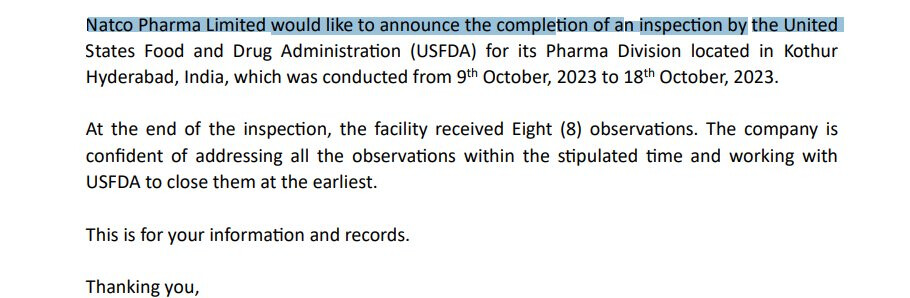

The USFDA with 8 observations is for Kothur facility. It is different from the USFDA clearence NATCO received for pharmacovigilance.

The USFDA with 8 observations is for Kothur facility. It is different from the USFDA clearence NATCO received for pharmacovigilance.

Kokuyo Japan is missing out the big opportunity in India. Single digit growth in Japan business is great, however a death warrant in Indian stationary and art space today. There are times when you really have to go full throttle, and the time is now. However Indian management has put the company on cruise control. Competitors are overtaking(Doms, Cello, Linc, HP, ITC, Pidilite etc) yet the parent company lacks proximity to Indian market. If focused well, Kokuyo can turn this India subsidiary into a $1B+ business in another 15 years. Tepid growth in Japanese market should not deter the parent to accelerate in a market like India. Art network is a good thing the current promoters have done, however there is more work needed in sales, channels, marketing and distribution.

Appointment of Mr. Masaharu Inoue may change the course. Demand pull is helping the company as of today, along with the softened raw material prices. The company has potential to double the sales in every 4 years, given the parent’s capabilities. Unfortunately, the company lacks the push as of today.

Key shareholder is missing from the action to fire up that ambition. Can Kokuyo and Mr.Masaharu Inoue correct it?

Disc: Invested.

Hey everyone,

KRBL is cylical business and depend deeply on rice prices globally. I want to know how to track Rice in India or International price.

Thankyou

Q2 Concall notes,

Financial Highlights (Q2):

ValueFirst Update:

Organic Growth:

Wisely ATP Innovation:

Q3 Outlook:

Customer Reaction to Price Increase:

Margin Impact of Price Hike:

VIL Contract Loss:

Wisely ATP Update:

Status of E-commerce Deal:

NLD SMS Pricing:

E-commerce Deal Ramp-Up:

WhatsApp Market Share:

Future Market Share Expectations:

UPI Transactions:

Greater than ₹50 Crore Client Bucket:

Volume Degrowth:

Wisely ATP Deployment in Saudi Arabia:

Revenue Impact and TAM for Wisely ATP:

Expansion Strategy and Focus on India:

Customer Loss and Competition:

Market Dynamics:

Strategies and Innovations:

Partnership with Kore.ai:

Co-sell Arrangement with Microsoft:

Impact of Vodafone India Deal on International Traffic:

Observing one thing

Filter copy using saregama music in there recent reels, observing from couple of days

Don’t know is they previously used or not

Anyone notice?

