I cant get over this point. To emphasise again – in last 10 years company has improved working capital cycle every year. Company has also improved ebidta margins every year in last 10 years except in FY17. I havent found any listed company who has done that. “Samaz main nahi aa raha hai – rear view mirror dekhu ya aage windshield dekhu”. The confusion arises yet again.

But I need to be honest with myself. I really dont understand the “what” has driven this achievement. What makes franchise so strong ? And therefore – cant go beyond 3-4% allocation

Posts tagged Value Pickr

Omkar’s Portfolio Analysis and Discussion (25-11-2023)

Pricol limited – OEM automotive (25-11-2023)

Pricol limited Q2 fy24 concall notes:

-

Financials

- Revenue (in crores):

- Q2 fy24 582 (yoy growth of 12.8% & qoq growth of 7.8%)

- Q2 fy23 516

- Q1 fy24 540

- H2 fy24 1122 (yoy h1 growth of 16.5%)

- H1 fy23 963

- Net profit:

- Q2 fy24 33 (yoy numbers not comparable due to very less tax rate last year, qoq growth of 3.8%)

- Q2 fy23 48

- Q1 fy24 32

- H2 fy24 65

- H1 fy23 68

- Impact of FAME subsidy issues on EV sales in the first half of fy24. Though the volume is less (about 7-8%), the value is higher due to higher kit value in EV sales. This should stabilize going forward, seeing positive traction in October sales.

- Revenue (in crores):

-

Revenue distribution

- 65% from driver information systems and connected vehicle solutions(DISCVS). 35% from actuation, control and fluid management systems(ACFMS). This will be more or less going forward (+/-2%).

- With in DISCVS:

- Around 65% from two wheelers

- 20-25%% from commercial vehicles

- Remaining from four wheeler passenger vehicles

- Share of new products in overall sales is about 20%.

- This should go up slightly higher in fy25/26 as they are launching new disc brakes and other products.

-

Capex

- 600 crores of capex planned in the next couple of years starting last year. About 150 crores was spent last year, about 200 crores is being spent this year, and another 200 crores would be spent in the next fiscal year. This is to enhance capacities, improve productivity and also going for modernization of some of the older plants. This will take our revenue up to about 3,800 to 4,000 crores.

- Pricol has made key investments in Surface-mount technology (SMT) for printed circuit board (PCB) Assembly Line and Disc Brake assembly lines.

-

Guidance

- Company guiding for 4000 crores of revenue by fy26. 3600 crores by organic growth and 400 crores of revenue by inorganic growth.

- H1 growth was around 16%, expecting a similar range in fy24.

- In a capex related question management does mention that they are looking for inorganic growth as well if something exciting comes up.

-

Margins

- EBITDA margin guidance of around 13.5% in next couple of years with an increase of 0.3-0.4% every quarter. This should happen before Q4 fy26. Current margins: Q2 fy24 12.42% vs Q2 fy23 12.97% and H1 fy24 12.57% vs H1 fy23 13.01%.

- Margins generally higher in ACFMS export products.

-

Kit value

- Two wheelers kit value has evolved from 300 to the current value of 1200. Expecting it to reach about 2500 in the next 3 years.

- Four wheeler passenger vehicles, still a nascent stage. Commercial vehicles this number is much bigger.

- ACFMS vertical, they were moving from small value oil pumps and chain tensioners to more complex BLDC fuel pump, electrical coolant pump, and other products which are more towards the Rs. 1,000 mark as against what we were supplying at Rs. 150 and Rs. 200.

- 8/10 EV two wheelers use TFTs from Pricol. Four wheeler is still at a nascent stage.

-

MoUs

- Signed MoU with BMS powersafe to produce battery management systems for the Indian market.

- Signed MoU with Sibros for Connected Vehicle suite of solution, for which trials have already started for the proof of concept ideas with at least 10 vehicle makers.

- Management expects revenues for these products will start flowing down from fy26. 4000 crores guidance is based on the current order book and does not include revenues from these MoUs.

- They also signed an agreement with TYW based in China for the advanced display information systems for the Indian market. More details of this are expected in coming quarters.

-

Ownership

- Minda corp has acquired a stake of 15.7% in the company through open market purchase. In response to this, management has increased stake by 2% in Q1 fy24. Overall management is owning 41% (including extended family members) and if need rises they would like to increase this further.

-

MIscellaneous

- Other expenses to be in range of around 42 crores going forward (in line with inflation)

-

Things to look for in the coming quarters:

- Improvement in EBITDA margins (they are a bit lower compared to last year numbers as against management commentary of this going up)

- EV sales pick up in coming quarters

- Minda corp stake increase related issues

- An eye on the growth as this year it seems to be doing less than what is required to reach fy26 target.

-

Disclosure: Got interested and started buying after Minda corp bought the shares from the open market. Currently forms about 3.7% of the overall portfolio. Will continue to add it in the coming days. Not an expert of valuation, the goal is to buy good companies to hold for the long term as long as the underlying business is performing.

