Hdfc putting restriction for lounge access & that 1 lac limit per quarter. I think, HDFC is No. 1 in terms of credit card market share.

I was inclined to buy dreamfolks but such news puts question mark about volume growth (degrowth ?).

Hdfc putting restriction for lounge access & that 1 lac limit per quarter. I think, HDFC is No. 1 in terms of credit card market share.

I was inclined to buy dreamfolks but such news puts question mark about volume growth (degrowth ?).

Hello Ishmohit,

In your opinion which are the few themes in India which will continue to play out in the medium term?

I am positive about these themes

Not sure about the below themes which have already given massive returns recently

(post deleted by author)

Not thinking ahead makes one prone to errors of judgement… lack of big ticket releases owing to the cricket world cup in the first half of Q3 and the actors strike in hollywood notwithstanding, we have salman and ranbir to shake things up from mid november… I am not too gung-ho about the 699 monthly plan as upon reading the fine print it has a lot of ifs and buts… but well tried to the company management…

As long as good content gets generated this appears to be a reliable money making machine, post merger it has higher market share and caters to the luxury, premium and now with tweaks in f&b and rationalizing of ticket prices, attempting to tap the value seeking customers as well… for me, this dip appears to be a perfect opportunity to add positions for bigger targets … I am pre-empting an INHS in the weekly charts and as always, prone to pulling the trigger before time ![]()

Market expecting straight line profit growth?

