Is anyone currently tracking this company?

Posts tagged Value Pickr

Hero Motor – Leader in two wheeler (06-11-2023)

Hero have already stated that after taking Vida to 100 cities in this fiscal year, they would be launching lower-priced EV products in FY 2025.

Transpek Industry limited (06-11-2023)

What could cause sharp downtun in Q2 revenue.… from 216 cr to 120 cr YOY…They did not gave any warning as such.

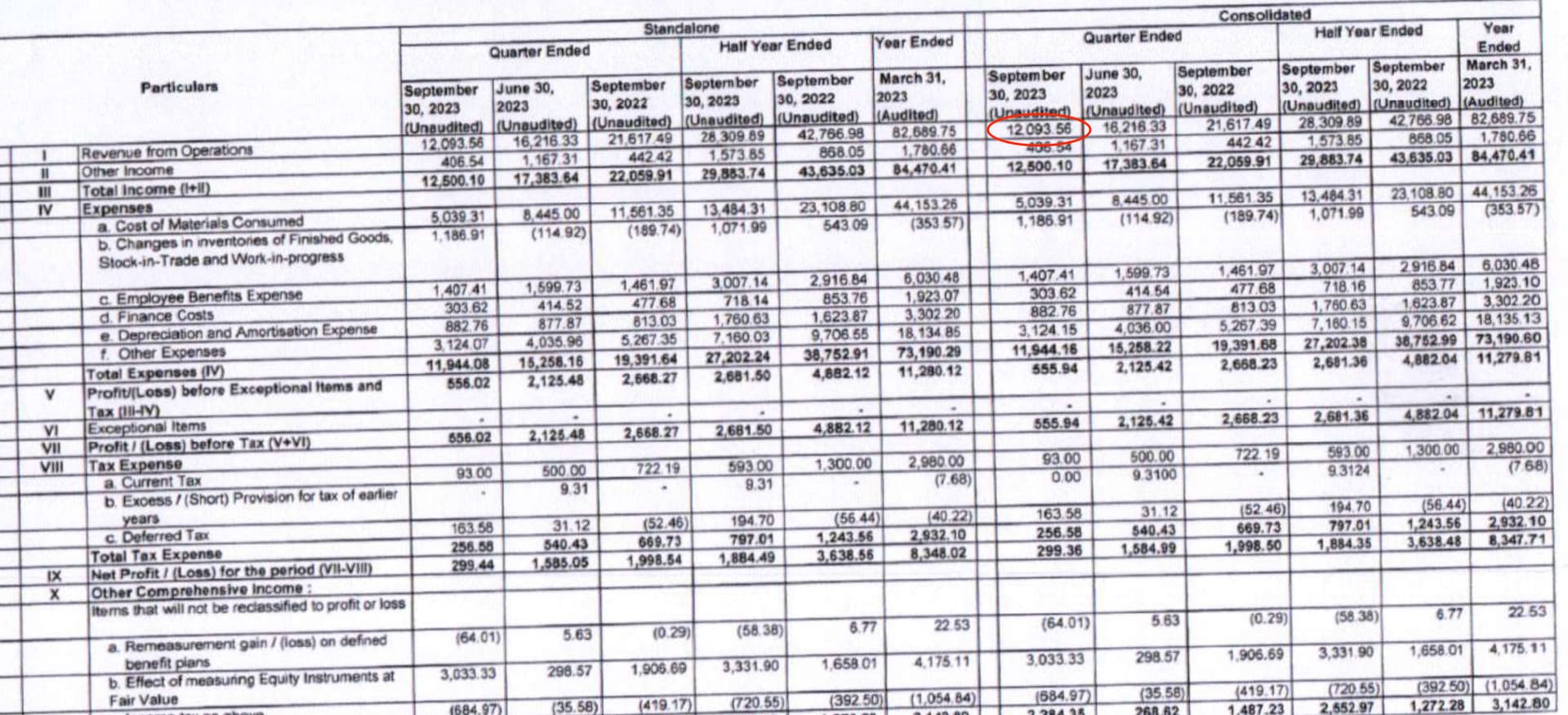

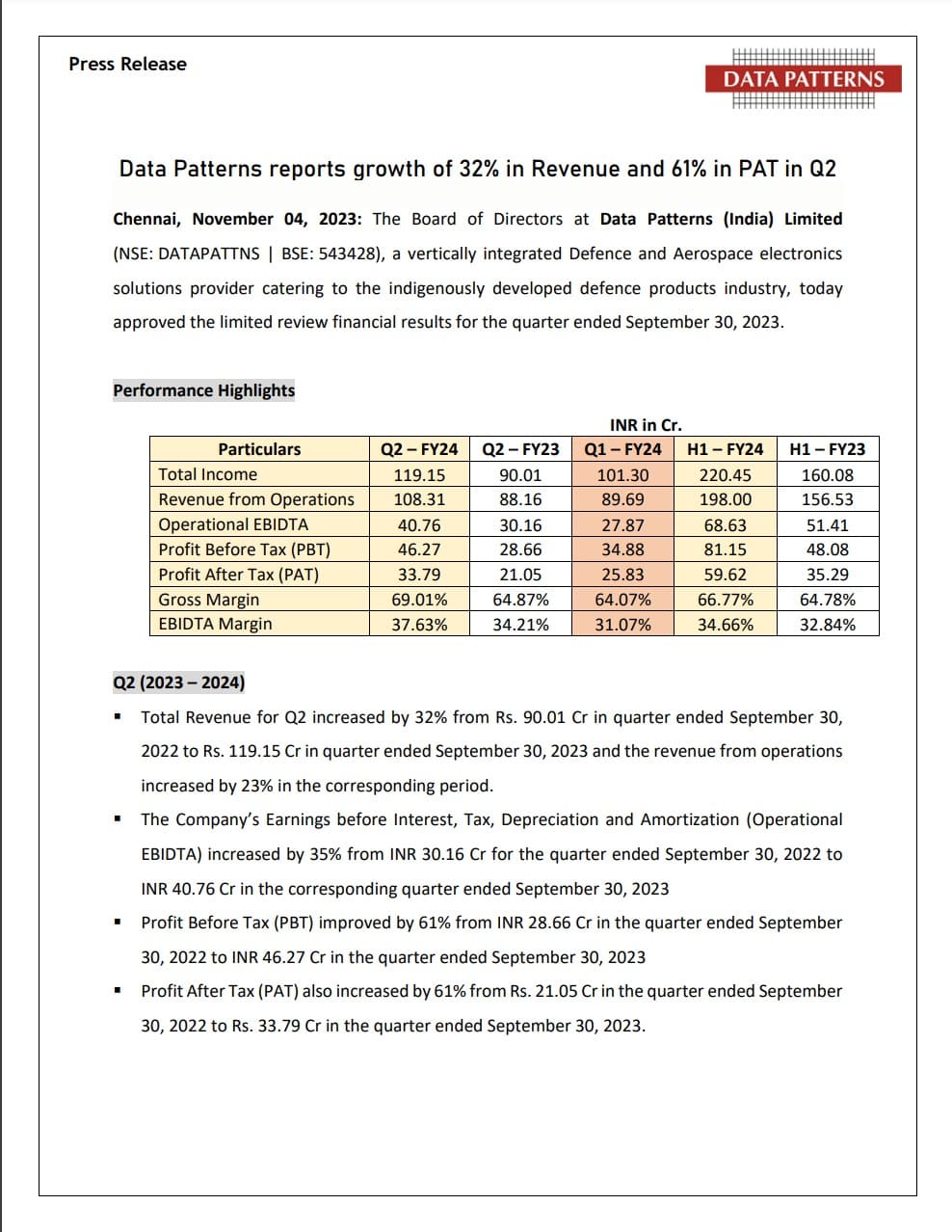

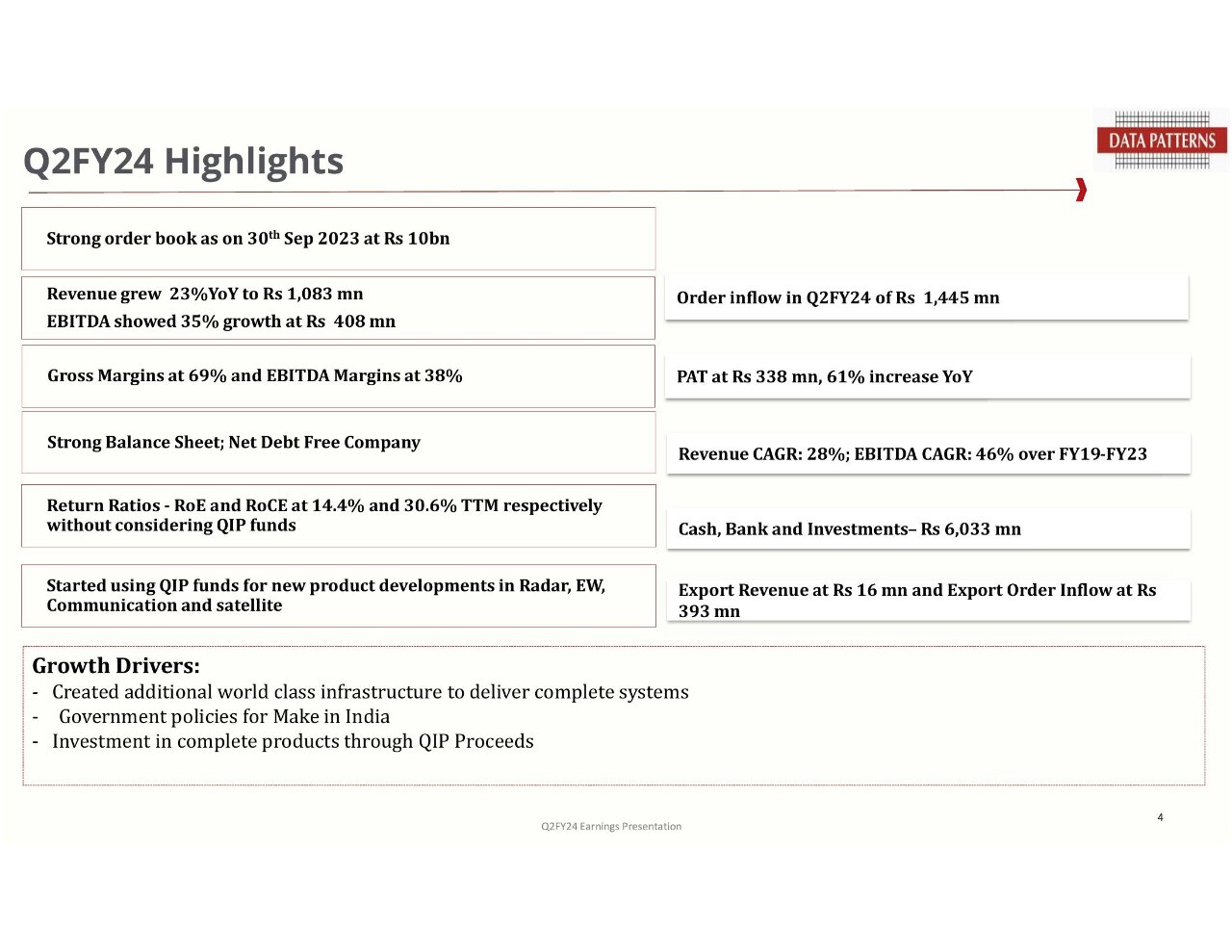

