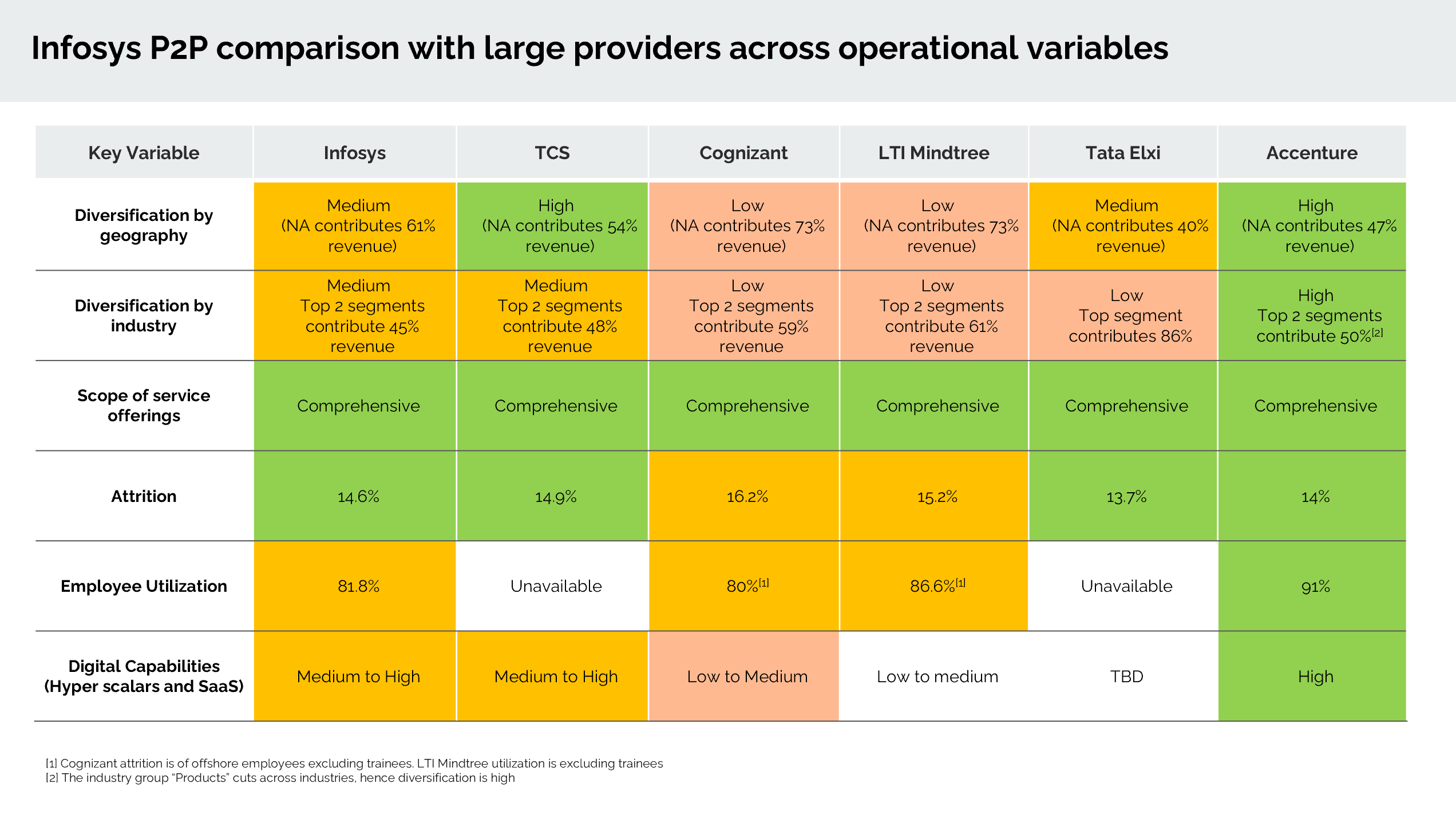

In case of diversification by industry, even though Accenture top 2 segments are contributing to 50% still diversification is shown high in green, while in case of Infosys and TCS , top 2 are contributing 48% and 45% , still their diversification is medium…how come? Or I am reading in wrong manner?

