@Keyur_Joshi we are doing what you are suggesting actually. We are not taking SD of the prices. Instead, we are taking SD of the daily price change. This is very comprehensive and captures the volatility nicely.

Posts tagged Value Pickr

XIRR Calculator for your stock portfolio (15-10-2024)

Thankyou for showing interest. Please make a copy of the sheet and use so that the original data is protected and also to keep your personal trading data private to yourself.

Please comment if you need more help!

Smallcap momentum portfolio (15-10-2024)

One query

There is standard deviation used for the calculation.

However I feel that it does not indicate true volatility…

Say the values 3,7,5,8 gives STD as 2.22…

and values 3,5,7,8 also give same STD… However the second one is smooth in terms of time-series.

Any idea how to tackle this case? How can we ensure that the price has increased smoothly over the period. STD does not capture that essence.

I read that people calculate daily return, convert that to annualized one… Then take STD of those returns… That may resolve some aspect, but still it does not capture the time series aspect.

XIRR Calculator for your stock portfolio (15-10-2024)

Hi, don’t have the editing rights for the same. It is set to view only.

Loyal Equipments (15-10-2024)

Loyal Equipments AGM’24 Notes

- Margins: Drop in GM in recent years due to increase in RM costs. Going forward expect ebitdm to grow to 22-23% with increasing scale

- Order Book: In good shape, have good order book in place (15-20% higher YoY) but last 1-2 months is down due to elections but will pick up.

- The recurring annual contract with Linde Engineering for 20Cr/annually will end in 2025 and it will get reviewed and mostly get renewed. The contract was to provide Modular Skids.

- Modular Package/Skid is the major product which the other competitors don’t provide so have an advantage in here and the market is shifting towards modular skid.

- Product Mix (FY’24):

- Modular skid/package: 30-40%

- Heat exchangers: 40%

- Auxilary Skids: 10%

- Pressure Vessels: 10%

- Expansion Plan: UAE office will be completed in 6 months. Already in USA doing sales & marketing and now will add a manufacturing plant in USA on the demand of a customer which might start by FY26-27.

Key Concerns:

-

Dependency on contracts/orderbook, top client (Linde) if doesn’t renew contract then revenues could be impacted too

-

Competitive Intensity: There is no differentiation in products and the other key players in market are at a bigger scale/are more established. And according to Loyal equipments their MOAT/differentiation keeping them in the market is their product mix – they claim no one else supplies Modulary Skids but once competition starts supplying then revenues could be hit pretty bad as contribution is very high ~50%

-

Working capital intensive business – Loyal’s revenue is dependent on large project by the user industry and typically the delivery period may vary from 30-150 days. If we look at its overall working capital days it remains between 100-200 days. These will also depend on dispatches during the year end.

Newgen Software (15-10-2024)

I think good set of results >https://www.bseindia.com/xml-data/corpfiling/AttachLive/c2fad84e-05cd-41ec-adf4-1c83cac0ee9e.pdf

Going by their history, They’ve usually reported +30% in H2 comparing H1.Going by this i think newgen has good quarters ahead and should do better than last year.

They got small content management order from USA.

D-Invested

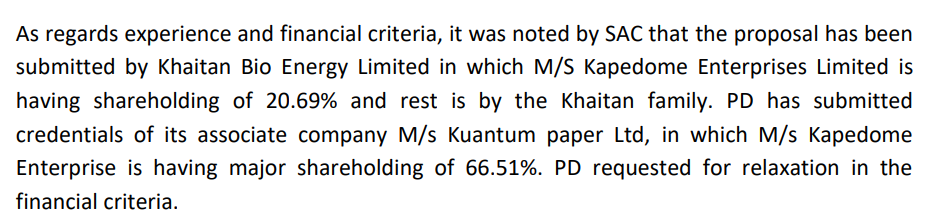

Kuantum Paper – Strong Turnaround (15-10-2024)

An update on this ethanol story – Found this piece of information on public domain. The khaitan bio energy which was mentioned in the previous post is held privately by the Khaitan family. Attached screenshot :

Also there was no follow up update on the ethanol story in this year’s annual report. The piece almost vanished in thin air.