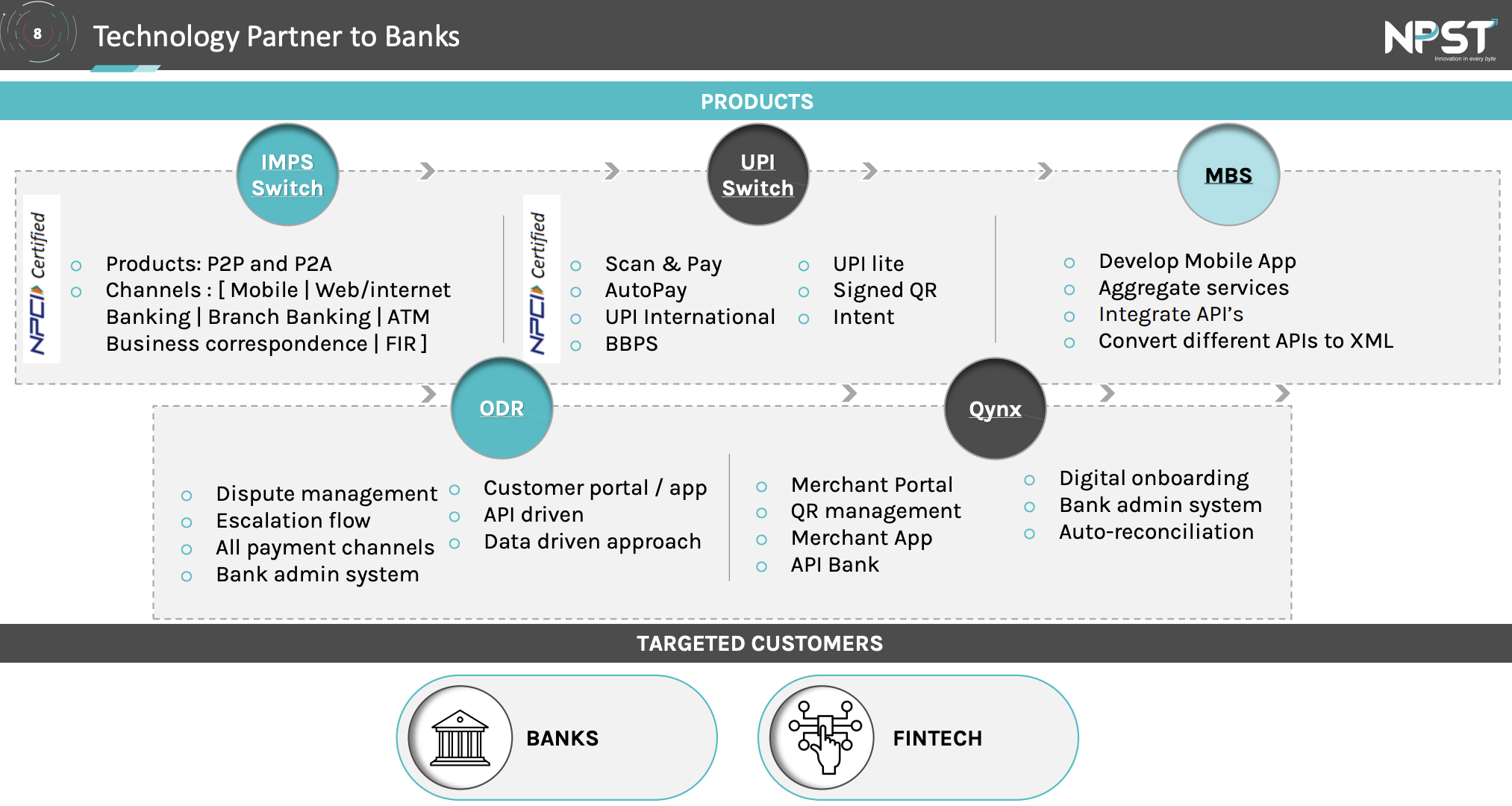

Established in 2013 Network People Services Technologies Limited (NPST) is a Fintech Company focusing on Digital Payment Solutions like UPI, IMPS, Mobile Banking & Wallets to Banks and Payment Companies.