Posts tagged Value Pickr

Infosys Limited – Are we getting a discount or no? (17-11-2023)

Sure, here you go.

Operational parameters

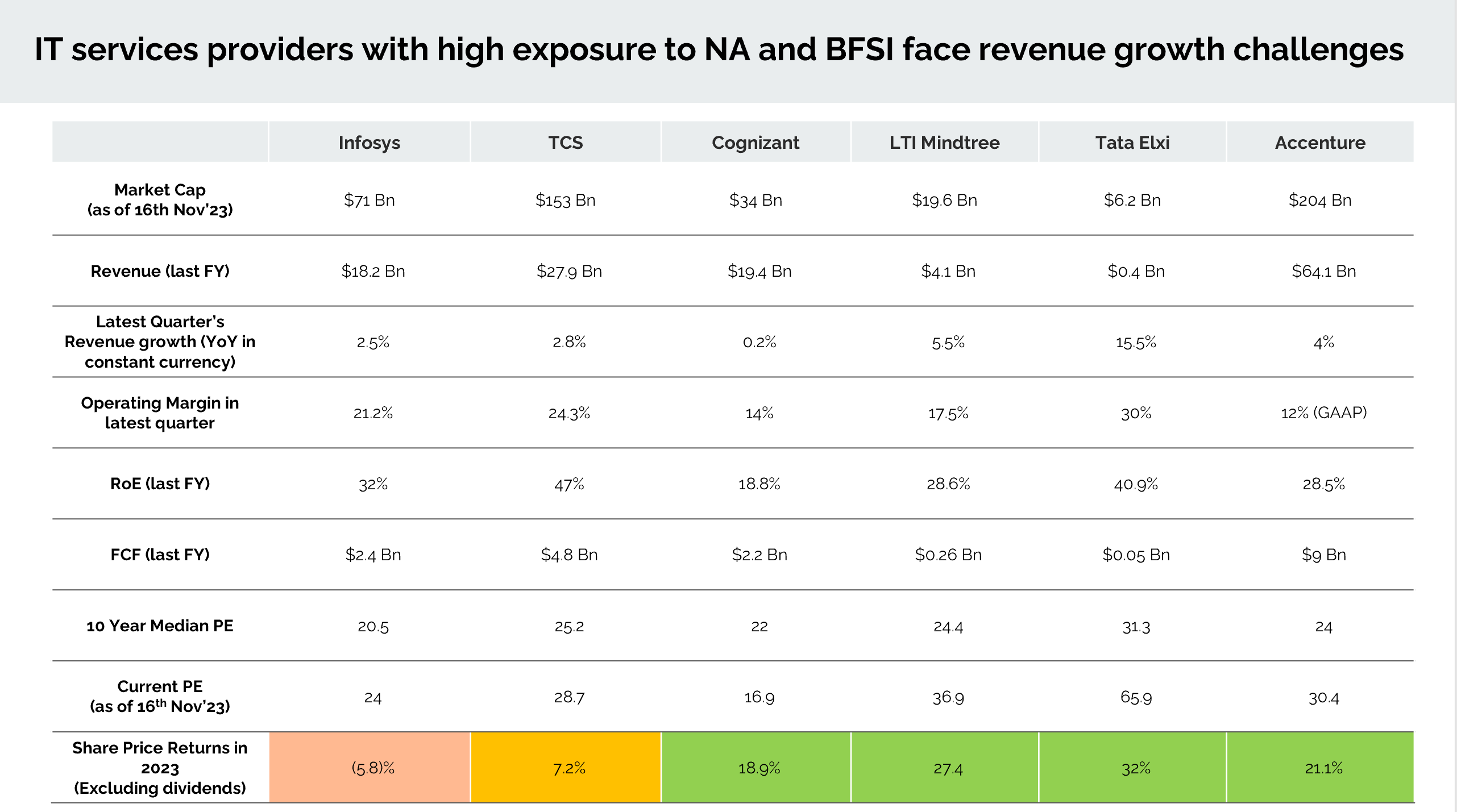

Numbers

Cheers!