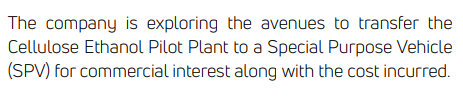

Earlier, in 2023 annual report there was a half page writeup on the ethanol story with a mention of creating a SPV and a concluding statement that read –

This was a bet on paper companies venturing into ethanol production, anticipating a boom similar to the sugar industry. However, it appears the management intends to keep the benefits to themselves for now.

Disc: Squared my position.

Sumit’s Portfolio (15-10-2024)

Here’s a summary of the key updates for UGRO Capital Limited for the quarter ended September 30, 2024 (Q2 FY25):

-

AUM Growth:

- Total Assets Under Management (AUM) crossed INR 10,200 Cr, compared to INR 9,218 Cr in the previous quarter (Q1 FY25) and INR 7,592 Cr in the same quarter last year (Q2 FY24), reflecting a 34% YoY growth.

-

Loan Origination:

- Achieved the highest-ever quarterly net loan origination of INR 1,970 Cr, up from INR 1,146 Cr in Q1 FY25 and INR 1,477 Cr in Q2 FY24.

- Significant growth in Micro Enterprises loans, with disbursements doubling to INR 450 Cr in Q2 FY25 compared to INR 209 Cr in Q1 FY25. This segment now contributes 11% to AUM, up from 8% in Q2 FY24.

-

Co-Lending and Liability Profile:

- Co-lending volumes reached INR 600 Cr, the highest ever, expanding partnerships to 9 banks and 7 NBFCs.

- Mobilized INR 1,100 Cr in borrowing during Q2 FY25, compared to INR 375 Cr in Q1 FY25.

- Total liabilities (excluding Direct Assignment) stand at INR 5,300 Cr, with a diversified borrowing mix: 45% from banks, 31% from capital markets, and 26% from Development Financial Institutions (DFIs) and Financial Institutions (FIs).

-

Ratings and Recognition:

- Received an upgrade from India Ratings to ‘IND A+/ Stable’ for long-term and ‘IND A1+’ for short-term borrowings.

- UGRO Capital was awarded Best Fintech Lender of the Year by Financial Express.

ugro updates.pdf (2.9 MB)

Sumit’s Portfolio (15-10-2024)

Infollion Research Services Limited: Financial Performance Overview (H1 FY2024 vs H1 FY2023)

| Particulars | H1 FY2024 (₹ Lakhs) | H1 FY2023 (₹ Lakhs) | Percentage Change (%) |

|---|---|---|---|

| Revenue from Operations | 3,518.86 | 2,510.91 | +40.14% |

| Total Income | 3,618.00 | 2,543.80 | +42.23% |

| Cost of Sales | 1,854.93 | 1,333.44 | +39.11% |

| Employee Benefits Expenses | 807.94 | 544.69 | +48.33% |

| Other Expenses | 142.18 | 96.37 | +47.54% |

| Profit Before Tax (PBT) | 793.73 | 565.57 | +40.30% |

| Profit After Tax (PAT) | 593.81 | 422.90 | +40.35% |

Sumit’s Portfolio (15-10-2024)

Anand Rathi Q2 Performance :

Anand Rathi Wealth Limited (ARWL) had a strong Q2 FY25, with total revenue reaching ₹249.6 crore—a 32% year-over-year growth. Profit After Tax (PAT) also increased by 32%, standing at ₹76.3 crore, maintaining a solid margin of 30.6%.

Their Assets Under Management (AUM) grew by 57% to ₹75,084 crore, reflecting their success in both attracting new clients and deepening existing relationships. Client growth hit nearly 20%, and the addition of 374 relationship managers (+20% YoY) supports this expansion.

Costs, like employee expenses, grew but remained efficient relative to revenue. Client attrition was minimal, showing strong loyalty with only 0.2% of AUM lost.

Looking ahead, ARWL raised its FY25 revenue target to ₹980 crore and AUM to ₹80,000 crore. The board declared an interim dividend of ₹7 per share, further rewarding shareholders.

In summary, ARWL continues to scale its business, grow profits, and capitalize on opportunities in India’s wealth management sector.