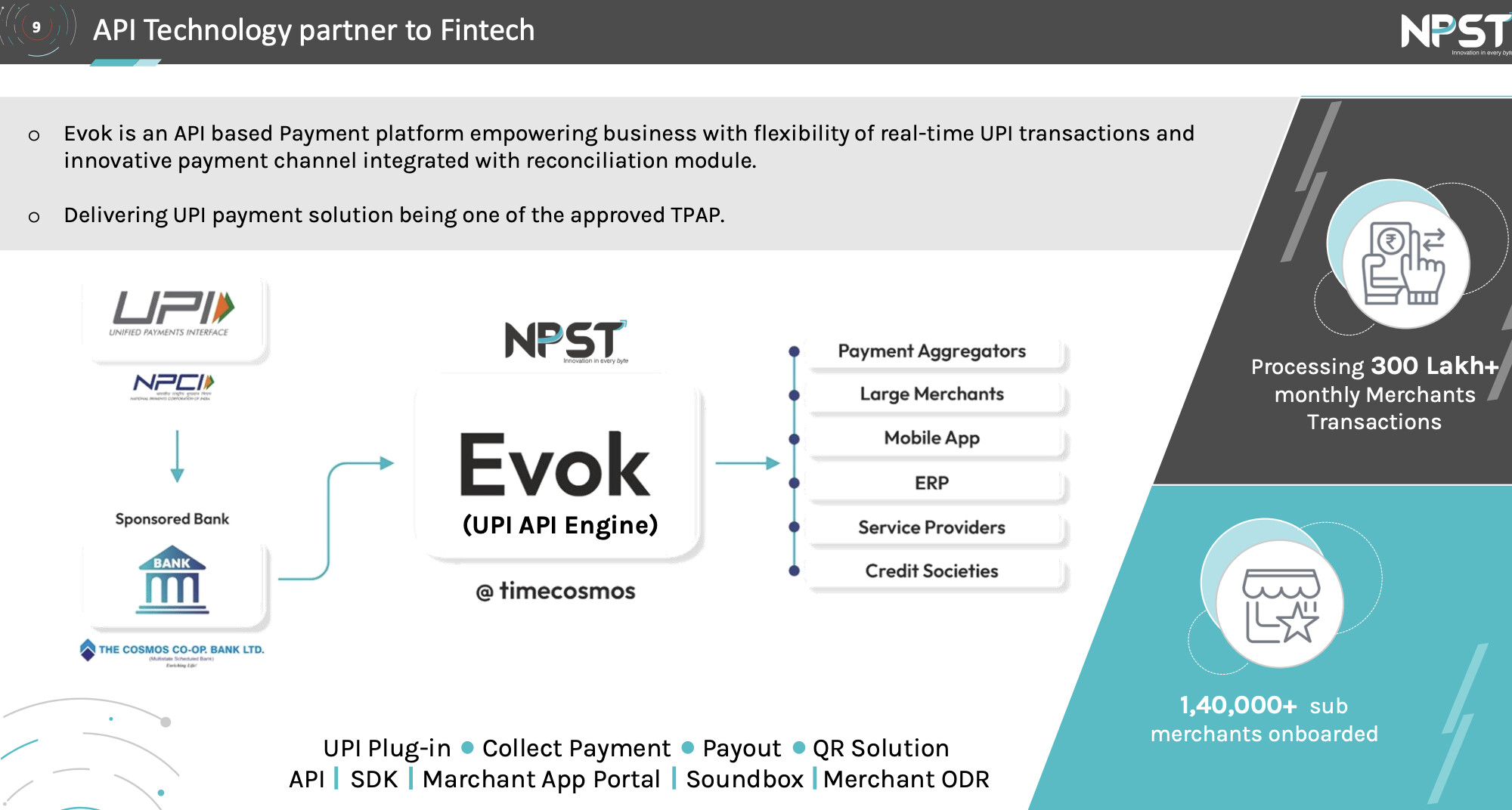

NPST is an authorised Merchant Payment Service Provider, approved by NPCI, providing payment solution to aggregators, merchants and users across various segments. NPST operate as “NPCI Approved Merchant PSP” digitizing Merchant acquiring space under the brand name of “TimePay”.

Currently, the company is providing its services under two verticals i.e. Technology Service Provider (TSP) and Third Party Payment Application Provider (TPAP).

Technology Service Provider (TSP) (For Banks & Financial Institutes)

Third Party Payment Application provider (TPAP) (For Payment Aggregator and Merchants)

Notes on Timepay app: this is actually called the payee business, where we give the APIs to our merchants or payment aggregators, where the sponsor bank is Cosmos. As part of this ecosystem, it is mandatory that we have a PSP application in the market. So, it was a mandate piece due to which we actually brought that application in market. We never promoted. We never pushed it, because our focus was always this API business, the merchant business.

API business (EVOK): when we give the API, we give it to payment aggregators and payment gateway on the bank platform. So, we play a technology API role in this particular segment. And those who are authorised to acquire merchants in market, or those who are merchants in market, those who need collection technology on UPI, or they need collection API, where they can collect funds for the services and the goods they sell in market. Or, re-sell those things, like payment aggregators and payment gateways.

So, these are the guys who take services from us. In order to do that, in order to manage the platform, right from the compliance, the reconsideration, the technology fees, the infrastructure, and the support system, the operations, there is a whole gamut of business that has to be built around it. And there is a cost around it. So, for that, we charge our payment aggregators and merchants on a SaaS model.

And I would say that those who are in merchant aggregation business, there are 30 odd accounts that we have in this particular segment, including something like PayG, EaseBuzz, or we are already in the final stage with Cashfree. So, these are the guys who would be using our services.

They have processed 4200 crore volume via their API in this quarter. It is only 0.1% of the total API business.

How NPST helps banks as TSP? We provide the interoperability switch between NPCI and bank. Okay, so every bank who wants to be on the UPI ecosystem, they need a partner like us. Because this is not the engine which is part of their core banking. This is a separate engine altogether which connects the bank’s core banking with the NPCI ecosystem and only then they participate in the UPI applications such as you transacting on a Canara Bank account on a Google Pay app. So, you need a processing engine in Canara Bank to connect to NPCI, only then Canara Bank will be in Google Pay app.

Revenue Split: Two third portion is from Evok business and one-third is from other business.

