Looking back, the company reached its peak valuation and margin in 2018-2019. Presently, it faces its lowest margin, with raw material costs rising from 50-55% in 2019 to 62% now . A softening in raw material prices might boost the margin to 12-15%, especially given the substantial increase in revenue, indicating customer retention. The current valuation appears cheap, might remain like this unless execution improves on margin front.

Posts tagged Value Pickr

Buy Unlisted Shares (03-12-2023)

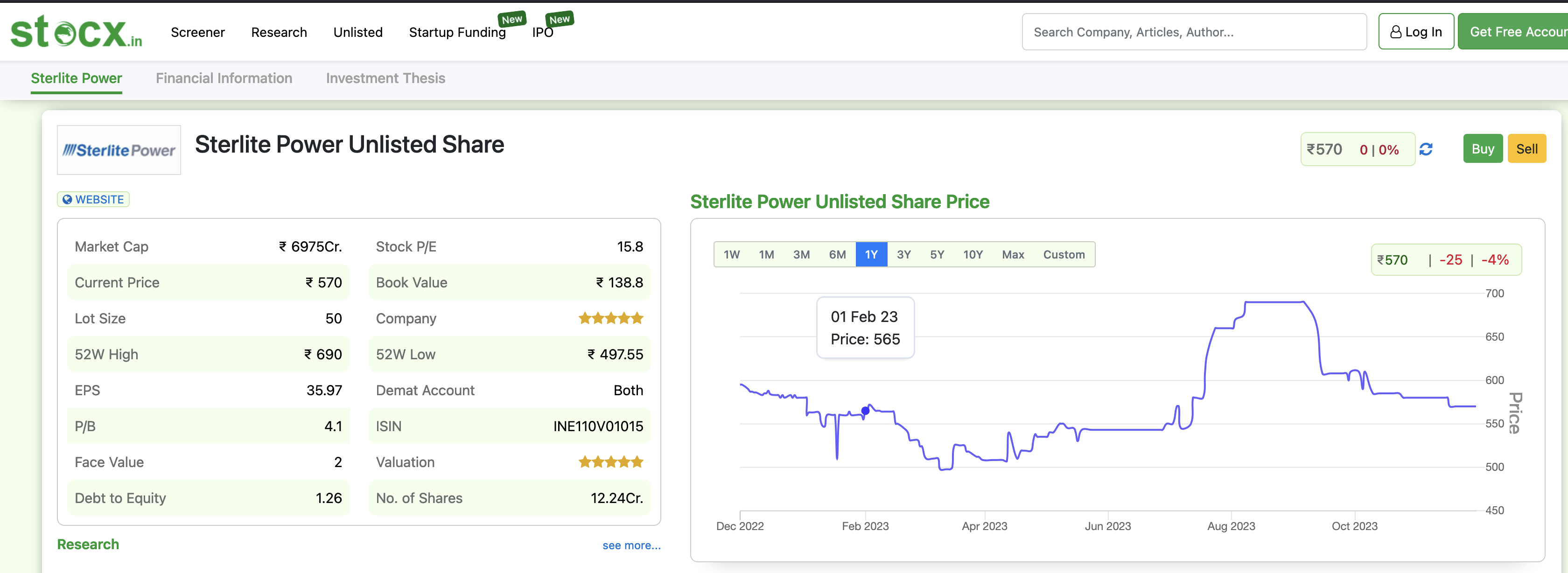

Hi, thanks for looking into it. From where did you check the P/E?

This is the data I am referring to and it seems 15.8

Buy Unlisted Shares (03-12-2023)

At P/E of 198.5, it seems overprized to me. My strategies are often simplistic, but with some many power companies available cheaper, I should need a strong reason to look at it.

Buy Unlisted Shares (03-12-2023)

I sold Studds accesories after poor results in Altius recently. They guided through the process of transfer authorisation in MyEasi CDSL. Money was transferred after 2 days.

Buy Unlisted Shares (03-12-2023)

What is your view on Sterlite Power unlisted shares?

One of it’s business is going to demerge, and they have to do IPO of that entity for value unlocking.

GMP has gone down from Septermber levels

Buy Unlisted Shares (03-12-2023)

I have pinged Nuvama and altius as suggested…Unlistedzone is where i did all my transactions, But they seem not to interested in business now…

Altius is working on getting me some polymatech… Will decide basis their support…

Hope your entire experience was good in altius

Galaxy Bearings (03-12-2023)

If Anybody’s active in this Thread i had several Question

Recently i started Learning about this company

- the capex is of 35 crores post to which the company will have the capacity of more than 9.5 Million bearings P.a. the capex is to be completed by the end of this year. SO anytime line regarding the capacity utilization schedule? Since 4x of original capacity means that the Depreciation will start to hit the P&L Statement as soon as the product is put to use but the Revenue will Build up steadily

- Who are their Export clients? since majority of their revenue is Export oriented and i saw they are exporting it to Italy and Germany, but in current scenario there is Import duty on European OEM if they import from India (around 10%). In last 2 AGM i didn’t hear anything about the same. how did they stay put if the product of there’s becomes Expensive? Any Measure since the margin are more or less Stable

- If I Understand correctly the money parked in Mutual Funds are for CAPEX, Since the capex money is required in next 6-12 months wasn’t the prudent strategy to keep it in Liquid Fund. Does any body find the management Risk Averse?

