Hi, i will be happy to join the meet.

Regards,

Ketan

Posts tagged Value Pickr

ValuePickr- Mumbai (05-11-2023)

Screener.in: The destination for Intelligent Screening & Reporting in India (05-11-2023)

Hi @kowshick_kk ,

For some companies, I’m seeing issue with Shareholding on screener.

One such page.

https://www.screener.in/company/JASH/consolidated/

Cera SanitaryWare Ltd (05-11-2023)

One more thing, as you said , in 2021, some investors were smart enough to predict the doubling of profit and hence PE was high. Currently PE is around 45, so does that same logic applies to current valuations too, that something good is still in future and hence such a high PE.

Cera SanitaryWare Ltd (05-11-2023)

Thank you so much for the update. What i get from your post is, its better to invest in SIP form with each dip in price.

SG Finserve Ltd – Does it has a scalable business? (05-11-2023)

Already there is thread for this stock. SG Finserve – is this birth of another Bajaj finance?

Dharmaj ready to benefit from high demand for agrochemicals (05-11-2023)

Dharmaj came with good set of results with sales growing by 14% and profits by 44%. These results are especially good given the weak agchem scenario currently. Their technical plant will be online this quarter, which might lead to subdued numbers for the next few quarters (depreciation costs + plant operating costs). Concall notes below.

FY24Q2

- Sayakha plant will be commissioned in November, it witnessed some cost overruns (cost escalations + additional equipment in MPP to improve product mix). Increased cost from 200 to 220 cr. Expect 10% utilization in FY24 and full utilization by FY27

- Will do external sales of ~600 cr. from plant + 100-150 cr. of internal consumption

- Inventory management: Purchase technical at the end to reduce price volatility risk

- 90-120 days receivable cycle. Increased receivables this quarter was because of higher sales in August which will be realized in October

- Have seeded smaller volumes to Rallis this year, expect higher growth in next year

- Fire incidence was minor and brought under control in half hour, not much losses

- CTPR: have got 9(4) registration to manufacture technical

- Technical pricing: have to compromise on prices in older molecules, but in newer molecules (such as CTPR), don’t expect lower pricing

- Gujarat, MP, Maharashtra are established markets for Dharmaj

- Farmer reach: 3L currently

- For any new product, 1st year is for field level demonstrations for demand generation, and 2nd year is for selling volumes

- Fixed costs for technical plant: 40-50 cr. in FY25 + Depreciation will be 24 cr.

- Hoping to do 60-65 cr. PBT in FY25

Disclosure: Invested (position size here, no transactions in last-30 days)

Cera SanitaryWare Ltd (05-11-2023)

Hi,

Thank you for seeking my views, I first bought Cera in 2019 because I had a view that residential real estate had bottomed out in India, and Cera was (and is still) one the most well managed building materials company. At that point, it was trading around 28x PE, which optically wasn’t cheap but they were one of the few companies which had grown sales and profits during the downturn.

I ended up selling in 2021 because I was not comfortable with the valuations at which it was trading (~58x trailing PE).

After selling, Cera’s profits more than doubled which suggests that in 2021, there were smarter participants than me who could foresee such a strong growth in profits, which is why it was trading at such multiples in the first place.

