Attended Pricol conf call. It seems participation was very low as I got opportunity to ask questions 3 times in a 30 mins call. Key points discussed- 1. Slower growth this quarter as they lost some EV sales, however EV sales have started picking up and they expect better growth in H2. 2. Still maintain guidance of 3600 cr of organic revenue by FY26. 3. Margin will steadily increase 0.3-0.4% every quarter to reach margin of 13.5% in next 2 years. 4. Creating a capacity of 3800-4000 cr with 600 cr of capex to be completed by FY25.

Posts tagged Value Pickr

Manappuram Finance (09-11-2023)

“HDFC bank enabling 200-300 branches every quarter for gold loans. They have been pushing gold loans majorly”

Caplin Point Laboratories (09-11-2023)

Strong statement on presentation :

Commenting on the performance, Mr. C.C. Paarthipan, Chairman said:

“We have multiple levers of high quality and consistent growth at Caplin, with the major one being our growth in existing markets in Latin America. This is evidenced by the fact that Q2 FY24 revenue of Rs.430 Cr and PAT of Rs.116 Cr are higher than the FY17 full year revenue (Rs.412 Cr) and PAT (Rs.96 Cr) respectively. Our US business also continues this pattern, as our H1FY24 revenue is higher than

our FY22 full year revenue. With our sharp focus towards enhancing our presence in the larger markets such as US, Mexico and Chile, we expect the next few years to be crucial and exciting for the company.Our initiatives into backward integration (API) and forward integration (front end presence) will adequately support the company’s prospects for top and bottom line growth, with stable cashflows.

We remain steadfast in our commitment to driving sustainable growth with benchmark cashflows and robust bottom line.

TCPL Packaging Ltd. — Statistical Facts & Figures — Views Invited (09-11-2023)

TCPL has achieved the highest revenue run-rate in its history in the quarter ended September 30,2023

TCPL has also successfully commissioned a new advanced offset printing line, complemented by modern ancillary equipment at the Haridwar facility.