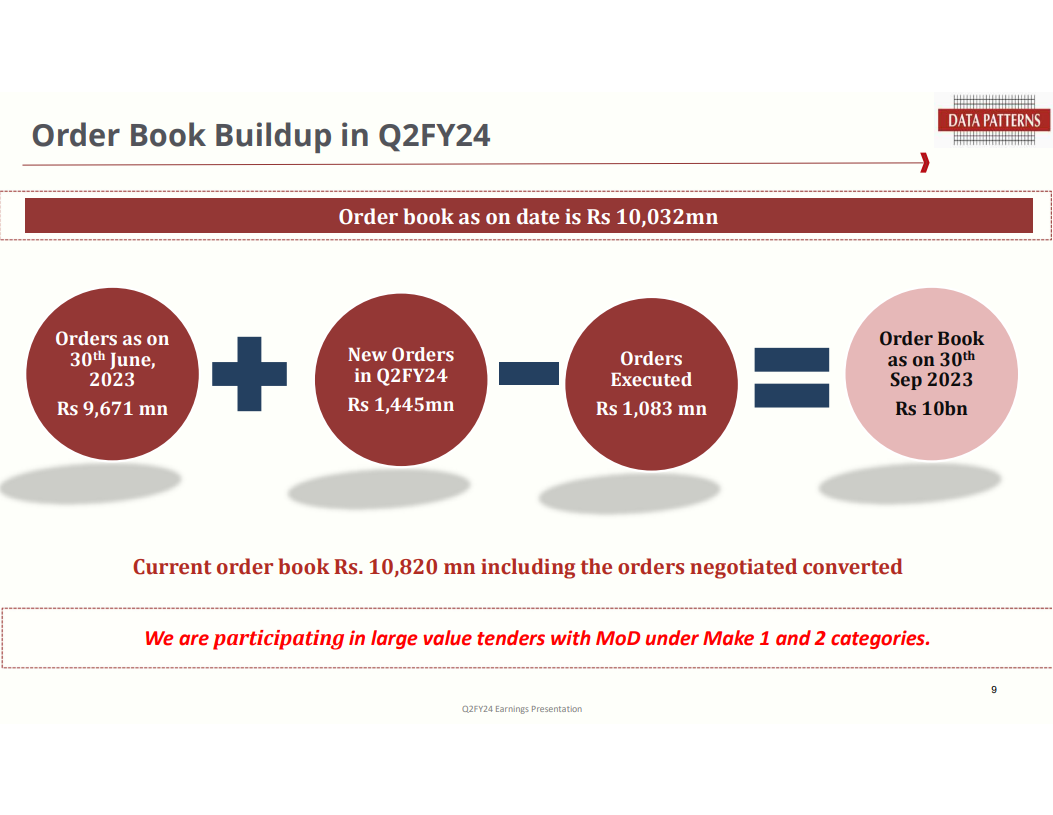

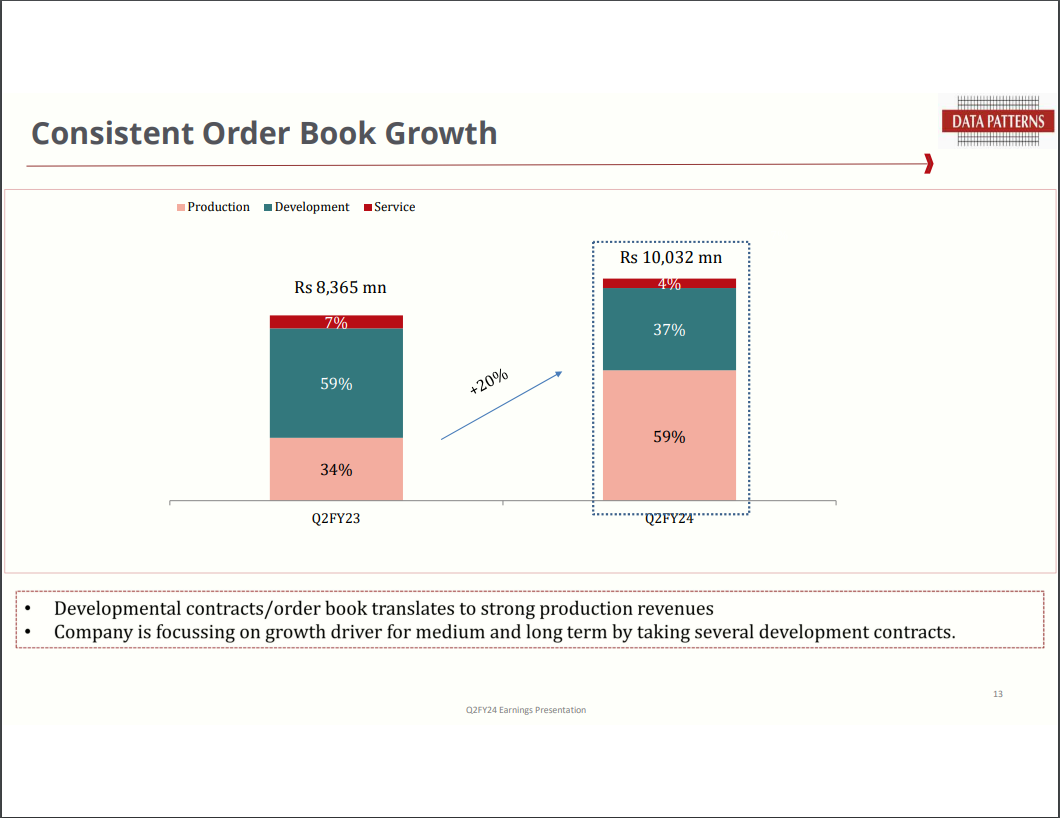

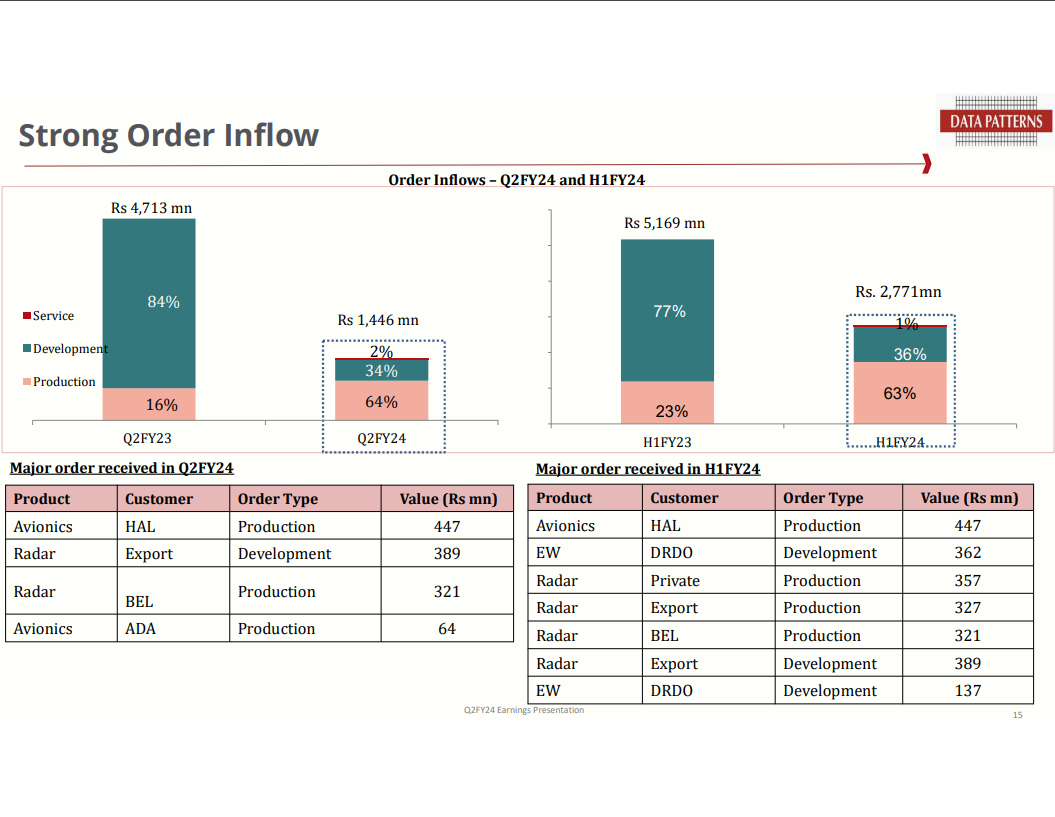

Data Patterns (India) Limited (06-11-2023)

Data Patterns (India) Limited, a defense and aerospace electronics solutions provider, has reported significant growth in its financial results for Q2 FY 2023-24.