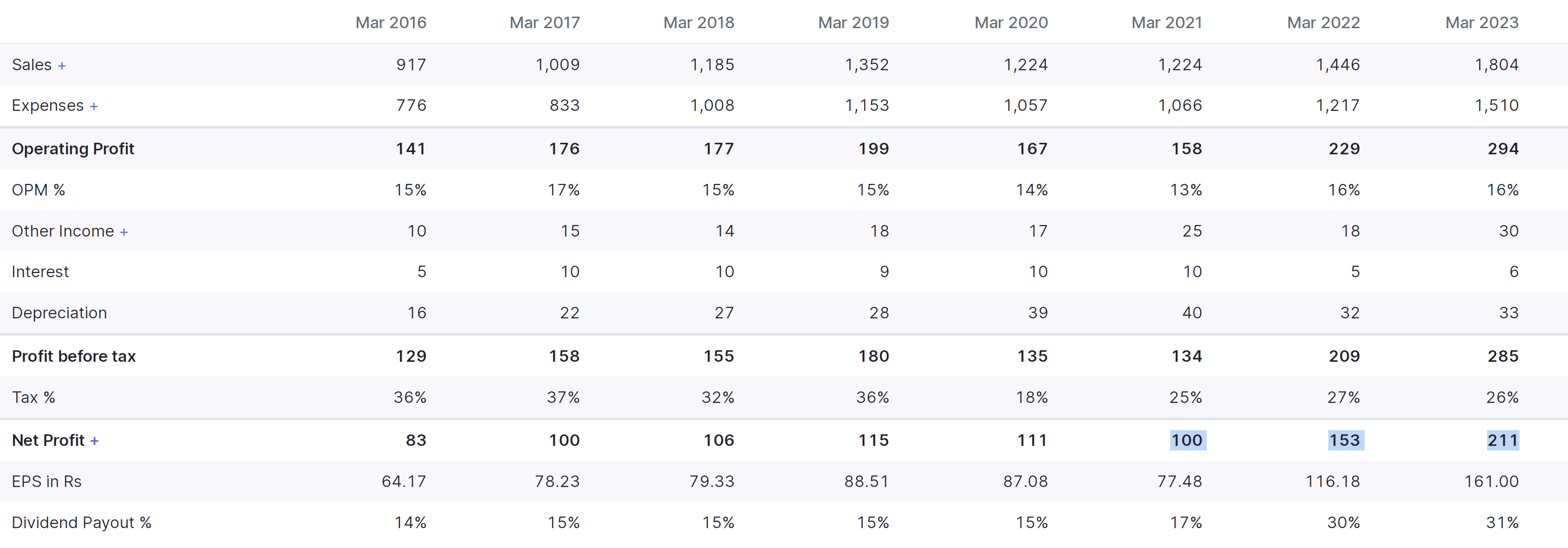

The most interesting thing which happened in Cera was they reported increasing margins during the commodity upturn in 2022, when most building material companies suffered. This was because Cera’s price increase was easily accepted by the market, and growth came back in their more profitable segments (sanitaryware, faucetware). Management had guided doubling sales (from FY22 levels) by 2025, which is probably why company continues enjoying higher valuations. However for me, I prefer buying real estate companies (or other building material cos like Stylam) which are exposed to similar tailwinds but are available at much much cheaper valuations. Apart from valuations, I don’t have any other concern w.r.t Cera. I have also attached my notes from FY23 below.

FY23Q1

- Hope to double topline in 40 months

- Cash has increased to 566 cr

- Volume growth ~ 10-15%

- Annual EBITDA margin should be 17-19%

FY23Q2

- H2 generally is 55% of annual revenues, confident of growing over 1600 cr. in FY23

- EBITDA margin guidance is for 15%+

- Gail gas cost price has gone to 33/m3 in October 2022. Average cost in Q2 was 25.7/m3 from GAIL (54% of requirement) and 74.87/m3 for the remainder (Sabarmati gas)