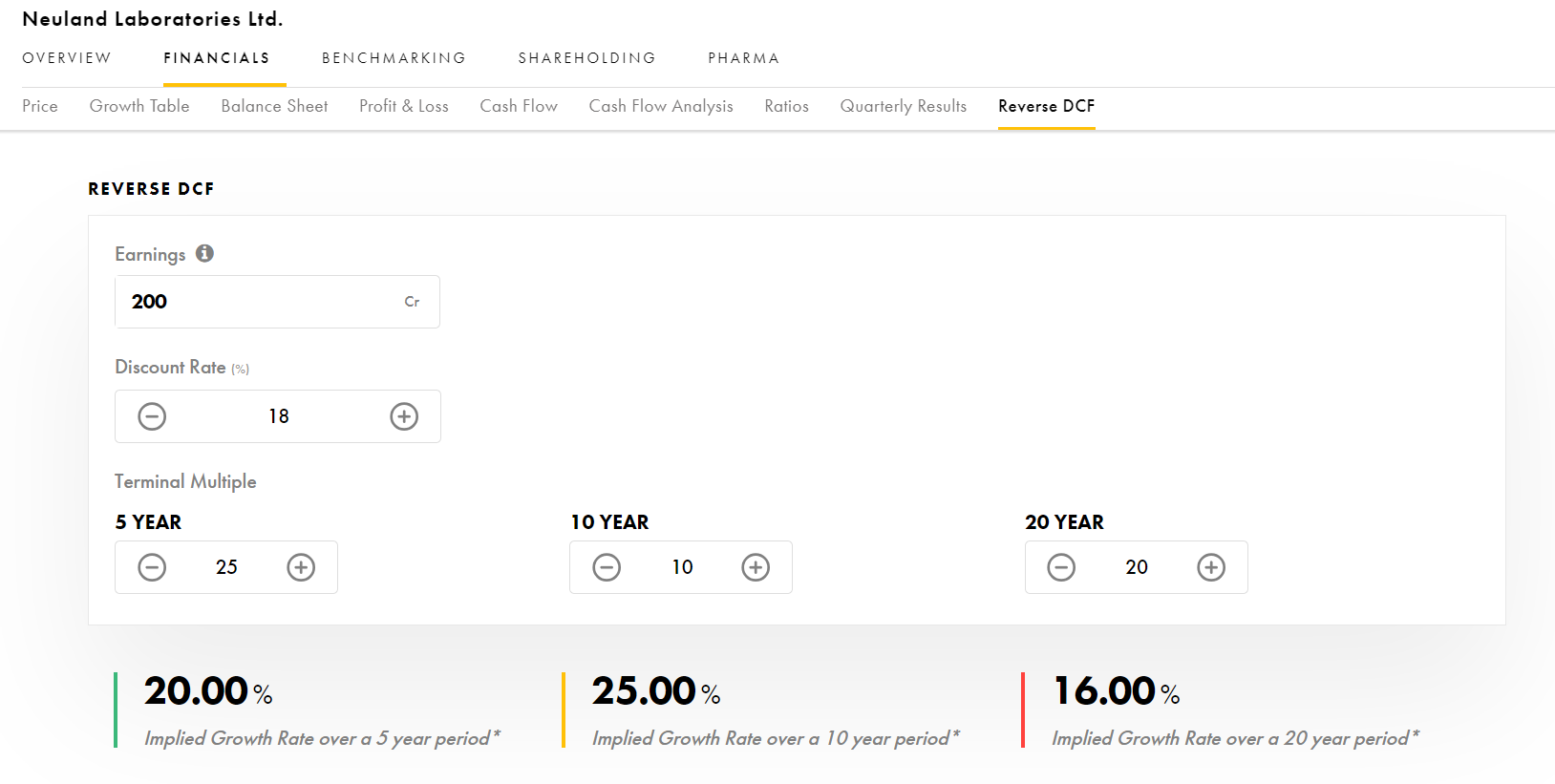

Neuland Laboratories Limited – Transformation towards niche APIs? (09-11-2023)

I usually do a reverse DCF to get an appx sense

To make 5yr cagr of 18%, earnings need to grow at 20%, assuming exit multiple of 25 which is not outrageous to me

!

Pidilite Industry : Fevicol ka Jod (09-11-2023)

Is it not indirect admission that pidilite cannot grow on its own core business?