Portfolio of a novice investor (25-11-2023)

Formula used for this?

Omkar’s Portfolio Analysis and Discussion (25-11-2023)

Also, from FY 14 to FY 23 – company has improved margins and working capital cycle every year except 1. And in all likelihood FY 24 will see improvement in both parameters over FY23. I am not sure any other company in the listed universe has achieved something like this

Iris Business Services – Emerging SAAS Microcap (25-11-2023)

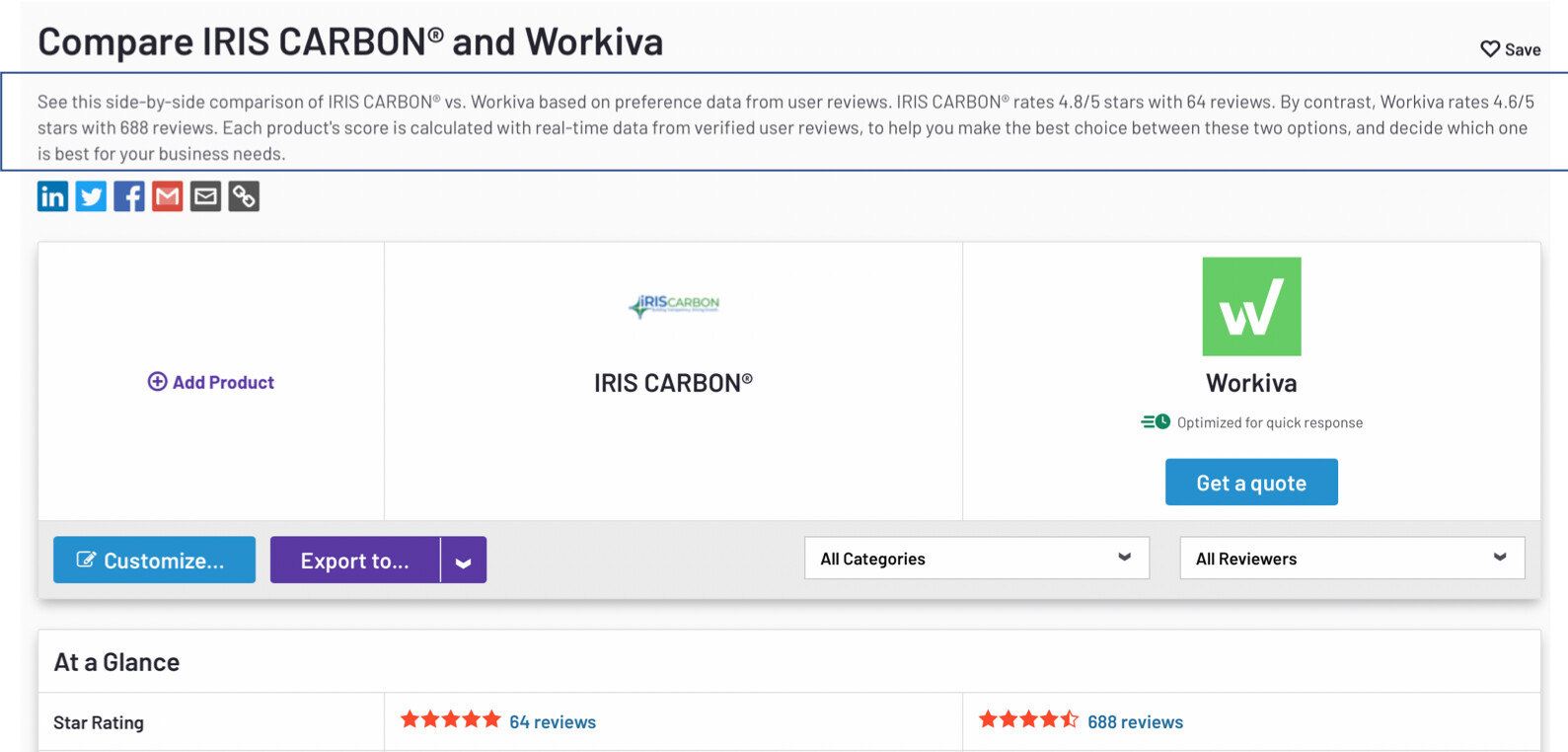

I tried to check this statement out from the CEO and he does seem to have a point. I was quite surprised by the vast gap in the way Workiva is valued on the NYSE and between the Iris valuation here. Just for context:-

- Workiva (Workiva | Software for ESG, Audit & Risk and Financial Reporting) is valued at ~5.1 Bn USD today, whilst guidance for FY 23 revenue is ~USD 627-628 million

This means that Workiva is being valued at >8x sales, 1 year forward, more in line with SAAS company Rategain (~10x sales). Even after the recent run-up, Iris is still quoting at 3.2x sales.

Big differences : Iris is profitable whilst Workiva is loss making. Iris is miniscule as compared to the established Workiva though.

