points year-on-year, mainly due to better product mix, operational efficiency, and cost optimization. The company also benefited from lower raw material prices and stable forex rates.

- New product launches: The company launched several new products in the quarter, such as Sleepwell Signature, Sleepwell Cocoon, Sleepwell Spinetech Air, and Sleepwell Feather Foam. The company also introduced a new brand, SleepX, to cater to the online and value segments.

- Outlook and guidance: The company is optimistic about the future prospects, as it expects the demand for mattresses and other comfort products to remain robust, driven by increasing awareness, urbanization, and disposable income. The company also expects to benefit from its strong distribution network, brand recall, and innovation capabilities. The company has guided for a 15% to 20% revenue growth and a 20% to 25% EBITDA growth for FY24.

- Kurl-on acquisition: The company has acquired 94.66% stake in Kurl-on Enterprises Ltd. at an equity valuation of Rs. 2,150 crore. The deal is expected to be completed by December 2023. The management expects significant synergies from the acquisition in terms of product portfolio, distribution network, manufacturing capacity, and cost savings. The combined entity will have a market share of more than 50% in India’s organised mattress space2.

- Furlenco acquisition: The company has acquired 35% stake in Furlenco, a furniture rental company, for Rs. 300 crore. The deal is expected to be completed by March 2024. The management believes that Furlenco is a disruptive player in the furniture industry, with a strong brand, loyal customer base, and scalable business model. [The company aims to leverage Furlenco’s online presence, data analytics, and design capabilities to expand its own product offerings and reach new customer segments]

Atirek portfolio (10-12-2023)

Kama holding

Earlier I ignored the SRF but now I think I have got few answers and also destocking seems to be bottoming out.

My answers

- Even after the patent is expired, innovator have process patent through SRF like companies which can keep the molecule margin high for 3-4 years more.

- The fluropolymer Capex is just near to 500 Cr and it has got delayed though they seem hopeful as per recent management meet. It is less than 20 percent of the capex. Then downside due to capex addition is limited.

- Size of the opportunity is looks high now as they seem to have entered the pharma custom synthesis which is huge.

Industry structure

Refrigent cagr – 7.9(fortune business) and 5% bloomberg

Flurochemicals – 5%

Fluropolymers – 5.2(fortune business)

Nearly 30 percent revenue is contract based whose margin are non fluctuating

Debt

Debt is Low and manageable

Growth

Huge capex majorly in custom synthesis and chemicals

Dividend opportunity will be high in Kama holdings

Product mix change towards high margin and stable margin products like agrochemicals custom synthesis and chemicals

Rerating

Chances of rerating is high as promoter needs to earn money and hence kama holdings discount will narrow

Margin expansion

Not there in short term as capacity is being commissioned(3 – 4 years)

Tailwinds

Capex and more than doubling of net block. (Long term)

Entry into floropolymers(Long)

Entry into pharma cms(long)

PI industries receivable has increased with good sales in Q2 FY24 and SRF has delayed the shipment. Q3 might be better as SRF has more stringent revenue recognition than PI industries(short)

After the inventory destocking stops, it margin might revert as its chemicals product are not too much dependent upon china. (Medium)

Moat

Patents in agrochemicals

Cow lost advantage in refrigerant

Negatives

Industry growth is single digit

Not sure when old agrochemicals molecule will expire(Process patent is there after the patent gets expire)

Not sure whether the process is PFOS free(yes it is as per the management meet notes)

Gujurat florochemicals have capitive mines but SRF does not have it, therefore may face margin pressure from Gujurat flourochemicals in flouropolymers. China has stopped procuring the fluorspar from their mines and hence it bring it on equal playing fields.

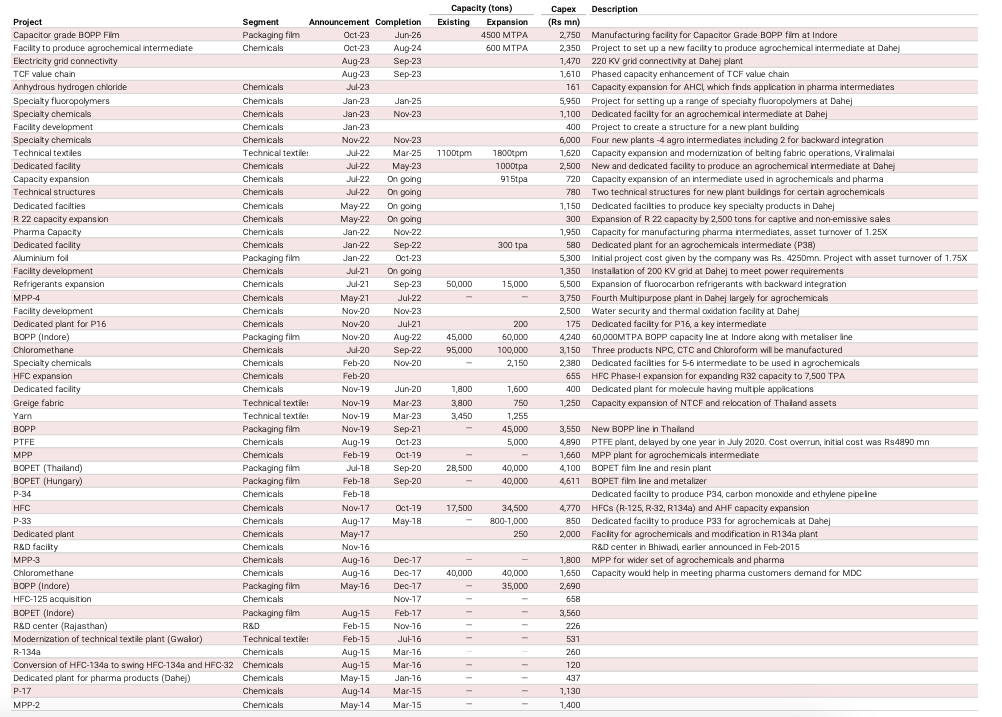

Upcoming Capex and past capex

Source Kotak