Mahesh

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

Where can I find buyback yield of Nifty50/Sensex (preferably) or of its constitutents?

I am calculating of Equity Risk Premium using total return on constituent of Nifty50/Sensex Index. For this I need dividend yield and buyback yield; I can calculate average dividend yield from TRI version of Nifty50 but where will I get buyback yield for Nifty50/Sensex on average or its constituent stocks?

Semiconductor world – CPU/GPU Wars (17-11-2023)

Regarding point 5. Note that it is enabled by arm neoverse (compute subsystem aka a boilerplate platform).

The basic idea is that Arm is providing not just the Core and fabric IP, but also ready-built IP blocks of many cores. The key building block Arm showed during that announcement was a 64-core IP block arranged in dual core compute tiles.

Arm is enabling CSPs to ‘backward integrate’ like apple did with its silicon.

H.G. Infra Engineering Ltd : Paving the Path to Success (17-11-2023)

Q2 FY24 Concall Notes

Introduction and Current Scenario

- Slow NHAI tendering until September ’23 due to prolonged monsoon.

- Recent acceleration in bidding process and internal changes.

- Anticipation of increased bidding activity in the next 4-5 months.

Diversification Strategy

- Focus on diversifying orders in various sectors.

- Opportunities identified in railways, metro, and water sectors.

Railway Sector Opportunities

- Participation in the Amrit Bharat Railway Station Scheme for station revitalization.

- Bidding for railway projects totaling Rs. 1000 crores, with plans for additional bids in FY23-24.

- Exploration of opportunities in the metro sector, both elevated and underground projects.

Water Sector

- Slow awarding in the water sector during the initial six months.

- Expectation of momentum in the coming months.

Order Book and Presence

- Order book at Rs. 10,678 crores, spanning 11 states.

- EPC segment constitutes 51%, while HAM segment comprises 49% of the total projects.

Operational Highlights – EPC Projects

- Ganga Expressway at 29.3% completion.

- Delhi UER projects at 78.8% financial progress, expected to complete by December ’23.

- Neelmangala-Tumkur NHAI project at 15.6% completion.

HAM Projects Progress

- Raipur-Visakhapatnam packages progressing well, expecting completion by June ’24.

- Khammam-Devarapalle Project at 28.1% completion.

- Rewari Bypass project to be monetized in the second tranche.

Railway and Metro Project Updates

- Progress in DMRC Metro project at 26.6% completion.

- Appointed date received for RVNL Rail Project.

- LOA received for Kanpur Railway Station Project, with machine mobilization completed.

Other Updates for H1 FY24

- PCOD for Mancherial Project received on July 26, ’23.

- Final sanction for Varanasi-Ranchi-Kolkata packages 10 and 13 received from HDFC and Axis.

| Financial Highlights | H1 FY24 | Q2 FY24 |

|---|---|---|

| Standalone | ||

| Overall Revenue | Rs. 2140.8 crores (+17.8% YoY) | Rs. 869.5 crores (+15.6% YoY) |

| EBITDA | Rs. 343.2 crores (16% margin) | Rs. 138.4 crores |

| PAT | Rs. 180 crores (8.4% margin) | Rs. 61.7 crores (7.1% margin) |

| Consolidated | ||

| Consolidated Revenue | Rs. 2305.7 crores (+21.2% YoY) | Rs. 954.5 crores (+20% YoY) |

| Consolidated EBITDA | Rs. 500.9 crores (21.7% margin) | Rs. 220.2 crores |

| Consolidated PAT | Rs. 246.5 crores (10.7% margin) | Rs. 96.1 crores (10.1% margin) |

Strategic Move: Sale of 4 HAM Projects

-

Agreement:

- Signed share purchase agreement with Highway Infrastructures Trust (backed by KKR).

- Involves the sale of 4 HAM projects, a significant move for the company.

-

Transaction Progress:

- NHAI and lender approval secured for the first tranche of 3 SPVs.

- All conditions met for successful closure; expected in November ’23.

-

Financial Outlook:

- Confident in achieving expected numbers with a (+20%) revenue upside.

- Aiming for order inflow with Rs. 5000-6000 crores from road and diversified sectors.