Key Highlights:

- Total income for Q2-FY24 increased by 32% compared to the same period last year.

- Revenue from operations in the same quarter increased by 23%.

- Operational EBIDTA increased by 35%.

- Profit Before Tax (PBT) improved by 61%.

- Profit After Tax (PAT) also increased by 61%.

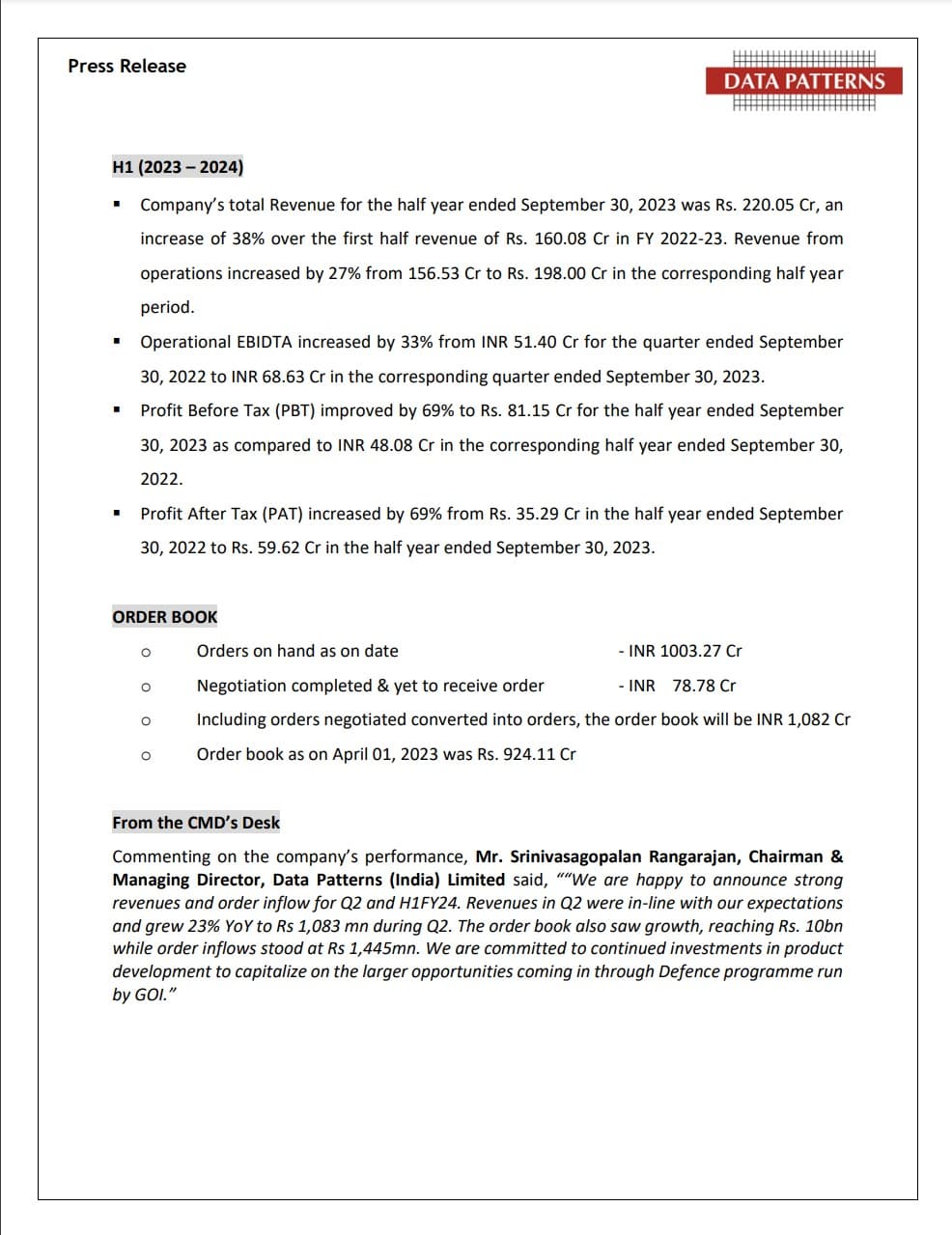

For H1 FY 2023-24:

- Total revenue for the first half of the year increased by 38%.