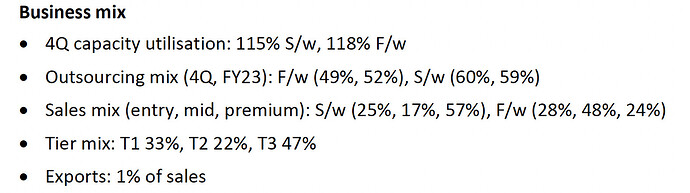

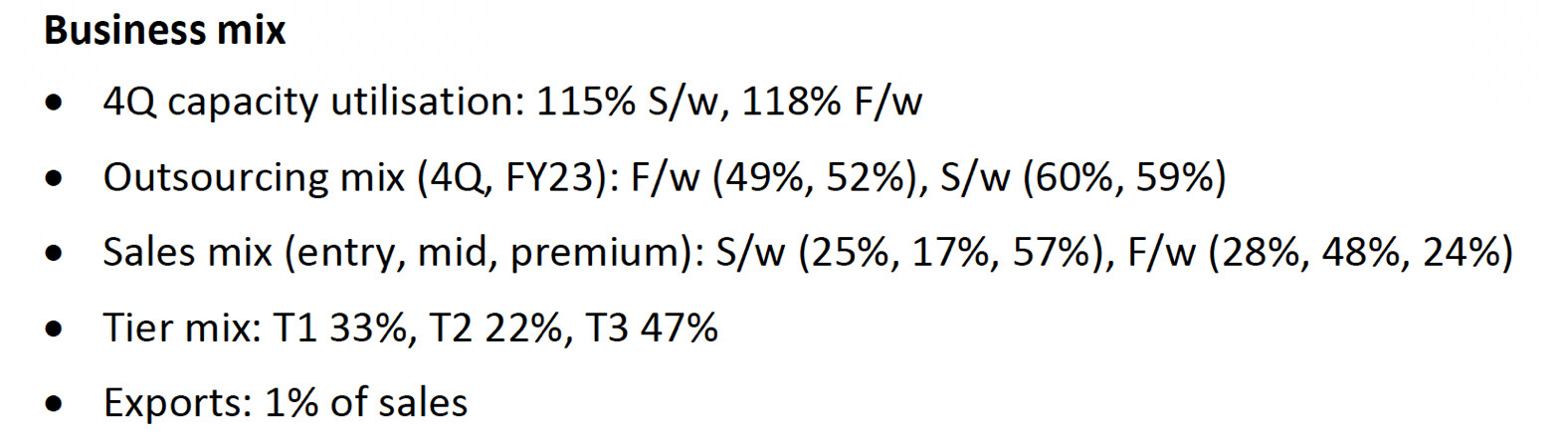

FY23Q4

- Industry grew at 6-7% vs Cera’s growth of 22% (both in sanitaryware and faucetware)

- Target: 2900 cr. revenues by September 2025

- Didn’t have to take price increase since May 2022 because of better cost efficiencies

- Rolled out new ad campaign (increased from 34-35 cr. To 57 cr.). Ad spends will remain at 4-4.5% of sales

- Largest co in sanitaryware and second largest in faucetware

- Dealers in March ’22 were 4,260 which in March’23 had become 5,462. And the retailers were around 11,300, which are now around 14,600.

- Looking to improve EBITDA margins by 75 bps in FY24

- Brownfield faucetware expansion ~ 69 cr. (capacity will increase to 48 lakh units by FY24)

- Greenfield sanitaryware expansion ~ 129 cr. (land purchase is 25 cr.)