-

Future Initiatives:

- Preparing for new projects, analyzing costs, and engaging with solar and metro sector clients.

- Focus on operational efficiency and execution capabilities.

-

Digital Transformation:

- Prioritizing digital transformation for automation in operations.

- Aiming for enhanced financial indicators through a transparent real-time working environment.

Order Inflow Concerns and Projections:

-

Initial Projections:

- Original expectation for the year was around Rs. 9000 crores order inflow.

-

Current Outlook:

- Current projection lowered to Rs. 5000-6000 crores due to slow progress.

- Factors influencing the decrease include state elections and delayed RFQ results.

-

Reasons for Confidence:

- Anticipated acceleration in NHAI projects, aligning with Gati Shakti initiatives.

- Optimistic about achieving a minimum of 3000-plus kilometers awarded in the next four months.

-

Future Initiatives:

- Diversification into metro and railway projects bidding with a potential of Rs. 8000 crores.

- Analysis and engagement in solar and metro sectors for new opportunities.

Compensation and Future Order Inflow:

-

Compensation for Shortfall:

- Confident in compensating for the current year’s shortfall in the next fiscal year.

- Expected addition of Rs. 10,000-12,000 crores from Quarter 2 onwards in FY25.

Revenue Growth and Segmentation:

-

Current Year’s Revenue Growth:

- Current projection for revenue growth is 20% compared to the initial 25%.

- On track with the annual report’s revenue target of Rs. 5400 crores for the year.

-

Segment-wise Breakdown:

- Revenue segmentation remains consistent with earlier projections.

- Major contributions from Ganga Expressway, six HAM projects, and diversified sectors like metro and railways.

Increase in Unbilled Revenue:

-

Ganga Expressway Projects:

- Milestone payments not aligned with physical progress.

- Unbilled portion around Rs. 150-200 crores due to the 2-3% gap in physical and financial progress.

- Continuity in unbilled status due to monthly milestone completion.

-

NHAI and SPV Projects:

- NHAI projects, especially in UER, facing similar milestone payment challenges.

- SPV projects experiencing an increase due to project execution initiation.

- Unbilled amounts likely to stabilize around Rs. 500 crores by Quarter 3.

- Old NHAI and MoRTH projects with receivables and claims causing unbilled figures.

Confidence in NHAI Ordering:

-

Strong NHAI Bidding Pipeline:

- NHAI holds a robust bidding pipeline.

- As of March ’23, approximately Rs. 60,000 crores worth of projects were expected to be awarded.

- Delayed due to certain reasons, NHAI plans to award Rs. 40,000 crores by the end of the year.

- Anticipating the awarding of around 2500-3000 kilometers from the current bidding pipeline.

Revenue Guidance and Inflow:

-

Current Fiscal Year (2023-24):

- FY24 Revenue Guidance: Targeted revenue of Rs. 5,400 crores.

- FY25 Revenue Expectation: Anticipating revenue in the range of Rs. 6,000 to Rs. 6,200 crores.

-

Future Revenue Growth:

- FY25: Expected to complete existing projects, anticipating revenue from existing order backlog to be around Rs. 5,500 crores.

- Order Backlog: Rs. 10,600 crores.

- Targeting to add new orders in the range of Rs. 5,000 to 6,000 crores.

Margin Guidance:

- Expected Margin: 15.5% to 16%.

Impact of Construction Ban in Delhi NCR:

- UER 1 and Metro projects expected to have minimal impact.

- Special permissions anticipated due to the high priority and monitoring by PMO.

- Pollution department likely to grant relaxation for these projects.

Arbitration Claims:

- No significant arbitration claims against NHAI or any government body.

- Small claim of Rs. 10 crores with Agra Development Authority; Rs. 6 crores already provided.

- Consolation in progress for four NHAI projects completed in 2018, amounting to Rs. 22 crores.

Segment-wise Revenue Breakup for Q2 FY24:

- Ganga Expressway (Adani Project – Mancherial): Rs. 290 crores

- NHAI EPC: Rs. 188 crores

- SPVs: Rs. 303 crores

- Metro and Railway: Approximately Rs. 52 crores

Railway Projects Margins:

- Bidding margin for railway projects is set at approximately 14%.