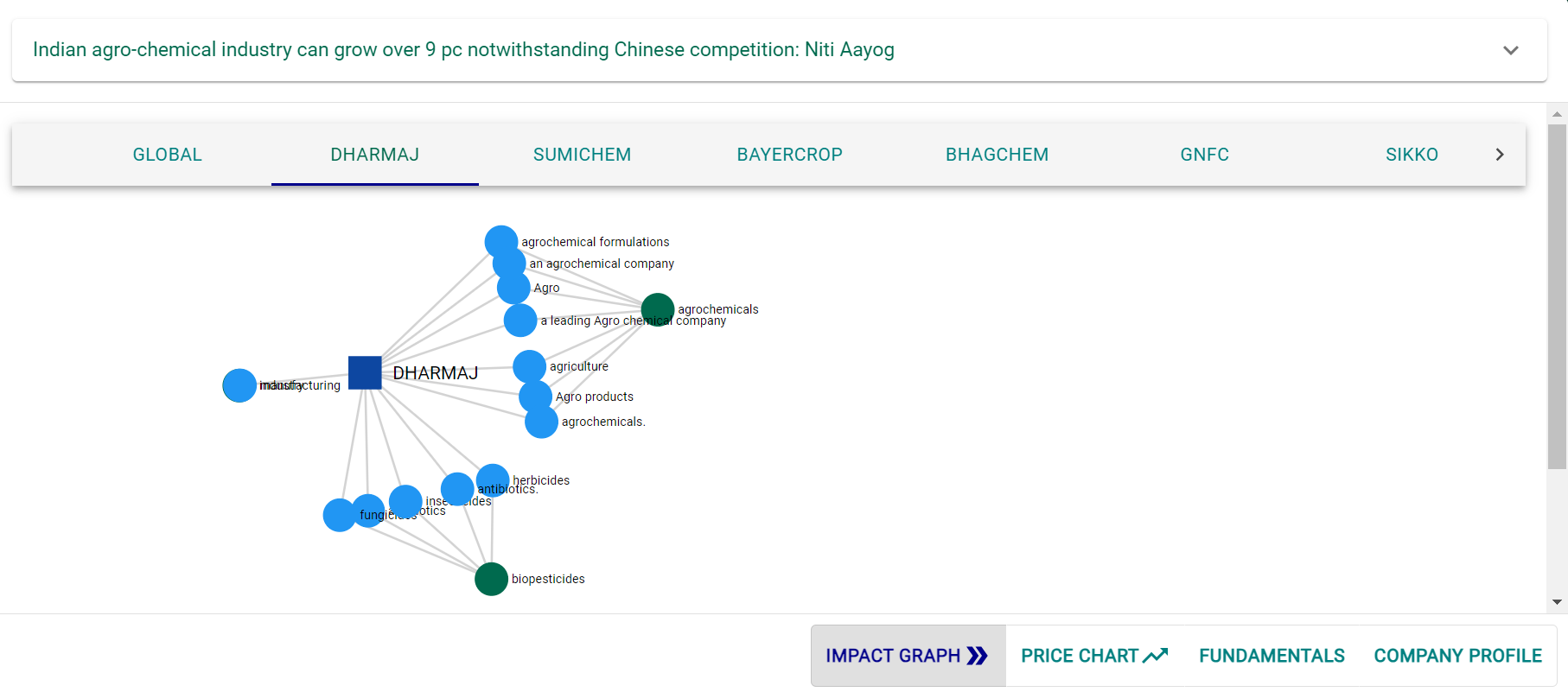

In a recent development, Niti Aayog member Ramesh Chand has expressed optimism about the growth potential of India’s agro-chemical industry, even in the face of stiff competition from China. This positive outlook for the sector has significant implications for companies operating in the agrochemical space, such as Dharmaj Crop Guard Limited, a leading player in the Indian market.

Dharmaj Crop Guard Limited (NSE:DHARMAJ), based in Ahmedabad, India, is actively involved in the manufacturing, distribution, and marketing of a wide range of agrochemical formulations. Their product portfolio includes insecticides, fungicides, herbicides, plant growth regulators, micro-fertilizers, and antibiotics, catering to both B2C and B2B customers.

Dharmaj Crop Guard Ltd (DCGL) is correctly positioned to capture growth in both domestic and international demand for agrochemicals.