- Workiva is a giant in the business, but still growing fast. This does show that the TAM could be large for Iris, and at the same time, competition is strong. Could Iris be the price competitive Indian alternative? I found this review especially interesting

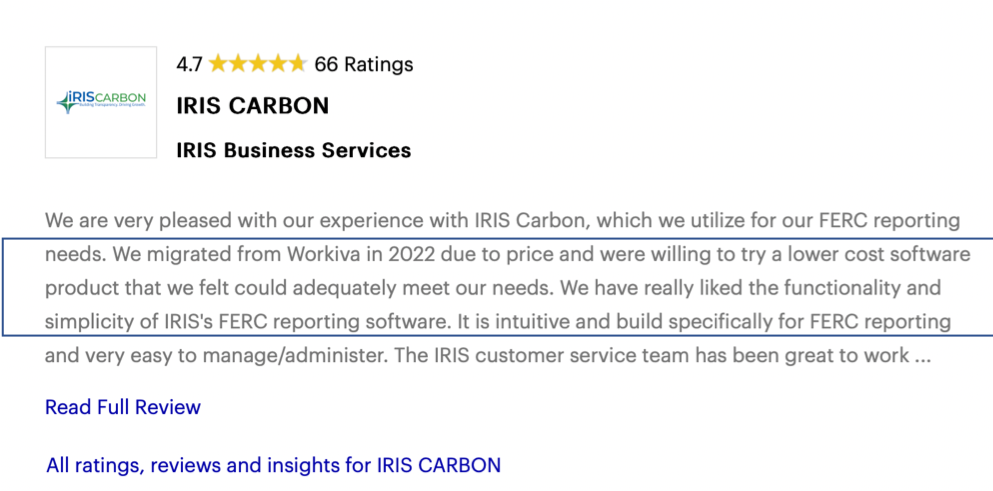

- Iris Carbon has some really good ratings on G2review which looks promising, at 4.8 is slightly better than Workiva at 4.6. But we need to understand that Workiva has a much wider review base, and also I have a feeling could be the better product being so much larger in terms of revenue.

Disclosure : I am invested in self and family accounts and am biased. I have made transactions in the stock in the last 30 days. I am not a SEBI registered advisor, not an expert and this is not investment advice.

Omkar’s Portfolio Analysis and Discussion (25-11-2023)

Abbott India

Abbott india, keeps proving me wrong. First half – 24 operational revenue growth is 11% ( ajanta H1 sales growth – 8%, Eris – 13%, Mankind – 15%, in that domestic business growth is 11% for mankind) and EPS growth is 28% ( ajanta H1 eps growth – 24%, Eris – flat, Mankind – 39%)

Most astonishing part remains cash flow generation. H1 CFO increased by whooping 83% to 683 Cr from 370 cr H1 last year . 2 years back their yearly CFO was 727 Cr ( for FY 21 )

The reason for lower allocation is inability to understand the leverage business model has. Every year I keep thinking margins and cash flows are peaked but company keeps proving me wrong. Fy24 ROE will be around 35%

Manappuram Finance (25-11-2023)

Major reason for lower opex in Muthoot is their AUM per branch which is very high compared to any gold financier. Muthoot has a per branch AUM of 14.2 cr, whereas Manappuram has 5.6 cr, IIFL has 8.8 cr, FedFina has 7.1 cr. I don’t know how Muthoot is able to do that. Even if I assume they have bigger branches compared to other players, their employee expenditure is proportionally low compared to other players, which signifies they do better in all parameters.

Smallcap momentum portfolio (25-11-2023)

Has it been documented/proven that one stock selection criterion is superior over the other for such a quant assortment? ATH/Volume action/Gainers list over multiple time periods/quarterly results etc

Do we know which screening criterion is the best?

HDFC Life Insurance Company (25-11-2023)

How do you find the economic moat of hdfc life in comparison with the other insurance players.

Smallcap momentum portfolio (25-11-2023)

Hello Viswanath

Thank you for starting this thread. I’m really interested in rule based investing/trading but I haven’t done any consistent effort on this side.

However I’d like to track the progress you make and how your portfolio turns out. I’d very much appreciate if you can keep updating this thread at a frequency of your choice. I have a few observations

The returns over 1 years are 40% where as the whole Nifty Smallcap index itself is up 36%. That’s 4% extra return and if one can get this consistently that’s a great outcome as per me. However the effect of fees and charges may eat into the returns you make

Let me ask a few questions

- How many stocks goes out of the portfolio evey week (rough estimate) ?

- How do you track the returns over 6 months and 12 months. Is this data readily available on any website ?

- From your broker you can see the total charges you’ve paid in a period ( may be one year). Could you check this and update what percentage of your portfolio went into charges ?

Questions on the strategy

- Is there any specific reason for selecting this index ? and also for selecting average of 6 month and 1 year average returns ?

- What percentage of your equity portfolio is invested in this momentum strategy ?

- Do you have any stop loss or do you exit only at the end of each week if necessary ?

Thanks

Praveen