New area of growth:

Extra Notes:

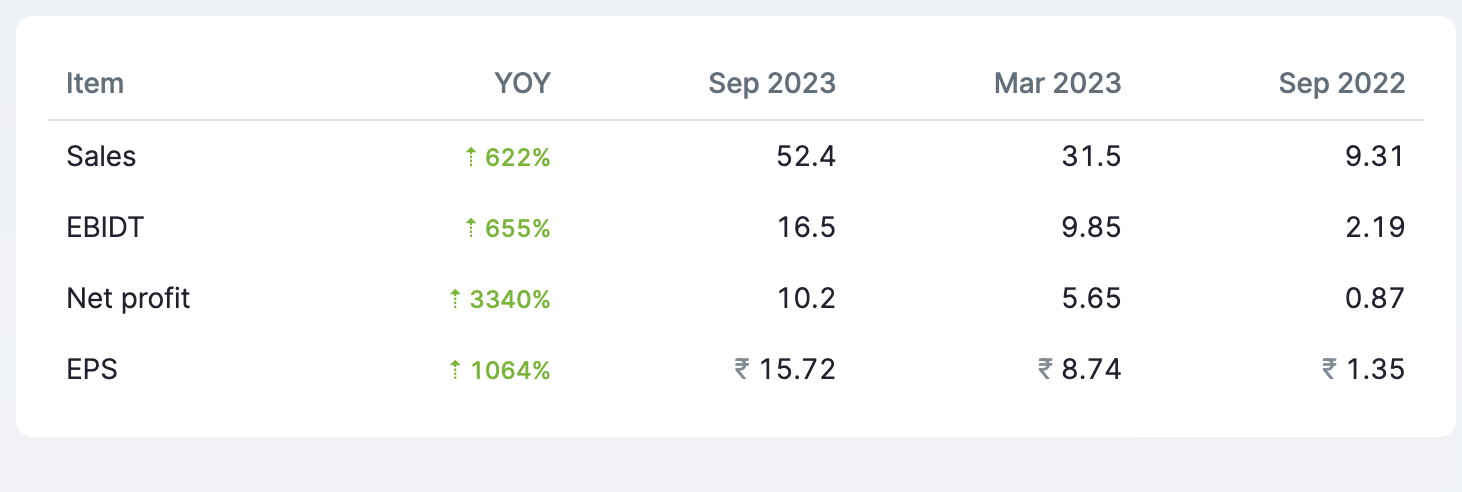

Results:

Risks:

Investment Rationale:

It would be great if people from the industry could share more insights on this API business (EVOK). As far as I can understand this is an actual area of growth for them.

Disclosure: Not invested

Current Market Cap: 1300 cr.

Markets finally bridging the huge valuation gap that was created after the Q2FY24 results.