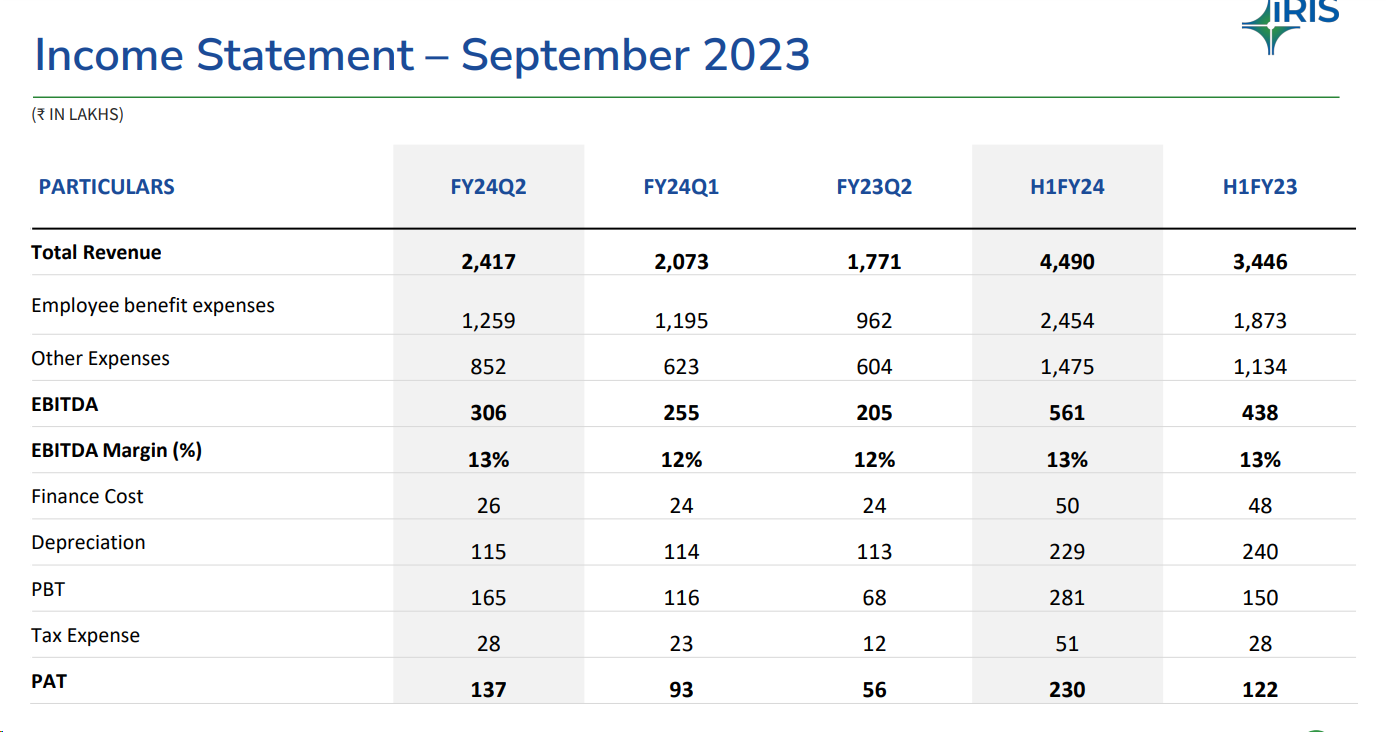

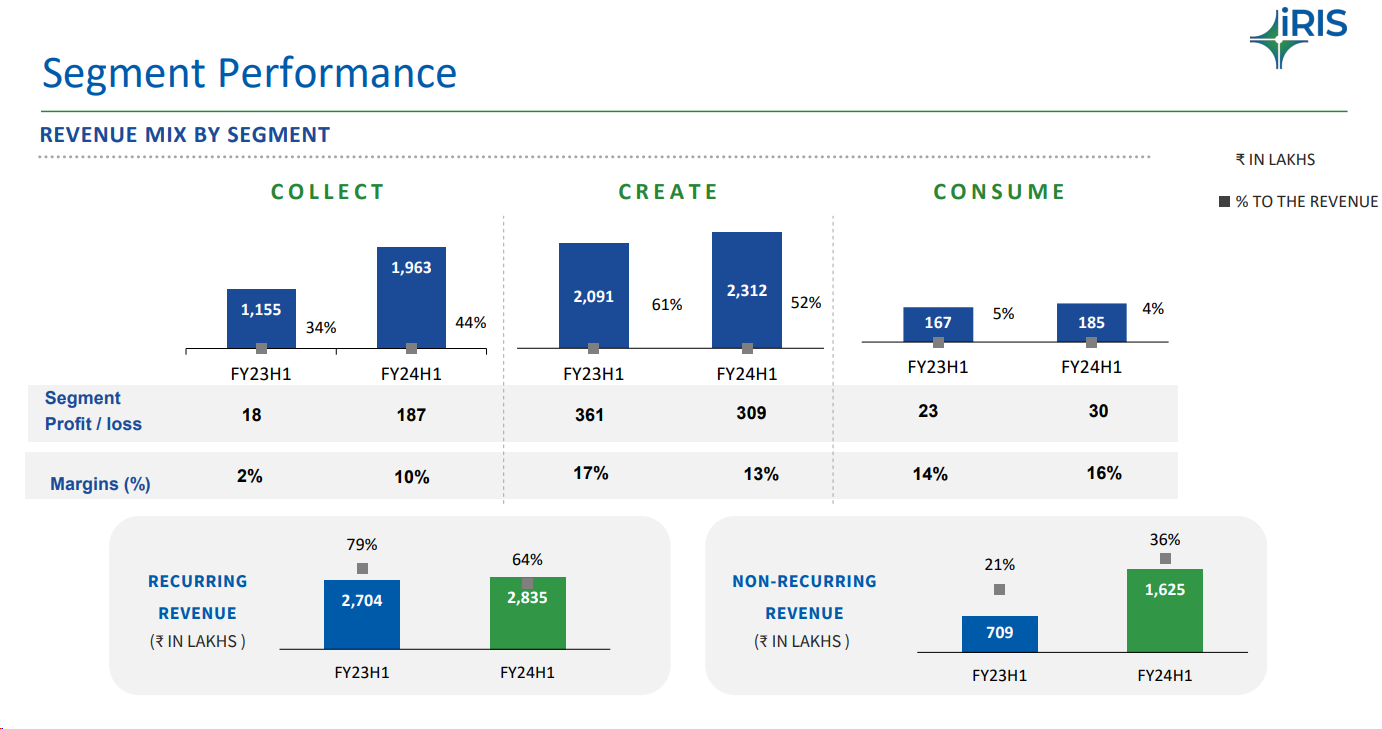

Iris Business Services – Emerging SAAS Microcap (09-11-2023)

Snippets from the Investor presentation Q2 FY24