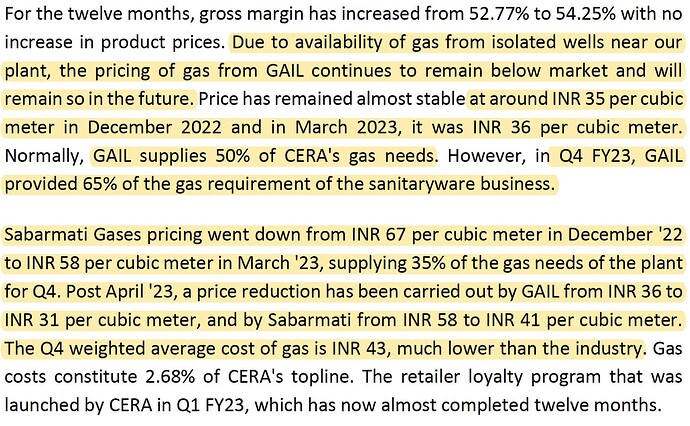

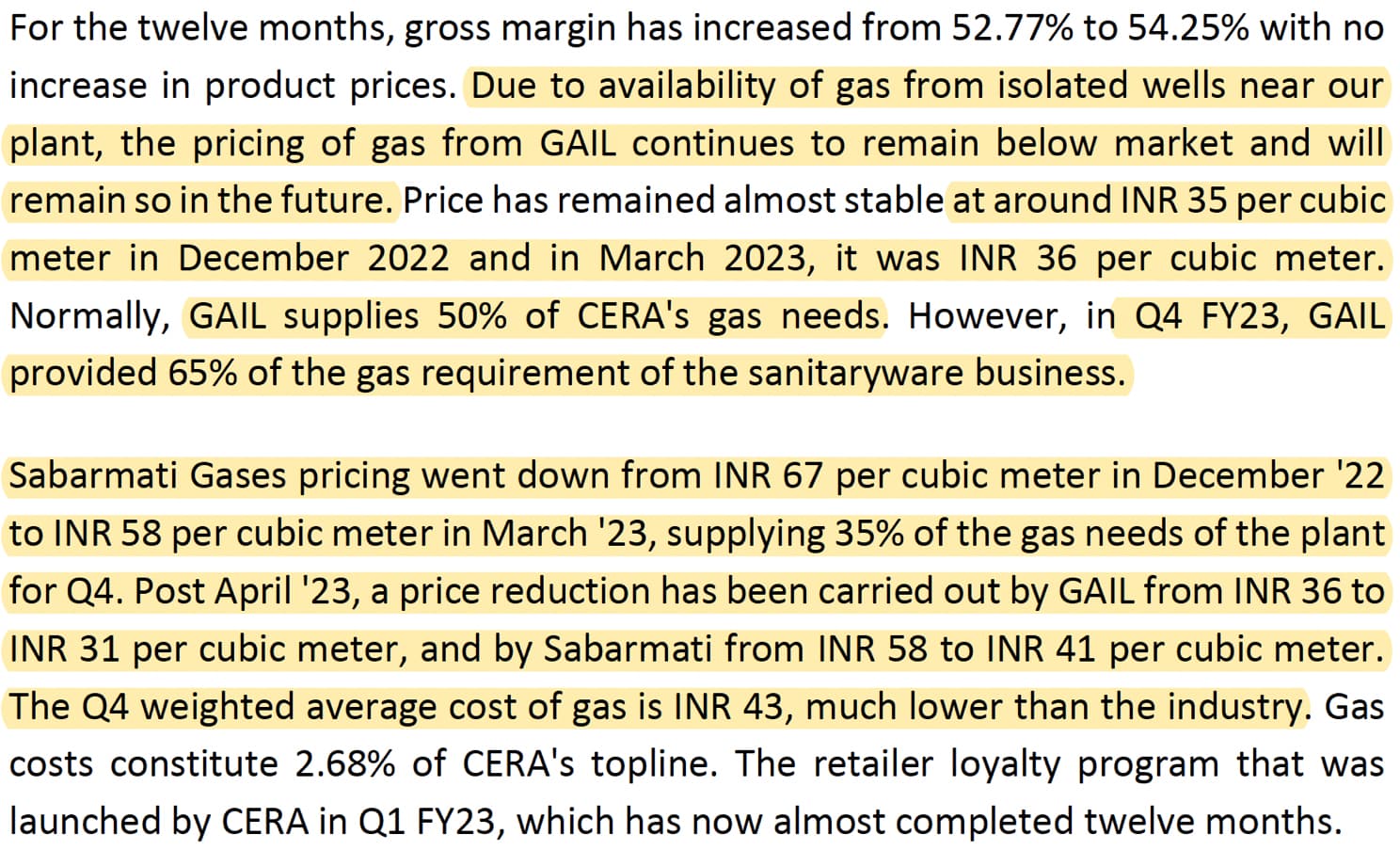

- Gas costs

Disclosure: Not invested in Cera (no transactions in last-30 days)

Prevest Denpro Limited (05-11-2023)

Will the co. be having a call to discuss the Q2 results…anybody having any info?

Aptus Value Housing : Is valuation justified or just another HFC? (05-11-2023)

Aptus continued with their growth trend (28% loan book growth, 23% in disbursement, 26% in interest income and 20% in PAT). They were facing some headwinds in Tamil Nadu due to higher attrition, where growth rates came down to 13% (vs 35%+ in other states). This problem seems to be normalizing now and they plan to maintain 25% loan book growth and add 30-35 branches annually (current branch count is 250). Concall notes below.

FY24Q2

- They increased SME loan rates by 50 bps in September 2023 and NIM growth trajectory will continue in next few quarters

- There was some attrition in Tamil Nadu at branch manager level which has affected growth (13% in TN vs 35%+ in other states). This problem has reduced recently and they are confident of reviving growth rates to 25% in FY24

- Growth strategy is always to go deep into a state and when going to a new state, start with places at border of the state nearby where they already have operations, and expand in a contiguous manner

- Always recruit local people for expansion

- Borrowing cost of NBFC is 25-50 bps higher than HFC (current borrowing cost is 8.25-8.3% for HFC)

- Will maintain spread of 8.5-9%

- Intend to add 30-35 branches annually

- Total pre-closures: 8% (5.5% from customer funds + 2.5% BT-out). According to my calculations, repayment/loanbook is 16% annually in normal times (e.g. Canfin) which translates to 4% quarterly. It becomes a problem when this increases to 20%. For Aptus, current quarterly number is around 4% which is fine

Disclosure: Invested (position size here, no transactions in last-30 days)

Krsnaa Diagnostics – what is the diagnosis? (05-11-2023)

Key Highlights of Q2 FY 24:

1.anagreement for the Assam Pathology tender, a significant opportunity that

encompasses 10 Labs and 1,256 collection centers. This development

significantly enhances our presence, covering all districts of Assam.

- Mumbai Facility: 15000 Sq Ft area in Kurla, current capacity 40000 tests per day, 6000 patients per day which is scalable upto 100000 tests per day, 15000 patients per day.

on Margin subdued on current quarter

Management reply: “It is important to acknowledge our profitability margins,

were impacted in comparison to the previous quarter. This impact can be attributed to the additional costs incurred for the on boarding of teams and operation and management of our newly established centers. We anticipate a positive trajectory in margins as these centers mature over the upcoming quarters.