- Revenue from operations in the corresponding half-year period increased by 27%.

- Operational EBIDTA increased by 33%.

- Profit Before Tax (PBT) improved by 69%.

- Profit After Tax (PAT) increased by 69%.

Additionally:

- The company’s order book as of the date stands at INR 1003.27 Crores.

- Orders negotiated but not yet received are at INR 78.78 Crores.

- Including converted negotiated orders, the total order book reaches INR 1,082 Crores.

Mr. Srinivasagopalan Rangarajan, Chairman & Managing Director of Data Patterns (India) Limited, expressed satisfaction with the strong revenues and order inflow for Q2 and H1 FY24. The company is committed to further investments in product development to capitalize on the opportunities in the defense program run by the Government of India.

Punjab Chemicals & Crop Protection Limited (PCCPL) A Clear Runway Ahead! (06-11-2023)

Q2FY24 Results

Industry Headwinds

-

Revenues impacted due to high channel inventory

-

Price erosion due to heavy dumping by China

-

Demand continuous to be sluggish

-

Price pressure is as intense as ever

-

Margins improved due to efficiencies in the processes (investment on equipment upgrade helped ), new products with better margins

Factors that impacted this are broadly due to below

- Product Mix (Promoted products that are more profitable )

- Cost Management ( Logistics, Fuel, People )

- Productivity and Efficiency ( Investment in R&D, process efficiencies , reduced waste)

- Innovation and R&D ( Added more people )

- Customer centric Approach – Helped to understand current market conditions and understand customer requirements

-

Revenue Mix – Domestic 48%

Margins

Gross Margins 40.6% ( vs 35.5% same period last year )

EBIDTA Margins 14.6% (vs 12.1% same period last year )

PAT Margins 7.5% ( vs 6.9% same period last year )

- One time interest cost of 1.98 crore

- Added 27crore worth of fixed assets

- Focusing more on data driven decision making, to achieve this, we are in the process of implementing S/4 Hana

- Working Capital days increased from 63 to 72 days (this is due to more domestic sale and that is the nature of domestic market, but sill Punjab is best when compare to peers )

- New molecules commercial supplies will pick in H2

- 40% of the new enquires are from non agchem space

- Expecting few registrations from Europe (very soon )

- Metconazole , capacities are fully utilized

- Lalru facility is mainly for Pharma and Specialty products (Current utilization is 55% )

- Looking for new site for Agchem products

Growth / Margin Guidance

18 – 20% Revenue growth

Aiming to achieve 18% EBIDTA Margins

Priyank’s Portfolio (06-11-2023)

I like your way of seing companies. Could you elaborate what concerns you had about management decisions like which decisions etc and also which lack of vision?

Thanks

Shivalik Bimetal Controls Ltd (SBCL) (06-11-2023)

Thanks, Ahmed. It is also showing on Screener now.

Kirloskar Oil Engines Ltd – Generating Returns from Generators (06-11-2023)

Thanks .

- The levers for margin enhancement are:

- Entry into higher horsepower segment

- Growing service and aftermarket business

- Strategic focus on international business

All of the above look highly plausible which will augur well for continued robustness in growth of KOEL.

Xpro India – getting bigger? (06-11-2023)

The supply-demand situation 2-3 years out is now looking bad for the industry.

- Xpro: 1 line already and adding 2 more lines. This itself will take care of ~75% of total domestic industry’s demand

- SRF: new entrant with 1 line as announced recently.

- Jindal: 1 line already operational and capacity utilization being ramped up. Getting the right quality is unlikely to be a challenge for them given that one of their subsidiaries is a global leader in this segment.

It seems like the industry will be in an over-supply situation in 2-3 years time unless the companies can crack the export market.

Pune Equity Discussion Group (06-11-2023)

We can make it online meet,rather than going and meeting…