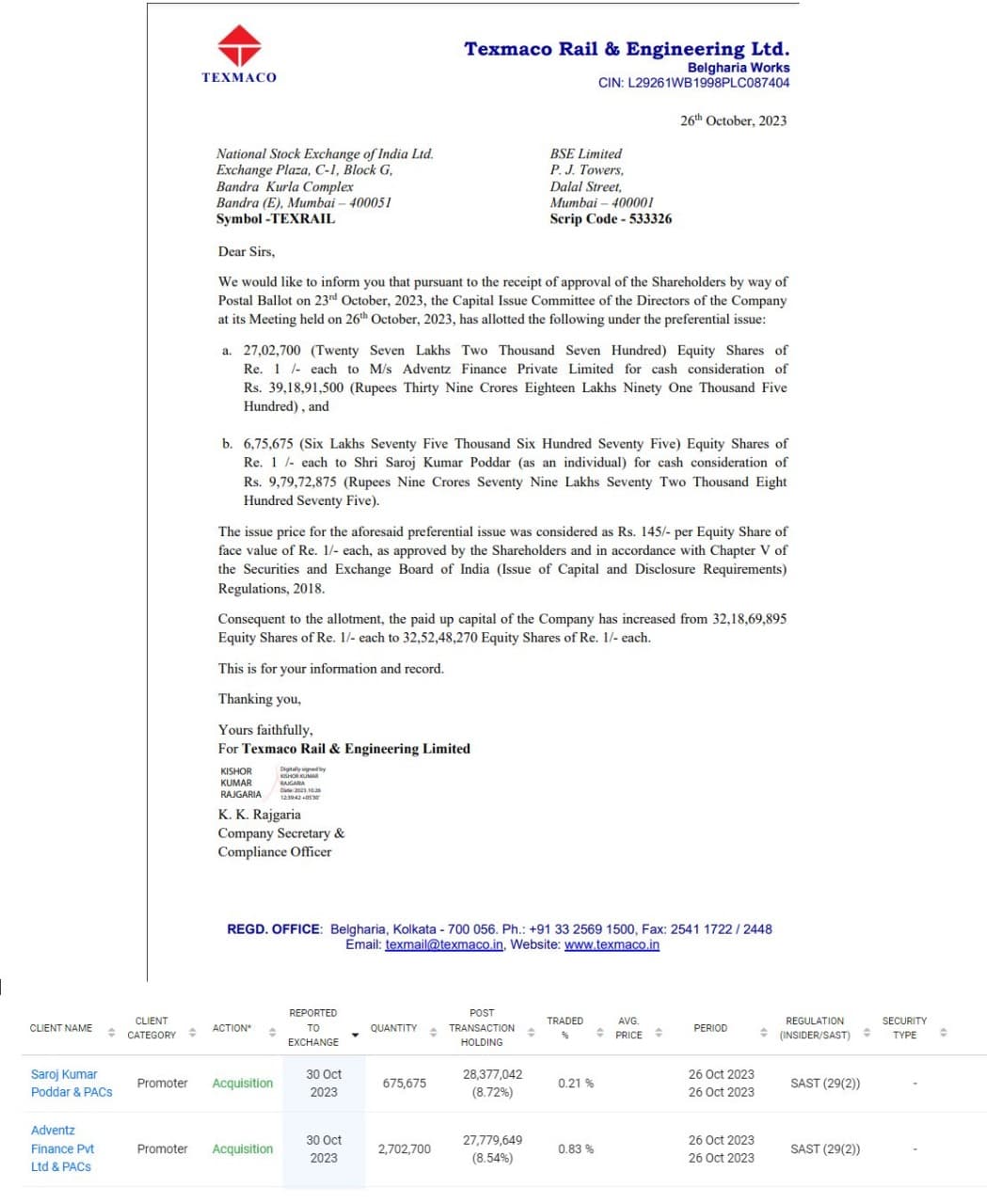

Texmaco Rail and Engineering

Just when the profits of years of perseverance have begun rolling into the bank for Natco Pharma, we minority investors are in a spot of bother due to twin negative news of legal action in US and the USFDA Form 483 with 8 observations during the Kothur plant inspection earlier in the month.

The legal action is of lesser concern to the company as it has a marketing partner in US who most likely has to bear the costs, and there are well established laws regarding patents in the country. However, Kothur plant is only one of the 2 USFDA approved manufacturing plants for Natco and this plant is capable of manufacturing cytotoxic orals and injectibles. It is imperative for the company to get a clean chit in the follow up from the USFDA. The Kothur plant is their older USFDA approved one and has been subject to audits from last many years.

Meanwhile the share price has taken a beating after the most impressive quarterly performance in the companys history.

In the long run price is a slave to earnings. Whileone is looking forward to the stellar Q2 numbers as guided by the mgmt in the post Q1 concall, here is hoping that more light is shed in the post Q2 concall by the management which would go a long way in calming nerves.

By the time Q4 results get declared Natco is anticipating a net profit of +1000 crores (management guidance) and this has a 50% probability of being bettered in the following year.

So maybe its best that I uninstall the trading app for the next 7 months ![]()

60cr every year is optimistic target and add to that their D/E is already at 1.2. Interest rates will continue to remain high for the next 9-12 months and so I think they will go for equity dilution (pledge, sell stake, warrants, rights issue, preferential allotment etc).

But either way, servicing the existing debt will be challenging for the company and could easily spiral out of control, if not serviced properly