- What is causing such Huge capex? I understand correctly that the structure of Industry is such that there is not Above hand Orders but still is there management Rationale behind the same.?

- The cash generation ability of the company is very poor. In AGM one of the participant asked the question on this line and the answer was Quite fluke by the management.

Anybody has any idea regarding the above questions then will be Great

Thanks

Syngene International (03-12-2023)

KMPs including CEO are selling Syngene in big quantity in last few months

How we as retail investors should view this development, considering that the captain of ship knows best what is happening around.

Marksans Pharma- Can it be the next Pharma Biggie? (03-12-2023)

Regulatory inspections have become once again a major concern for Indian pharma companies. Marksans seems to be doing well on that front. There was a PADE inspection at Marksan’s Goa facility and had two observations. Seems like minor issues as the company mentioned in August concall. Also, the company has successful USFDA inspection at it Time caps facility without any observations and German health authorities also had an inspection of its Teva facility with no major observations.

The company has been able to improve its sales continuously over the past many quarters and is expected to continue to do so in the future with the new facility contributing.

Gross margins have also improved with freight and raw material prices coming down.

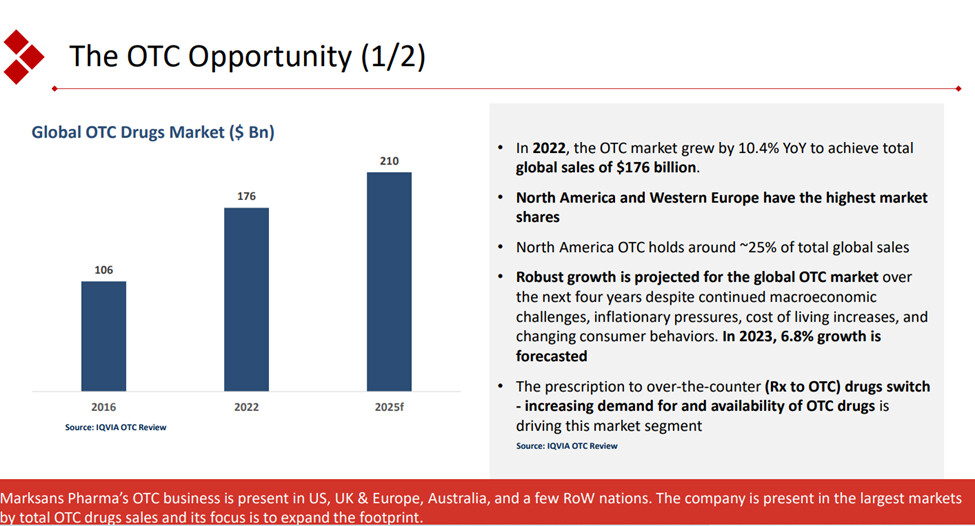

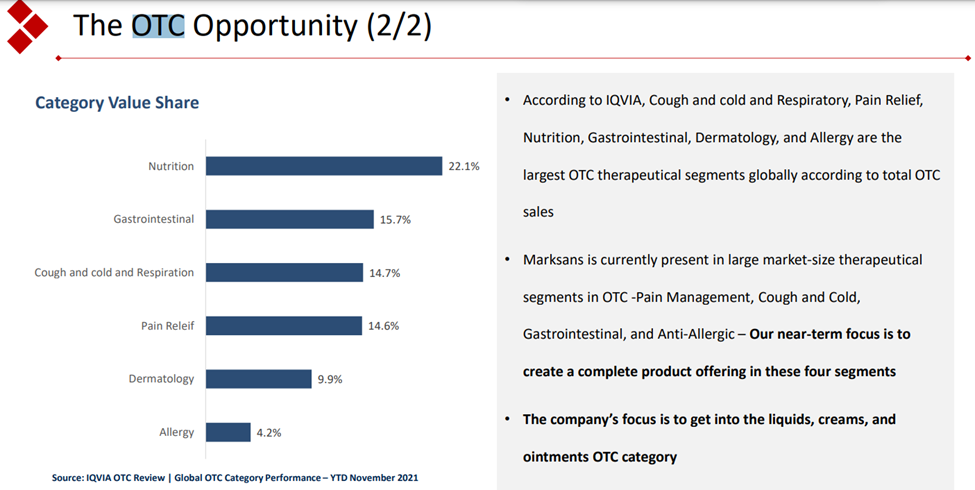

The company seems to be focussing on the OTC opportunity. OTC contributed 74 % of the revenue as of FY23. The company has illustrated the prospects of OTC pharma market in the presentation.

This focus of the company seems to be the differentiating factor for the company. The company so far has been able to capitalize on this Rx to OTC switch. The company is also planning to integrate backward to API for major molecules which could expand margins. They are yet to file DMF for these molecules. The deal for a frontline marketing pharma company in the EU still seems to be elusive. The company has a cash of 668 cr on the balance sheet. Would be interesting to see how they plan to utilise the funds.

Have plans to increase their R & D exp from 1.6 % of sales to 4 – 5 %.