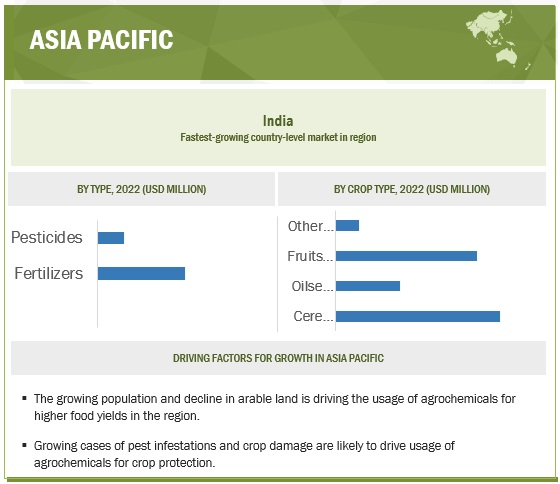

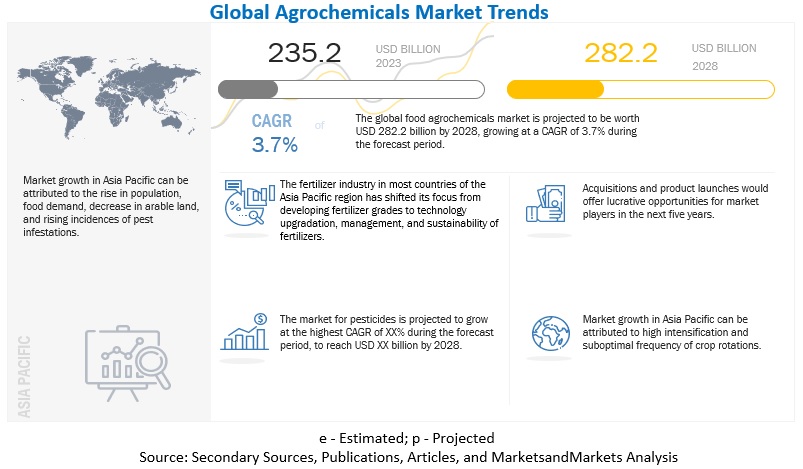

Domestic demand

International demand

Financials

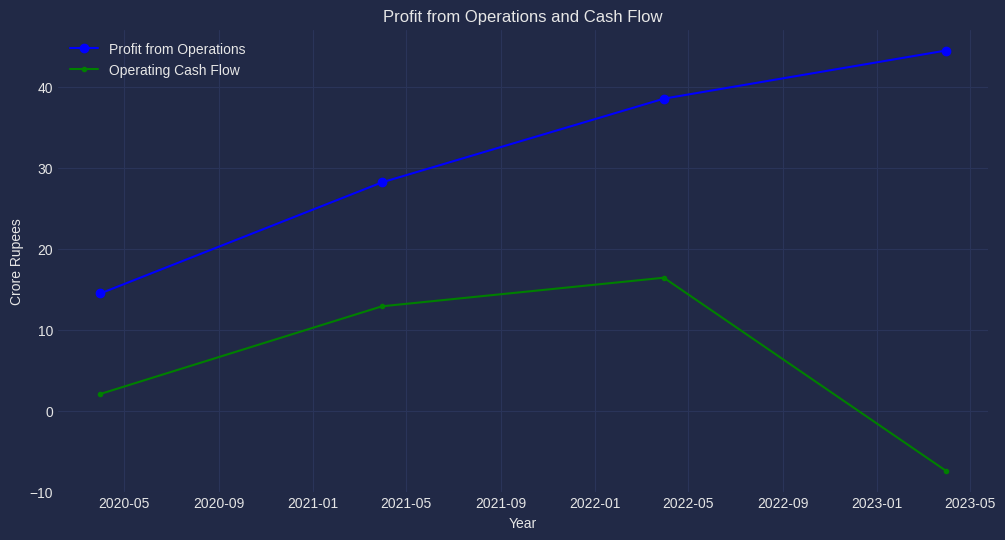

The financials are strong with sustained revenue and profit growth. However, the cash flow in recent reports has been on the lower side.

