Per Google finance graphs, I am able to keep my ‘Stocks’ return above Nifty 50, for 6 Month and 1 year period.

Still very early and this is not my goal in anyway. Just sharing.

Per Google finance graphs, I am able to keep my ‘Stocks’ return above Nifty 50, for 6 Month and 1 year period.

Still very early and this is not my goal in anyway. Just sharing.

Won’t take a lot of time for Google Maps to beat that feature. Lot of hiring in India Maps team since last year.

Though the company has moat in B2B as mentioned many times in this thread (as compared to foreign players)

Portfolio Update – Oct2023

No change in Core Portfolio. Entry into Shyam Metalic in Satellite portfolio.

Core Portfolio

| Instrument | Weight |

|---|---|

| Titan | 16 |

| United Spirit | 15 |

| ITC | 14 |

| HDFC Life | 11 |

| LTTS | 7 |

| Pidilite | 7 |

| Dr Lal PathLabs | 6 |

| Nestle | 6 |

Satellite Portfolio

| Instrument | Weight |

|---|---|

| BCL Ind | 5 |

| MAFANG | 5 |

| FINEORG | 4 |

| RATNAMANI | 2 |

| SHYAMMETALIC | 2 |

MF – continuing SIP in below MFs –

PPFAS Flexicap

Motilal Midcap

Can anyone guide me – what are the key risks for the company – from now onwards

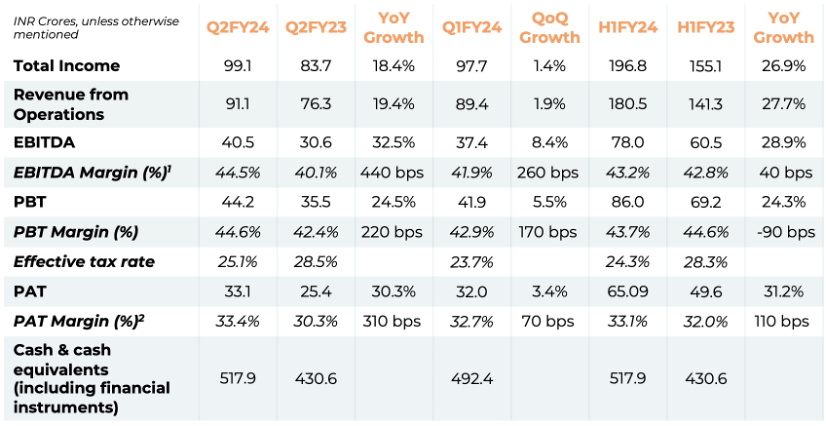

Figured I would add some of my notes from the Q2FY2024 earnings call here…

Financial Snapshot

June 2023 – Held an investor meet. 150 members of the investor community attended. Highlighted the ₹1000 cr revenue vision (FY27/28).

C&CE up from ₹431 cr to ₹518 cr y-o-y.

EBITDA and PBT margin improvements are evident.

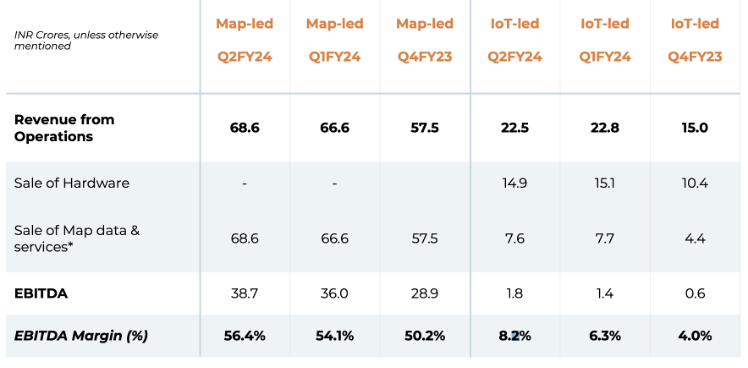

The IoT-led business has seen decent EBITDA margin growth (4.0% to 8.2% from Q4FY2023 to Q2FY2024). Both SaaS revenue, and better pricing for devices has helped here.

Map-led businesses have also seen EBITDA margins grow (50.2% to 56.4% from Q4FY2023 to Q2FY2024).

A&M Highlights

• Adoption increasing for spectrum of NCASE solutions with go-lives for multiple 2-wheeler EV/ICE OEM customer for Navigation Software and Wins including a 4-wheeler OEM customer for IoT supply, OEM customer for Shared Mobility Software platform and CV (Bus) OEM customer for Connected Vehicle Software platform

• Mobility wins include expansion of business with large State Road Transport Corporation business for public transit IoT-based monitoring and consumer-facing app solution, as well as extremely prestigious deployment for the G20 event for VIP cavalcade movement planning & monitoring.