Competitive Scenario:

- HAM: Moderate competition with 7 to 10 bidders.

- EPC: More aggressive with 20 to 25 bidders.

Diversification Projects Margins:

- Diversified sector projects (e.g., water, metro) margins range from 12% to 15%.

Revenue Composition:

- Targeting at least 10% of total turnover from metro and railway projects this year.

- Aiming for 20% of total order execution by 2025 and 25% by 2026 from diversified sectors.

Depreciation Increase:

- Increase in depreciation due to the addition of new assets, particularly shuttering.

- Expected to continue throughout the year.

- Shuttering depreciates faster, impacting the overall depreciation cost.

- Anticipated depreciation and interest costs to remain similar to the previous year, with a slight increase of about 0.25%.

Execution Timeline:

- Highway Projects: Approximately 24 to 36 months.

- Railway Projects (e.g., Kanpur Railway Station, RVNL): Ranges from 30 to 36 months.

- Metro Projects: Typically completed in about 30 months.

- Water Projects: Execution timeline extends to around 36 months.

PAT Margin Analysis:

- Recent Decline: Standalone PAT margin affected by a rise in interest costs.

- Asset Monetization Impact: Anticipated improvement in PAT margin due to asset monetization of HAM projects.

- Finance Costs: Expected to be in a similar range as previous years, around 1.25% of total turnover.

- Employee Costs: All-time high due to project mobilization, but anticipated to normalize.

Future Outlook:

- PAT Margin Improvement: Confidence in the PAT margin returning to earlier levels, potentially around 8.6%.

- Finance Costs Management: Efforts to maintain finance costs within the historical range.

- Mobilization Impact: Employee costs expected to stabilize as execution catches up.

Ganga Expressway Impact:

- Acknowledgment of the concern regarding the eventual completion of the sizable Ganga Expressway project.

- Capability and Qualification: Successful completion of significant elevated portions in projects like UER at Delhi and Gurgaon Sohna positions the company for bidding on large-sized projects.

- Future Prospects: Exploration of opportunities in high-magnitude projects, including high-speed network corridors for railways and tunnel projects through joint ventures and alliances.

Order Inflows Analysis:

- Bidding Activities: Participation in several bids; however, loss of projects due to unmet margin expectations.

- Expected Momentum: Anticipation of an increase in momentum and order inflows from November onward.

- Market Share Loss Explanation: Loss of projects with unsatisfactory margins; optimistic about the upcoming months.

Bidding Activities Overview:

-

Road Sector Bids:

- Submitted bids for 6 road sector projects.

- Bidding on the Chambal Expressway project.

-

Railway Sector Bids:

- Expressed interest in railway projects, estimating opportunities worth around 8,000 crores.

- Shared ongoing bids in the state of Chhattisgarh; results pending.

Diversification Strategy:

-

Metro Projects:

- Qualification for metro projects achieved through recent project completions.

- Expectations of bidding for metro projects, independent of railway opportunities.

-

Tunnel Opportunities:

- Exploring tunnel opportunities in Northeast states, including Himachal Pradesh, in collaboration with DRO.

-

Joint Ventures and Alliances:

- Existing Orders: Solely secured all current orders without joint ventures.

- Future Prospects: Consideration of joint ventures for projects where 100% qualification is challenging (e.g., water projects, large-scale metro).

Amit Singh Learning page (17-11-2023)

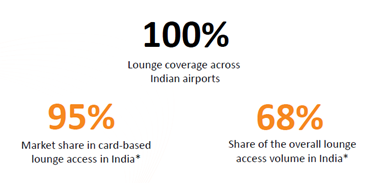

Dreamfolks:

Q2 FY24 Highlights:

-

DreamFolks has delivered a strong revenue performance registering 65% growth YoY in Q2FY24 while on a QoQ basis revenue grew marginally by 6%.

-

PAT increased by 1.39% @6.25% QoQ at Rs. 18Cr.