Financial Performance : Descent growth albeit on a low base and low absolute value.

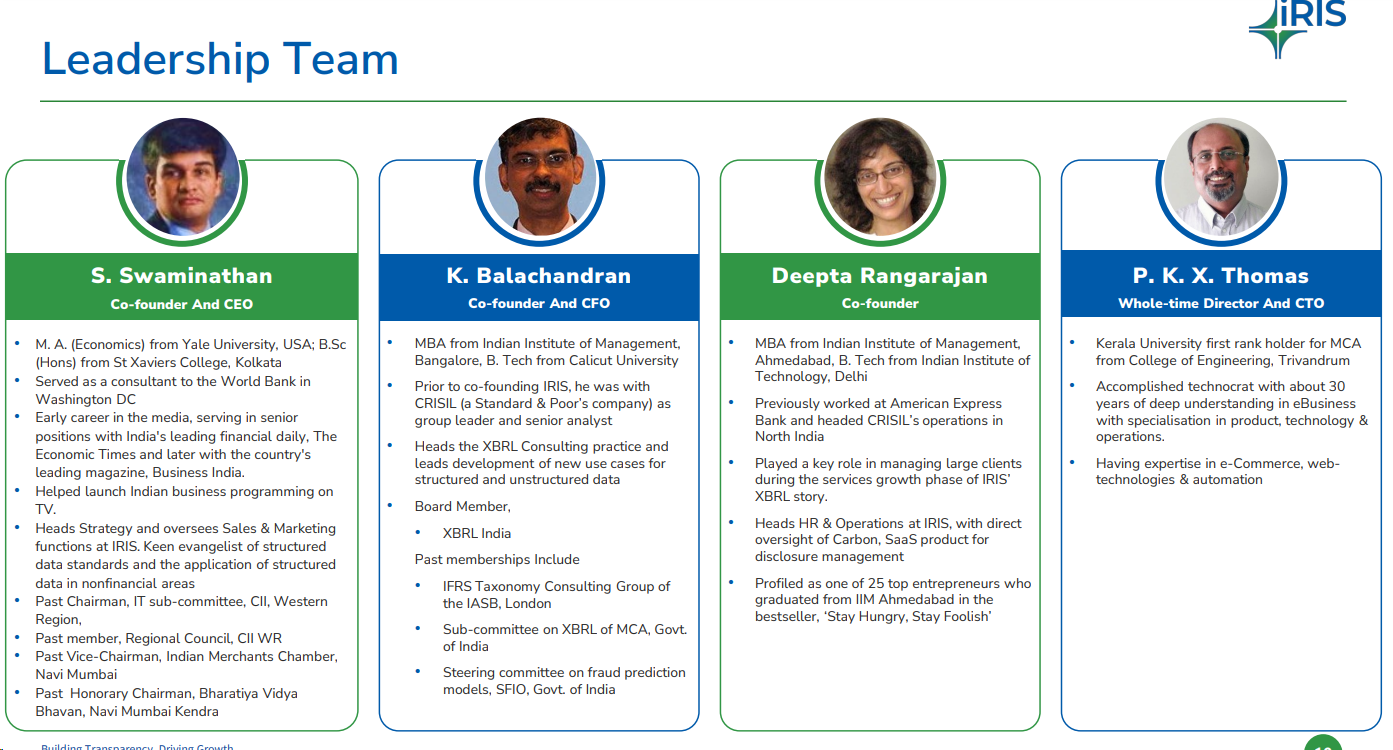

What I am enamored by is the quality of the management ![]()