References

Indian agro-chemical industry can grow over 9 pc notwithstanding Chinese competition: Niti Aayog

Disc: Invested

Disclaimer: The article is not a recommendation or advice as to whether any investment is suitable for a particular investor.

| Stock | Avg. cost | Weightage % | Rationale |

|---|---|---|---|

| TATASTEEL | 133.73 | 5.15 | Large Cap Share bought at the mid of Cycle for long term , holding for rise to exit |

| JIOFIN | 246.91 | 3.72 | Good Potential with Reliance backing and good track record of disrupting businesses in India |

| ASIANPAINT | 3244 | 3.50 | Large cap and strong fundamentals |

| SBICARD | 787.43 | 6.22 | Credit card penetration in India is very minimal now , with SBI’s PAN India presence and large customer base it has great potential and also they are tieing up with Reliance Jio Mart |

| INFY | 1390.45 | 11.31 | Fundamentally strong Large Cap – IT and AI stock |

| BATAINDIA | 1874.95 | 1.22 | Holding only 2 qtys will dispose once meet the target |

| UJJIVANSFB | 57 | 1.56 | Longterm Holding in the Small Finance segment, Currently penetration is low in Rural Areas |

| EIDPARRY | 490.42 | 2.40 | Large cap and strong fundamentals |

| BANKBEES | 457.02 | 2.43 | Banking indices for general investement |

| SBIN | 580.6 | 4.51 | PSU Bank – Large Cap with strong fundamentals |

| TCS | 3402.93 | 5.30 | Fundamentally strong Large Cap – IT and AI stock |

| JWL | 315.98 | 1.83 | Railway Infra – holding a few stocks after profit booking |

| INTLCONV | 83.99 | 0.75 | Conveyor belt business – Has potential for Mining – Coal , Lithium , Iron Ore |

| HINDUNILVR | 2507.7 | 1.97 | Large cap and strong fundamentals |

| NATIONALUM | 107.6 | 0.15 | Holding only 4 qtys will dispose once meet the target |

| ULTRACAB | 19.99 | 0.06 | Cables Business – Bought for educational purposes |

| COALINDIA | 309.6 | 0.85 | Large cap and strong fundamentals |

| AMDIND | 59.55 | 0.03 | Experiment |

| TEXRAIL | 118.7 | 0.34 | Railway Infra – holding a few stocks after profit booking |

| KITEX | 187.95 | 0.80 | Fundamentally strong – Good track record and Professional Management |

| IRFC | 65.5 | 0.55 | Railway Infra – holding a few stocks after profit booking |

| SUZLON | 19.93 | 0.19 | Renewable Energy – Holding very few qtys |

| SUNDARMHLD | 126.68 | 3.10 | Large cap and strong fundamentals – For dividend income |

| WONDERLA | 796.95 | 1.05 | Huge potential in India for theme parks – New site added recently |

| POWERGRID | 191.44 | 2.64 | Power Sector |

| GMRINFRA | 43.04 | 0.71 | Fundamentally strong – Good track record and Professional Management |

| KOTAKBANK | 1695.95 | 10.29 | Bank- Private Sector |

| IDBI | 46.83 | 1.46 | Bank- Private Sector |

| GRNLAMIND | 490.4 | 4.26 | Longterm Investment in construction |

| NIFTYBEES | 191.95 | 5.01 | NIFY -General Investment |

| TATAPOWER | 183.97 | 2.17 | Power Sector Investment |

| BEL | 109.65 | 3.21 | Defence Sector Investment |

| TATACONSUM | 853.9 | 11.50 | FMCG – Similar to HUL but a growing company |

Hope this helps. These are my convictions based on which I continue my investing journey… I have been very cautious not to take too much risk.

Thanks

I too am invested and based on the comments above, I’ve decided to hold till at least Q2 results and con call.

Any update on unit holder meeting of ppfas . I think it used to happen in month of October

The guy putting the data in Screener portal should add investors to correct category from the start. This reclassification happens in 100s of companies each quarter (from my personal experience). Try comparing the shareholder structure of a random company from different sources eg. Screener, Trendlyne, Finology, Brokerage reports etc and you would observe some differences!