C&E Highlights

• Multiple go-lives and wins across variety of new-age tech & traditional corporate customers for multiple solutions, including expansion of business with existing Payments & Fin-Tech conglomerate customer for territory/beat planning of large field force using geospatial analytics & API platform.

• Large E-commerce Company transporters and Multiple Large Cement companies signed up for IoT-led logistics optimisation, and Large Steel company signed up for Video Telematics for Mine Vehicles.

• Achieved Defence business and revenue based on wins and execution of multiple Defence customer projects.

Other Highlights

Besides our existing, core B2B and B2B2C business, we’re very happy that our B2C Mappls App has been receiving significant traction recently, and now has 11 Mn+ lifetime downloads, including 10 Mn+ on Android and 1 Mn+ on iOS.”

In terms of map and location data, platform, software, drone technology and the like, we are the only full-stack and integrated mapping solutions company in the country. We have a huge moat, network effects and technology reliability working in our favour, not to mention robust deep tech abilities to provide exactly what our customers need. There have been hundreds of companies who have tried to get into mapping in some way or another. But here we are.

In response to Ola’s mapping efforts, management highlighted, “Even Uber tried to have its own maps, but now is clear on its focus, and relies on external mapping partners.”

Keen to cover the entire span of drone opportunities, both organically and inorganically.

B2C apps can be a channel to sell devices and services. Kogo can be a great travel commerce play, not just a maps app. Then there’s advertising opportunities here as well.

Disclosure: Cost basis of ₹1137, entered early in CY2023. Long term hold for me.

As you said, < 100$/kwh, investment can go for a toss. Toss in the sense of asset payback – Asset turnover i think.

I have not studied Spread between raw materials for cells and final cell price $/KWH, but it seems OPM will maintain a range over a longer period of time. Any comment on this?

Any idea on how cost incurred to set up plant goes down with fall in cell price? That will determine asset payback and desire to add more capacities. Usually longer than 7 years asset payback slows down new capex.

Is plant fungible to other technologies like metal air, sodium based OR even different Li based compounds (likes of LiCoO2, LiMn2O4, LiFePO4, LiNiMnCoO2 etc) cathods ?

Source- Team-BHP forum article

Few anti-thesis points:

You may have come across in social media platfroms that the Lounges had big queues. I assume that most people were going there just because it’s available for free and I believe not many would go if there’s no free lounge access option.

I don’t think many of them would shift from current cards (500 AMC ) to premium cards (1500-2000 AMC) just to avail the Lounge access benefits.

Let’s ask ourselves the following questions:

From my limited understanding people are taking different Credit cards to avail shopping benefits (1.5% or 5% reward points) and the lounge access is not a deciding factor. So, I believe people will just let go of lounge benefits

From my above anti-thesis I believe that the revenue will not grow beyond 50% (not CAGR) in next 4 years and stock would not reach it’s ATH of 847 any time in next 3-4 years unless the contribution from their other business vertical (leasing their software to othe cos etc.). and I’ll not be buyer in a business with no growth at 35x P/E

Disc: My views are with limited understanding and no holding in the stock

The affect of War on Bromine realisation will be seen in Q3 results as conflict escalated from first week of October and Q2 was normal quarter and resluts are in line with other chemical companies?

Management guided that he is observing debottlenecking and guided for green shoots. So, more important to listen this concall to get clear picture as apart from media report, nothing is discussed about affect of War for this business in this or any other forum.

Also, there is a mention of upcoming selling pressure as lock-in period for shares will get over (read somewhere on twitter).

My question here for the more informed and experienced members is what is the average reaction on short term price due to this?

Disclaimer: New to investing have minimal knowledge.

I agree that may be true in somecases. But it’s not applicable for all cases (infact not applicable for most of the cases)

Take example of pidilite

One can see that the profit growth in last 10 years is in teens and the returns are higher because of the rerating. Basic common sense tells that the chances of profit growth will be only in teens for next decade as well. So, the returns would also be in teens (as valuation rerating from here onwards is quite difficult).

So what I mean to say is, If we pay high valuation like (50-100x) for a co growing <20% in sales and profits be ready for derating.

Short response to your above point is, “In Indian market with 2000+ listed stocks why buy a low growth, high PE stock that may fall 50% ?”

I’d rather wait and buy the stock at historically low valuations

Take example of Saregama Ltd

It’s a co that can grow profits at 20-25% CAGR. If someone paid 67x P/E for it, he/she should be ready for derating. But at Current P/E of 33x It’s not a bad decision to buy.

Cases where I’d pay high valuation:

Finally If someone is experienced enough to have vision on a co. for 10 years time frame, they should very well be aware and consider the entry valuation and drawdown potential

@CreateBetterVersion If the comments you’ve made are coming from experience of holding a stock for few years with drawdown, please share with examples. This would be a good case study to oppose the point I made and would help other participants

Thank you

Praveen

Disc: No recommendation by any means. Holding some of the cos discussed