-

The domestic passenger traffic, as reported by the DGCA, has witnessed a growth of 20% on YoY basis in H1FY24, while the Dreamfolks pax has increased by 47% in the same period.

-

Above indicated growing demand for lounge service.

-

The industry is also going through a structural change where card issuers are changing the program structure of the benefits to a spend-based structure.

-

At Industry level optimization in benefits for non-premium cards may have short term impact leading to reduction in revenue. For the longer term the move to a spend based benefit mechanism will be beneficial for all stakeholders concern

-

As travel industry is poised from growth DreamFolks is well positioned to capitalize on growth opportunities

-

Revenue Mix is 76% Domestic Card holders and 24% International card holders.

-

Having 40 Cr as Cash reserve.

-

Partnership with top E-SIM provider for hassel free service to International customers.

-

PAT avg at 9.38% for FY23 and now at the rate of

-

ROE and ROCE is at > 60%

-

Asset light company, and no capex is planned. Even if any capex is required it will be done through internal accruals and not through loans.

-

Encouraging external tailwind in terms of increasing Air travel (@ 20% Quarterly increase )

-

Margin prediction for future annual guidance is maintained at 11 to 13%.

-

Avg Rev per passenger improved from Rs. 950 to Rs 990/-. With passenger base growing from 2.63 Million to 2.7 Million QoQ.

-

Rs. 343 Cr is invested by company in overnight funds and FD. Completely secured based and not in equity.

-

Any price increase on the lounge service is passed on to the card issuing banks. Power of pricing. Ensuring that margins are intact.

-

Railway business is also gaining traction.

-

1.76 Cr is the ESOP charges.

-

Additional lounges are opening up in all metros and Hyderabad due to increase in demand.

Praveen’s Portfolio (17-11-2023)

Concall notes and Result summary:

Vishnu Chemicals Ltd

- In the process of Chromium mines and processing plant. The acquistion of Chromium benefacation plant is to secure the consistent supplies and not for cost saving.

- Starting up of Barium sulphate plant costed ~5crs. Demand outlook is strong. Currently in the approvals process with Big players. Supplies to start from Jan 2024

- Done QIP for working capital and debt reduction

- QOQ: Chromium volume is there, but chrome ore price went up, so GM reduction. Realization of chrome product also dipped

- Expect the utilization to move from 70% in Q2 FY24 to 90% by Q4 FY24

- Chrome ore prices went up 25% in last 3 quarters

- Barium chemicals: Received approvals from big paint manfrs. Utilizaiton to go from 40% in Q2 to 60% in Q4.

- Depreciation and Finance cost impacted the bottomline

- Domestic demand is stable but Exports are seeing headwinds (still doing good in volumes as co is leader in domestic market).

- Barium Carbonate: Mainly related to Infra/construction industry. Dumping from China is impacting the demand (since china real estate market is facing headwinds). The main application is in tiles, water purification, bricks etc. Domestic demand is good

- Largest Chromium plant in Eu being shutdown. They used to supply very speciality grade product. Co, is developing that product and in the R&D and Approval process. Expecting to supply from Q4 Fy24/ Q1 FY25

- H2 should be (much) better than H1.

- International markets contribute ~50% revenue. But international market has demand headwinds. But the co is planning to manage by focusing on barium suplhate, barium carbonate and other derivative

- Next CY, Next FY: Commisioning and ramp up of utilization in subsidaries. Reducing cost of power through solar, Backward integration of Soda ash plant ramp up in utilization. These factors will improve the profitability in next year. Macro factors if become better, would lead to even better growth

- Scope for margin expansion: Above mentioined points. Flexible product mix is the main factor that the management wants to realize. Chrome ore acquistion would help.

- Domestic : Export ratio is ~54: 46

Note: Missed lot of details in the summary. Advise to read concall transcript or listen to concall recording

Phillips Carbon Black (17-11-2023)

Significant jump in share price today… any specific reason?

DELHIVERY – One stop solution for shipping and parcel delivery (17-11-2023)

Based on your study, what’s the moat? How do these companies differentiate?

Mudit’s Portfolio (Passively Active) (17-11-2023)

from 1st January 2023 till today (17th nov 2023) my XIRR returns are 24.33%