Segment wise performance :

Thanks @Lynch for bringing this company to the notice . Nice find.

Disc : I have started a tracking position in this company. Not very sure how Large Language AI models might disrupt their business though , since they are into XBRL compliance and automating disclosures .

Neuland Laboratories Limited – Transformation towards niche APIs? (09-11-2023)

Valuation is a very subjective topic to discuss. Here are my two cents in this case. Thanks to @Worldlywiseinvestors, Aditya Khemka, and @unseenvalue for their public teachings.

The common framework for valuing Pharma companies is EV/EBITDA and PE. @Worldlywiseinvestors mentions following bull, base, and bear scenarios. In the bull case, the aspiring company (Neuland) will reach the valuation of leaders in the segment (such as Divis and Syngene). The base case will be for EV/EBITDA to grow according to the YoY growth of the company, and the bear case will be going below the last 3 or 5 years of EV/EBITDA.

In similar lines, Aditya Khemka mentions underperforming and outperforming companies, essentially leaders and newcomers. In the case of CDMO, he mentions a minimum of 12 and a maximum of 25 EV/EBITDA multiples, and in terms of PE, 18-45, which covers the broad range.

If you believe Neuland is still cyclical, the current valuation might have no margin of safety. If you believe it has joined the list of CDMO players, you may expect a consistent compounder type of company and growth rates.

The Art of Valuing Pharma & Healthcare Companies in Youtube.

Pidilite Industry : Fevicol ka Jod (09-11-2023)

seems like a John Deere model. I came to know that they also have internal lending business and it helps them keep PAT at good levels by keep good margins.

my understanding so this should bode well for pidilite as well.

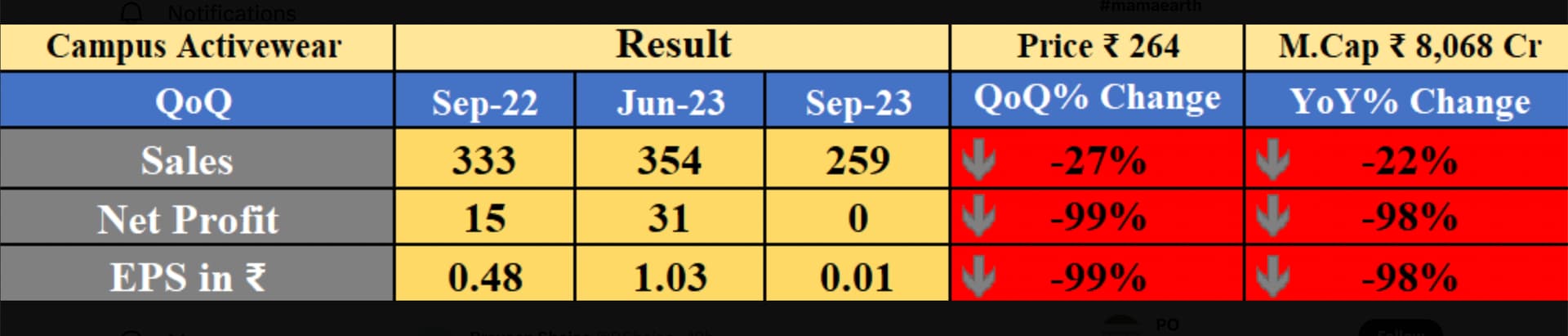

Campus Activewear – betting on the India Consumption Theme (09-11-2023)

Q2 Results FY23-24

Very bad results.

Lesson learned: don’t ignore red flags (Insider Trading & COO resignation)